Cookstoves

Key Takeaways

- Not all cookstove carbon credits are created equal—legacy projects using outdated methodologies show systematic over-crediting of up to 1,000%, while newer metered and CCP-track projects deliver far more reliable emission reductions.

- For CSRD compliance and greenwashing risk management, the critical question isn't whether cookstove credits are inherently "good" or "bad," but whether each specific project meets today's integrity standards with verifiable monitoring data and conservative baseline assumptions.

- High-quality cookstove credits can serve as short-lived avoidance offsets with strong social co-benefits in an Oxford-aligned portfolio, but only when paired with rigorous due diligence on methodology version, usage tracking (ideally metered or SUMS-verified), and independent quality ratings.

- Using a structured evaluation framework—checking for CCP labels, MoFuSS-based fNRB calculations, direct stove-use monitoring, and third-party ratings like BeZero or Calyx—is essential to ensure your credits can withstand both auditor scrutiny and media investigations.

Introduction

You've probably seen the headlines: "Cookstove carbon offsets overstate climate benefit by 1,000%." Then you look at your procurement budget and see cookstove credits priced at a fraction of what durable removals cost, with compelling stories about health improvements and women's empowerment in Sub-Saharan Africa. So which is it—are cookstove carbon credits a cost-effective way to support real impact, or a greenwashing liability waiting to blow up in your next CSRD audit?

