Greenwashing

What greenwashing means for corporate climate and carbon-credit claims

Greenwashing is the gap between what a company says about its environmental performance and what it actually delivers. At its core, it's misleading consumers, investors, or regulators about how green a product, service, or strategy really is. While the term has been around for decades, its meaning has sharpened considerably in the past few years, especially for large EU companies navigating climate commitments and carbon markets.

Management research frames greenwashing as a form of "decoupling" between symbolic green talk and substantive action. A company might announce a bold net-zero target, publish glossy sustainability reports, or stamp products with "climate neutral" labels while its underlying emissions trajectory, supply chain practices, or offset portfolio tell a different story. That disconnect is what regulators, auditors, and increasingly sceptical stakeholders are now scrutinising.

For sustainability leaders, the most critical exposure sits in climate and carbon-credit claims. These are the statements that carry the highest reputational and legal weight: net-zero pledges, carbon neutrality labels, offsetting disclosures, and nature-based solution narratives. When these claims rest on vague language, selective data, or low-quality carbon credits, the line into greenwashing territory is crossed quickly and often without intent.

The difference between intentional deception, careless over-claiming, and good-faith evolving practice matters less under the new EU rules than you might think. If the evidence backing your claim is weak or missing, regulators treat it as a risk regardless of motive. That shift puts the burden squarely on sustainability teams to ensure every public environmental statement can withstand external audit and regulatory review

Why greenwashing is now a strategic risk under EU rules (not just a reputational issue)

Greenwashing used to be primarily a brand and PR concern. Today, it's a compliance, legal, and board-level governance issue. Three major EU regulatory developments have transformed the landscape for large companies.

First, the Corporate Sustainability Reporting Directive (CSRD) requires sustainability disclosures under European Sustainability Reporting Standards (ESRS) starting with FY 2024 reports. These disclosures are subject to dual materiality assessments and external assurance, meaning every material climate claim in your sustainability report must be traceable to robust data and methodology. Auditors will ask for the same level of evidence they demand for financial statements.

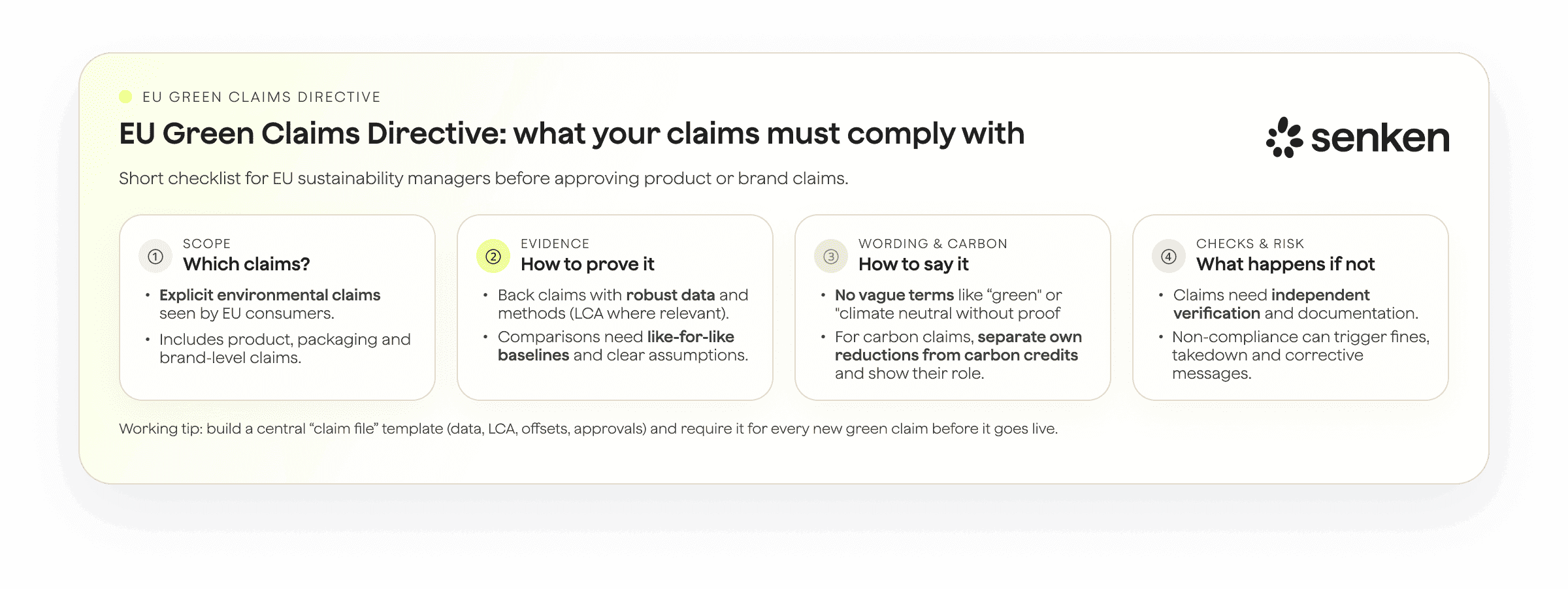

Second, the Empowering Consumers for the Green Transition Directive (amendments to the Unfair Commercial Practices Directive) came into force in 2024 and must be transposed into national law by March 2026. It bans generic environmental claims that lack substantiation and prohibits offset-based "climate neutral" labels unless they reflect actual lifecycle impact. This affects product marketing, packaging, and consumer-facing communications directly.