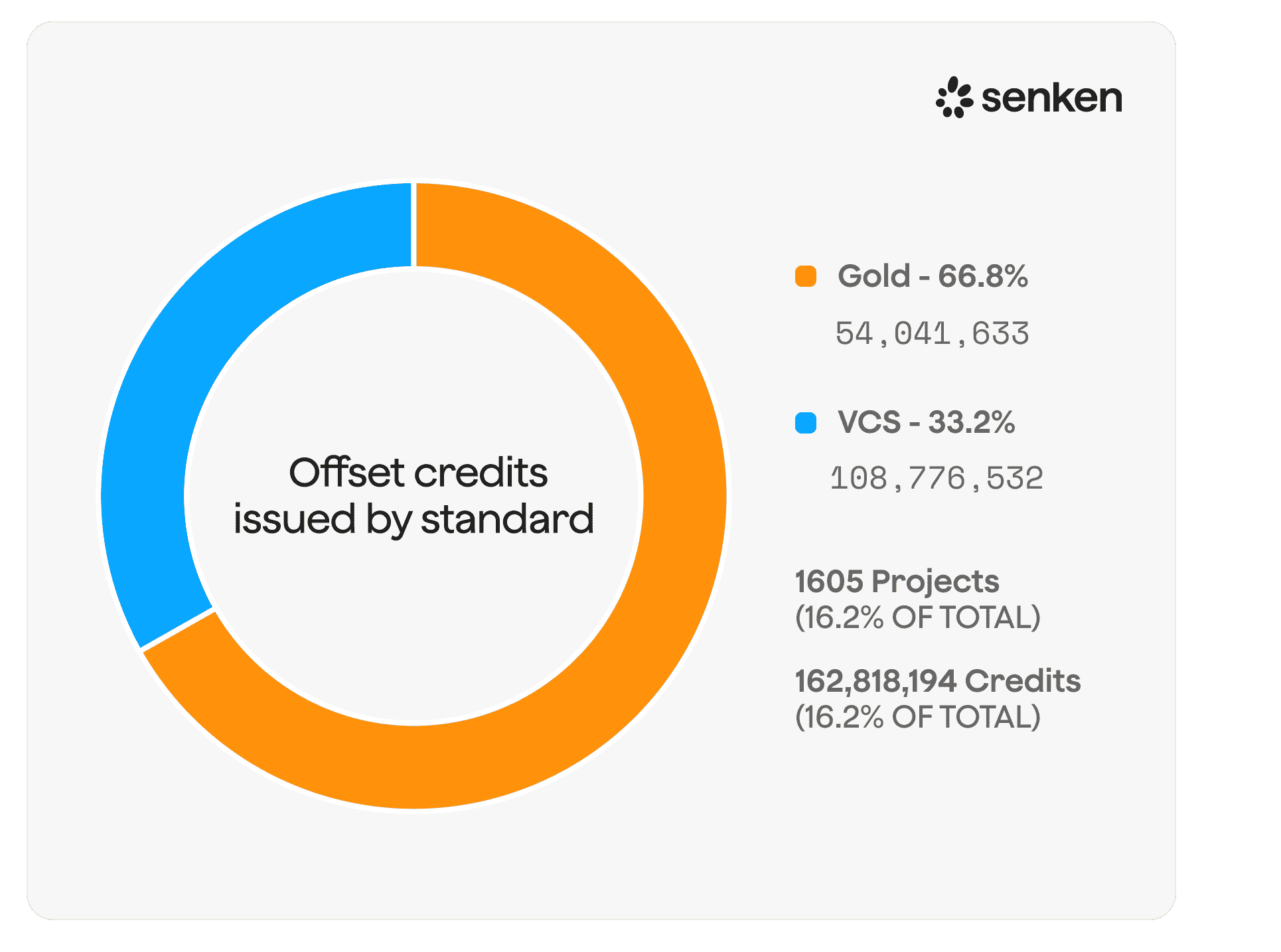

Cookstove carbon credits are verified emission reductions generated when households replace traditional cooking methods—open fires or basic biomass stoves—with cleaner alternatives like improved biomass stoves, LPG devices, or electric cookers. These projects have issued over 181 million credits since 2004, representing roughly 7–8% of the entire voluntary carbon market. The theory is solid: more efficient combustion means less fuel burned, which translates to fewer greenhouse gas emissions. Add in health co-benefits from reduced indoor air pollution, and you have a project type that ticks multiple SDG boxes.

But recent research from UC Berkeley, regulatory reforms from ICVCM, and high-profile over-issuance scandals have exposed serious quality gaps in much of the existing supply. The reality is that cookstove credits span a massive quality spectrum—from projects with robust metered monitoring and conservative baselines that genuinely deliver climate impact, to legacy vintages built on inflated assumptions and survey-only data that may over-credit by an order of magnitude. For DACH sustainability managers navigating CSRD documentation requirements and board-level scrutiny, the stakes are clear: you need a practical framework to separate signal from noise, not a blanket yes-or-no answer. This article gives you that framework—covering how cookstove projects actually work, what the latest science reveals about effectiveness, which integrity risks matter most, and exactly what to check before you buy.

What Are Cookstoves Carbon Credits

Cookstoves carbon credits are avoidance credits generated when projects replace traditional cooking methods (open fires, three-stone stoves, basic charcoal burners) with improved biomass stoves or clean-fuel devices like LPG, electric, or ethanol cookers. These projects quantify the greenhouse gas reductions from lower fuel consumption and cleaner combustion, then issue credits under methodologies from Gold Standard, Verra, and other registries.

For DACH sustainability leaders, cookstove credits have been attractive: they typically price in the mid-single-digit Euro range per tonne, come with compelling SDG narratives (health, gender equity, jobs), and help fill the gap between internal decarbonisation and near-term net-zero claims. Over 181 million cookstove credits have been issued since 2004, making up roughly 7-8% of all voluntary market issuances. Most volume comes from Sub-Saharan Africa, where over 2 billion people still lack access to clean cooking and household air pollution causes millions of premature deaths each year.

But the market has shifted dramatically. In 2024, a Berkeley study found that widely used cookstove methodologies over-credited by an average factor of around 9-10x, driven by inflated baseline assumptions, optimistic usage data, and weak monitoring. In response, the Integrity Council for the Voluntary Carbon Market (ICVCM) disqualified many legacy methodologies and approved only three cookstove approaches as Core Carbon Principles (CCP) eligible, subject to strict conditions. Verra cancelled over 5 million over-issued cookstove credits following a quality review. German companies face additional pressure: Deutsche Umwelthilfe lawsuits and CSRD auditors now demand underlying assumptions, usage data, and independent ratings, not just registry IDs.

According to Senken's analysis, 68% of DAX40 companies that bought carbon credits ended up with projects delivering no real climate impact, and 84% of credits on the market are high-risk. The result: cookstove credits are no longer a single quality bucket. The real question for your procurement and compliance teams is whether each specific project meets today's integrity criteria and can survive auditor and media scrutiny.

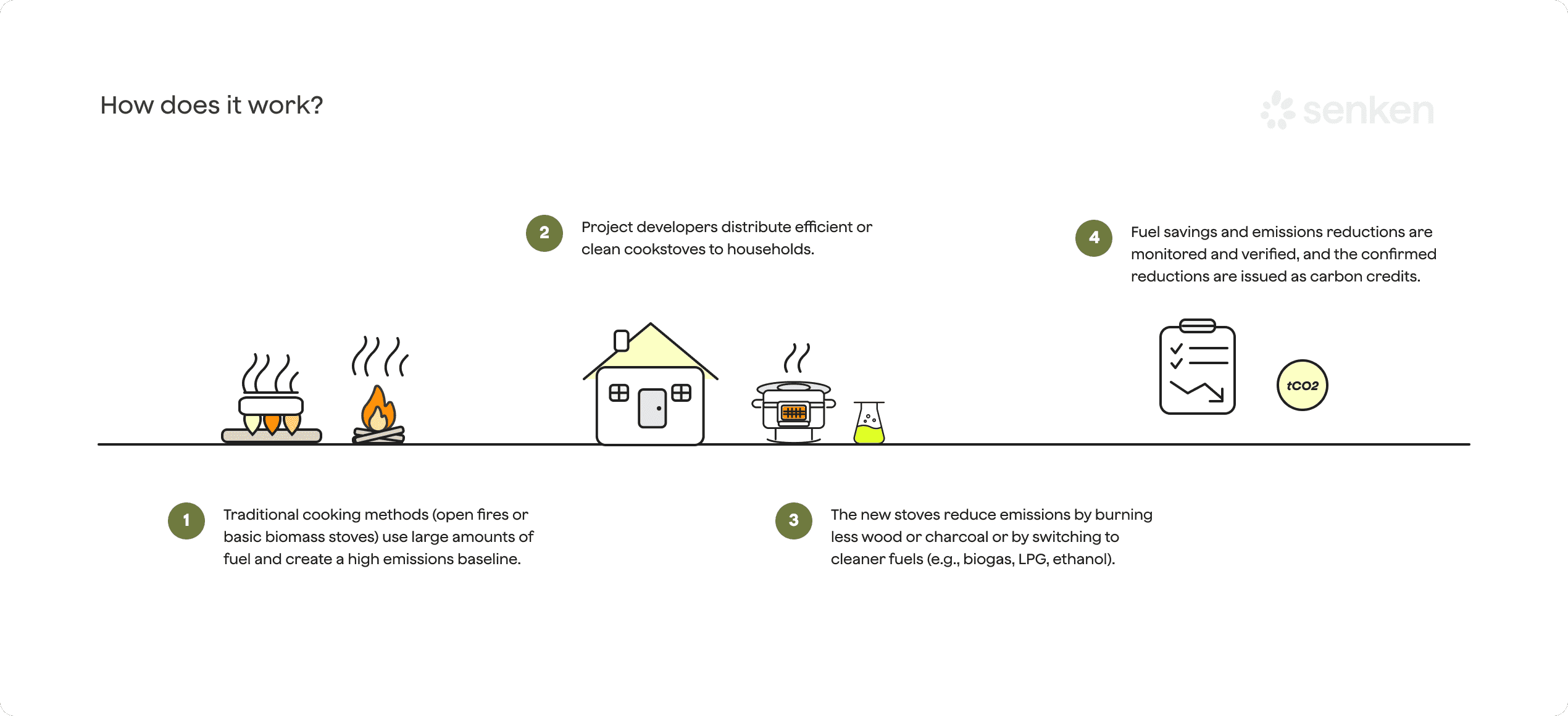

How Cookstove Projects Actually Generate and Measure Emission Reductions

Understanding the mechanics behind cookstove carbon credits is essential before you evaluate quality. Projects generate emission reductions in three main ways, each with different accounting methods and risk profiles.

Improved biomass stoves versus clean fuel stoves

Improved biomass stoves boost efficiency by 30-60% compared to traditional open fires. Better insulation, controlled airflow, and optimized combustion chambers mean households use less firewood or charcoal per meal. The carbon benefit comes from avoided deforestation (where biomass is non-renewable) and lower emissions of CO2, methane, and black carbon. These stoves remain affordable and culturally familiar, making them easier to adopt in rural settings.

Clean fuel stoves (LPG, electric, biogas, ethanol) replace high-emission solid fuels entirely. Because these fuels produce far fewer pollutants per unit of energy, clean stoves deliver larger health co-benefits and more predictable emission reductions. Electric cooking, when paired with renewable grids, can approach zero direct emissions. However, clean fuels often require ongoing supply chains and recurring costs, creating adoption and usage risks if subsidies or credit revenues disappear.

Fuel-switching and behaviour-change programmes combine stove distribution with community education and monitoring. These projects tackle the "stove stacking" problem by encouraging households to fully replace old cooking methods rather than using new and old stoves side by side.

Use this simple comparison when assessing projects:

| Stove Type | Fuel | Efficiency Gain | Emission Reduction Mechanism |

|---|---|---|---|

| Improved biomass | Wood, charcoal | 30-60% | Lower fuel use, cleaner burn |

| Clean fuel (LPG, electric) | Gas, electricity | 70-90% | Fuel switch to low-carbon source |

| Behaviour change + monitoring | Mixed | Variable | Sustained usage, reduced stacking |

From lab tests to field data: how reductions are calculated

Emission reductions depend on three core variables: baseline fuel consumption (how much a household would have burned without the project), fraction of non-renewable biomass (fNRB, the share of wood or charcoal that would otherwise drive deforestation), and usage rates (how often and how completely families use the new stove).

Older methodologies relied on survey-only monitoring and default fNRB values, often drawn from outdated national data. Modern approaches use tools like MoFuSS (a geospatial model that estimates fNRB based on local biomass supply and demand), kitchen performance tests (KPTs) that measure real-world fuel consumption, and Stove Use Monitoring Sensors (SUMS) that log ignition events and temperature over time. Electric cooking projects can meter energy use directly, removing much of the uncertainty.

Many methodologies also use Monte Carlo simulations to model uncertainty across thousands of scenarios. The problem: results are only as good as the input ranges. If a developer feeds optimistic assumptions about stove efficiency, adoption, or fNRB into the model, the simulation will produce inflated credit volumes. That is why, when you review a project, you need to ask not just "Was Monte Carlo used?" but "What data fed the model, and who validated it?"

This technical foundation is what transforms a stove distribution programme into a credible carbon credit. It is also where most legacy projects fell short, and where the new generation of metered, CCP-track projects stand apart.

How Effective Are Cookstoves Carbon Credits in Practice? What the Latest Science Says

The title question has a nuanced answer: some cookstove credits are effective; many are not. The difference comes down to methodology, monitoring, and how well the project handles real-world adoption challenges.

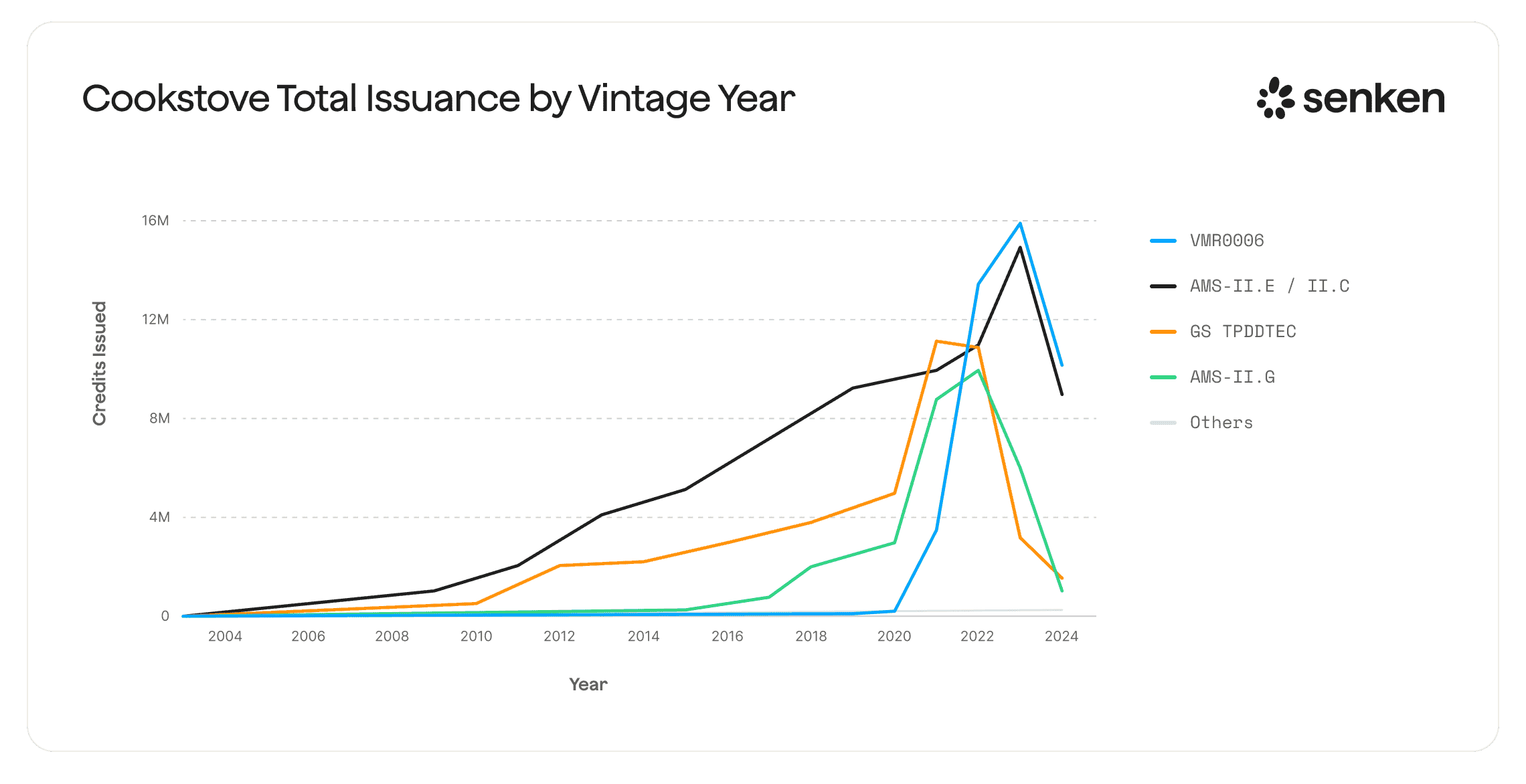

What the Berkeley and RMI analyses actually found

In 2024, UC Berkeley and RMI published a comprehensive quality assessment covering a large sample of cookstove projects, representing roughly 40% of all issued cookstove credits. The core finding: average over-crediting of approximately 9.2x across widely used methodologies. The worst cases showed over-crediting by more than 1,000%, while the best (Gold Standard's metered approach) landed closer to 1.5x.

What drove this gap? Four main factors:

- Inflated fuel baselines: Projects assumed households would burn far more wood or charcoal than they actually did.

- Optimistic fNRB values: Using defaults like 0.9 (90% non-renewable) in areas where biomass was partly renewable or imported.

- Overestimated usage: Survey data showed high adoption, but sensor data revealed frequent stove stacking or abandonment.

- Charcoal conversion factors: Generous assumptions about how much wood is needed to produce charcoal inflated credit volumes.

Independent rating agencies like BeZero and Calyx have confirmed similar patterns. Projects using old CDM-era defaults and survey-only monitoring consistently score low, while those with SUMS, metered data, and conservative baselines rate much higher.

The good news: the market has responded. ICVCM's 2025 CCP decisions now require projects to use MoFuSS for fNRB, adopt a 4:1 wood-to-charcoal conversion factor, and demonstrate verified fuel-use measurement. Verra consolidated older cookstove methods into VM0050 with stricter baseline and monitoring rules. Gold Standard's Metered & Measured methodology for electric cooking is now setting the benchmark for transparency.

Legacy versus next-generation projects: drawing the line

For your procurement team, "cookstove credits" is not a single quality bucket. Think of the market in three tiers:

- High-risk legacy projects: Issued under old methodologies, survey-only monitoring, generous fNRB defaults, no SUMS or metering. These credits may have already been flagged or cancelled. Price: often €3-5/t on secondary markets.

- Transitioning projects: Developers moving to updated methodologies (Gold Standard TPDDTEC v4, Verra VM0050) with improved monitoring. Quality depends on how fully they implement the reforms. Price: €6-9/t.

- Next-generation, CCP-track projects: Metered electric cooking, SUMS-verified biomass stoves, Article 6-labelled credits with corresponding adjustments. These projects meet or exceed ICVCM conditions and carry independent ratings of A or AA. Price: €10-15/t or higher.

For CSRD auditors, the question is not "Are cookstove credits bad?" but "Can you defend this specific vintage and methodology with hard data?" That means checking registry documentation, methodology version, monitoring reports, and external ratings before any purchase. If a supplier cannot provide that documentation quickly and clearly, walk away.

Key Integrity Risks in Cookstove Credits – And How the Market Is Tightening

Baseline, fNRB and Monte Carlo data quality

Baseline inflation is the top concern. If a project assumes households would burn more fuel than they realistically would, every tonne of "avoided" emissions is overstated. Older projects often used national averages or aspirational consumption figures rather than direct household surveys or fuel-use monitoring.

fNRB assumptions can swing credit volumes by a factor of two or more. A project using 0.9 fNRB (claiming 90% of biomass is non-renewable) will issue nearly twice as many credits as one using 0.5 (50% renewable). The problem: many legacy projects used outdated or overly generous fNRB defaults. ICVCM now mandates MoFuSS modeling or a conservative 0.3 default, with leakage adjustments if fNRB rises above certain thresholds. When you review a project, ask: "What fNRB was used, how was it derived, and has it been updated since project registration?"

Monte Carlo data quality is where technical modeling meets buyer scrutiny. A Monte Carlo simulation runs thousands of scenarios to estimate credit volume and uncertainty. But if the input distributions are optimistic (e.g., stove efficiency between 45-60% when field data shows 30-50%), the model will produce inflated results. Look for projects that document their Monte Carlo assumptions, cite field studies, and had those assumptions independently reviewed. If a developer cannot explain what ranges were used or why, that is a red flag.

Stove stacking, double counting and registry issues

Stove stacking happens when households keep using their old stoves alongside the new one, especially for larger meals or when fuel for the new stove runs out. This cuts the real emission reduction by 30-70%. Older projects relied on survey self-reporting; modern projects use SUMS or metering to detect stacking objectively. Ask for stacking data: what percentage of households show consistent, exclusive use of the new stove?

Double counting emerges in two forms. First, jurisdictional overlap: a national clean cooking programme and a project-based credit scheme might both claim reductions from the same households. Second, within carbon markets: if a project issues credits under one registry and then seeks Article 6 authorization without retiring the original credits, those tonnes may be claimed twice. Article 6 "corresponding adjustments" are designed to prevent this, but implementation is still uneven. Always confirm that credits carry a clear, single claim and are not also counted in national inventories.

Registry and methodology transitions create temporary gaps. Verra's consolidation of cookstove methods into VM0050 meant that projects registered under older methodologies had to either transition or stop issuing credits. Some projects delayed or struggled with the new requirements. Similarly, ICVCM's CCP conditions are prospective, so credits issued before 2024 may not automatically qualify. When buying cookstove credits, check the issuance date, methodology version, and whether the project has a clear path to ongoing CCP eligibility. Credits from a project that has not updated its monitoring since 2020 are high risk.

The market is tightening because registries, ICVCM, and rating agencies are now explicitly modeling these risks. The result: a clear quality gap between projects that anticipated these reforms and those that did not. For buyers, this is good news. You now have clearer signals on what to avoid and what to prioritize.

A Practical Quality Checklist for Evaluating Cookstove Projects

Three non-negotiable checks for CSRD-ready quality

1. Methodology and version check: Only consider projects using Gold Standard TPDDTEC v4.0 or later, Gold Standard Metered & Measured, or Verra VM0050. Confirm the project is either CCP-labelled or has applied and can demonstrate compliance with ICVCM conditions (MoFuSS fNRB, 4:1 charcoal conversion, verified fuel-use measurement). If the project is registered under an older methodology and has not transitioned, it is high risk. Ask for the methodology name, version number, and date of last update.

2. Monitoring and data check: Request evidence of SUMS deployment, metered devices, or recent kitchen performance tests. For biomass stove projects, ask what percentage of households have sensors and how often data are collected. For electric cooking, confirm that energy use is metered per household and reported monthly. Ask to see a sample monitoring report and verify it includes stove usage rates, fuel consumption data, and clear documentation of how Monte Carlo input ranges were set. If a project relies solely on annual surveys without sensor or meter data, pass.

3. Independent quality signals: Cross-check with external ratings from BeZero, Calyx, or Sylvera. Look for ratings of BBB or higher. Also review Senken's Sustainability Integrity Index (SII) scorecards, which evaluate over 600 data points across carbon impact, beyond-carbon co-benefits, reporting processes, and compliance. If a project has no external rating or scores poorly, treat it as high risk even if the registry label looks good. A "Gold Standard" badge alone is no longer enough; you need to verify the specific methodology, vintage, and third-party assessment.

Questions to send to any cookstove developer or broker

Copy these questions into your procurement emails. Suppliers who can answer clearly and quickly are more likely to offer quality credits. Those who dodge or delay are red flags.

- What methodology and version is this project registered under, and is it CCP-eligible? (If not CCP-eligible, ask for a detailed explanation of why and what the transition plan is.)

- What fNRB value was used, and how was it calculated? (Accept MoFuSS modeling or a conservative default of 0.3 or below. Reject generic national defaults above 0.5 without site-specific justification.)

- What monitoring tools are in place? (Require SUMS, meters, or KPTs conducted within the past 12 months. Survey-only monitoring is insufficient.)

- What is the measured stove usage rate and stacking rate? (Look for >70% exclusive usage and <30% stacking. If the developer cannot provide these numbers, they likely do not have them.)

- What were the key assumptions in the Monte Carlo simulation, and who validated them? (Ask for input ranges on efficiency, usage, and fNRB. Confirm a third-party auditor reviewed the model.)

- What co-benefits are documented, and how is community feedback collected? (Strong projects can show health impact data, gender-disaggregated employment figures, and community grievance mechanisms.)

- What happens if the project is later found to be over-credited? (Ask if the seller offers replacement credits, refunds, or insurance. Get the policy in writing.)

- What independent ratings does this project have? (Request rating agency scores and links to public scorecards.)

Keep this documentation in an evidence pack for CSRD and EU Green Claims audits. Your auditors will ask for proof that you conducted due diligence and can trace each tonne to a credible, independently verified project. Structured checklists like this, combined with Senken's multi-layer verification framework (registry data, dMRV, third-party audits, external ratings), operationalize quality at scale without overloading a small in-house team.

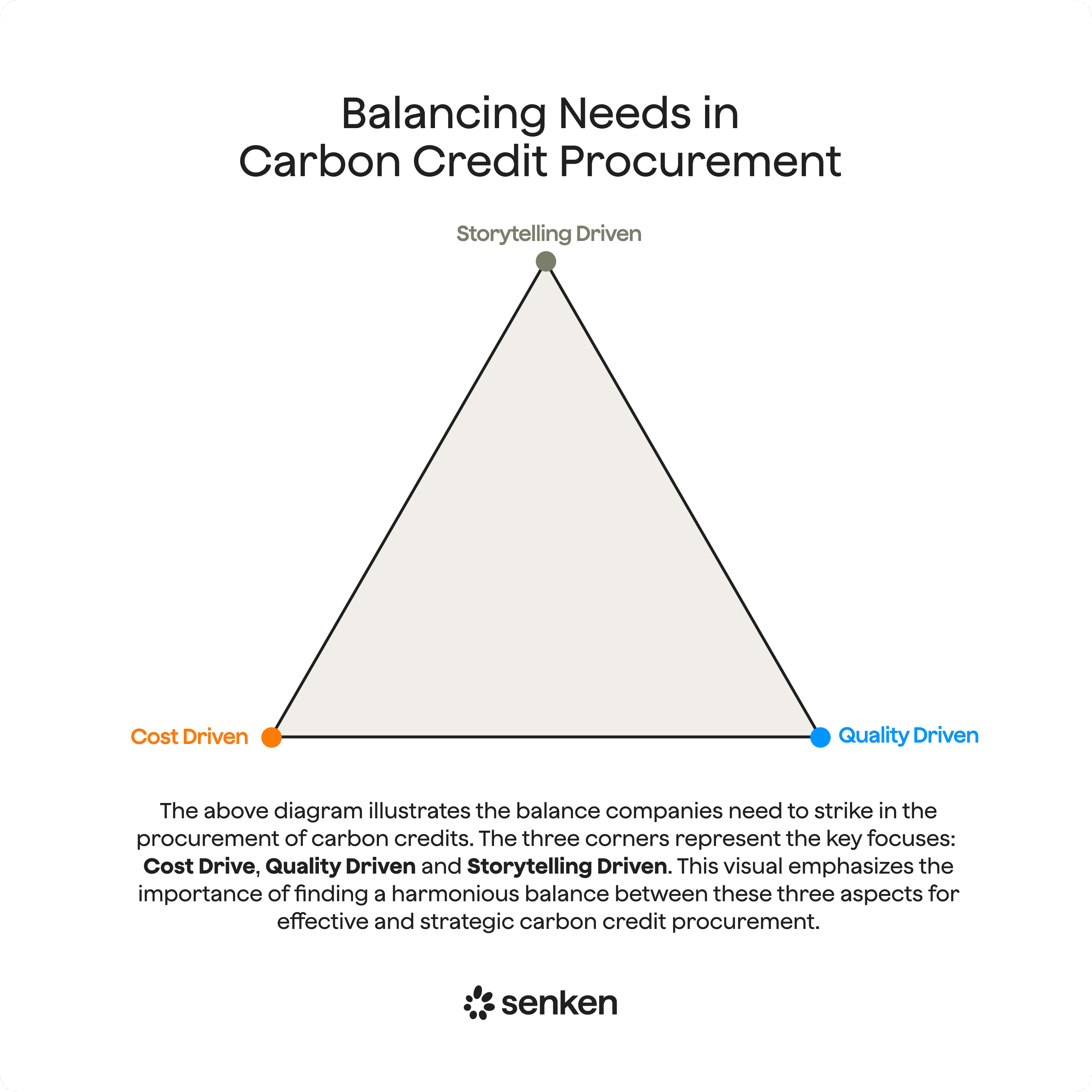

Where High-Quality Cookstove Credits Fit in an Oxford- and CSRD-Aligned Portfolio

Once you have identified genuinely high-quality cookstove projects, the next question is strategic: where do they fit in your broader carbon portfolio?

Position metered, CCP-eligible cookstove credits as short-lived avoidance with strong social co-benefits. They work best as a complement to long-duration removals like biochar, afforestation, or enhanced weathering, not as a substitute. The Oxford Principles recommend that companies increase their share of removals over time, especially those with permanence above 100 years. High-integrity cookstove credits can help you neutralize a small portion of residual emissions in the near term, while you ramp up internal decarbonisation and build a durable removal pipeline.

Here are three simple portfolio rules for DACH corporates:

1. Cap exposure to non-CCP, non-metered cookstoves: Set an internal policy that no more than 10-20% of your annual credit purchases come from cookstove projects unless they carry a CCP label or meet equivalent metered standards. This limits greenwashing risk and signals to stakeholders that you prioritize long-term, high-integrity solutions.

2. Prioritise projects with clear Article 6 or CCP labels and independent ratings: Article 6 authorization with corresponding adjustments ensures credits are not double-counted in national inventories. CCP labels confirm adherence to the latest integrity benchmarks. Independent ratings (BeZero AA/A, Sylvera AAA/AA, or Senken SII high scores) provide a third layer of assurance. When choosing between two cookstove projects at similar prices, pick the one with stronger labels and ratings every time.

3. Invest a growing share of your budget into durable removals over time: As your company moves toward net zero, shift the portfolio balance from avoidance (including cookstoves) to removals. For example, in 2025-2027, you might allocate 70% removals and 30% avoidance (with high-quality cookstoves as part of that 30%).

By 2028-2030, aim for 85% removals and 15% avoidance. Document this transition in your climate strategy and CSRD disclosures to show progression toward Oxford alignment.

4. Build an audit-ready evidence pack: For every cookstove credit purchase, keep copies of the methodology document, monitoring reports, external ratings, Monte Carlo assumptions, fNRB calculations, and seller replacement/refund policies in a central repository. Link each credit retirement to specific scope 1, 2, or 3 emissions in your carbon accounting system. When CSRD auditors or board members ask how you chose these credits, you can walk them through a structured decision framework rather than pointing to a registry logo.

Clean cooking enterprises now derive a significant share of their revenues from carbon finance, and high-integrity carbon demand is a genuine lever for SDG progress. The 2024 Africa Clean Cooking Summit mobilized over $2 billion in commitments, much of it tied to carbon credit markets. By insisting on quality, you help channel finance toward projects that genuinely improve lives and reduce emissions, while protecting your company from the reputational and compliance risks of buying over-credited supply.

If your current portfolio includes legacy cookstove credits or if you want to design an Oxford-aligned, CSRD-proof multi-year strategy, consider working with a specialist procurement partner. Senken's SII-based portfolio reviews and multi-year offtake planning help teams like yours stress-test credit quality, diversify risk, and lock in supply at stable costs before prices rise or regulatory requirements tighten further.