Third, the proposed Green Claims Directive will require companies making explicit environmental claims to verify them through accredited third parties within 30 days. Violations will carry fines of at least 4% of annual turnover, with potential confiscation of revenues linked to misleading claims. While still in draft, the direction is clear: substantiation standards are tightening, and enforcement penalties are rising sharply.

Beyond regulation, greenwashing carries serious financial and operational risks. The Volkswagen Dieselgate case showed how misrepresented environmental performance can destroy market value almost overnight. VW's share price dropped approximately 40% in two days, erasing €30 billion in market capitalisation, with reputational losses estimated at five times the operational penalties. Negative spillovers hit European competitors and suppliers too, demonstrating how greenwashing scandals ripple across sectors.

For your day-to-day work, this means scrutiny of climate claims now comes from all directions: boards nervous about enforcement actions, auditors demanding substantiation files for CSRD, Legal flagging exposure under consumer protection law, and Finance calculating potential fines as a material risk. Greenwashing is no longer just a comms problem; it's a strategic governance challenge.

Where greenwashing actually shows up in climate, net-zero and carbon-credit claims

Understanding where risk concentrates helps you focus internal controls. The highest-risk patterns in large-company practice fall into a few recognisable categories.

Offset-based "climate neutral" labels are the most visible flashpoint. Slapping "climate neutral" or "CO2 neutral" on a product because you purchased offsets to match its footprint is now legally problematic in the EU unless you can demonstrate outstanding environmental performance and actual lifecycle impact. German courts ruled the term ambiguous; companies must clarify whether it means emission reductions or mere compensation. Deutsche Umwelthilfe has successfully sued major brands like Faber-Castell and Beiersdorf over such claims, arguing they rely on low-quality offset projects that mislead consumers.

Net-zero pledges without interim targets or Scope 3 coverage represent another common pattern. Announcing a 2050 net-zero goal sounds ambitious, but without science-based interim milestones for 2025, 2030, and 2035, and without addressing value-chain emissions (often the largest share of your footprint), it's green talk without a credible pathway. The UN High-Level Expert Group's "Integrity Matters" report makes this explicit: credible net-zero requires near-, medium-, and long-term absolute targets across all scopes.

Reliance on low-integrity carbon credits is where the voluntary carbon market's quality crisis directly creates greenwashing exposure. A study published in Science found that only 6% of credits sampled from forest preservation projects delivered additional, verifiable emissions reductions; over 60 million credits assessed barely reduced deforestation. Separately, research identified that 33 of the top 50 corporate offset buyers held more than one-third of their portfolios in "likely junk" credits. When your offsets don't represent real climate impact, any claim built on them collapses under scrutiny.

Selective storytelling is subtler but widespread: highlighting a "green" product line or renewable energy procurement while core business emissions and Scope 3 footprints continue to grow. It's not lying, but it's curating a narrative that gives a misleading overall impression of environmental performance, exactly the kind of selective disclosure regulators are targeting.

Moving from risky to compliant claims means shifting from "We offset 100% of our emissions" to "We follow a science-based reduction pathway aligned with SBTi, reducing absolute emissions by X% by 2030, and use independently verified, high-integrity carbon removals only for residual emissions we cannot yet abate."

How to design climate and ESG claims that avoid greenwashing in a CSRD world

The best defence against greenwashing is a disciplined internal process that stress-tests every claim before it goes public. This requires both a clear decision framework and the governance structures to enforce it.

Before any environmental or climate statement leaves your organisation, run it through a structured review across six dimensions.

Specificity and quantification: Is the claim precise and measurable? "We are committed to sustainability" fails. "We reduced Scope 1 and 2 emissions by 22% versus 2020 baseline" passes. Vague, qualitative language is a red flag for auditors and regulators alike.

Time-boundedness: Does the claim include clear deadlines and interim milestones? Net-zero by 2050 alone is insufficient. Add near-term (2025-2030) and medium-term (2035-2040) targets with defined metrics and accountability mechanisms, as recommended by SBTi and the UN High-Level Expert Group.

Scope transparency: Does the claim cover the full organisational and value-chain footprint, or is it selectively narrow? If you're only addressing Scope 1 and 2 while Scope 3 represents 80% of total emissions, state that limitation explicitly. Hidden boundaries are a common greenwashing tactic.

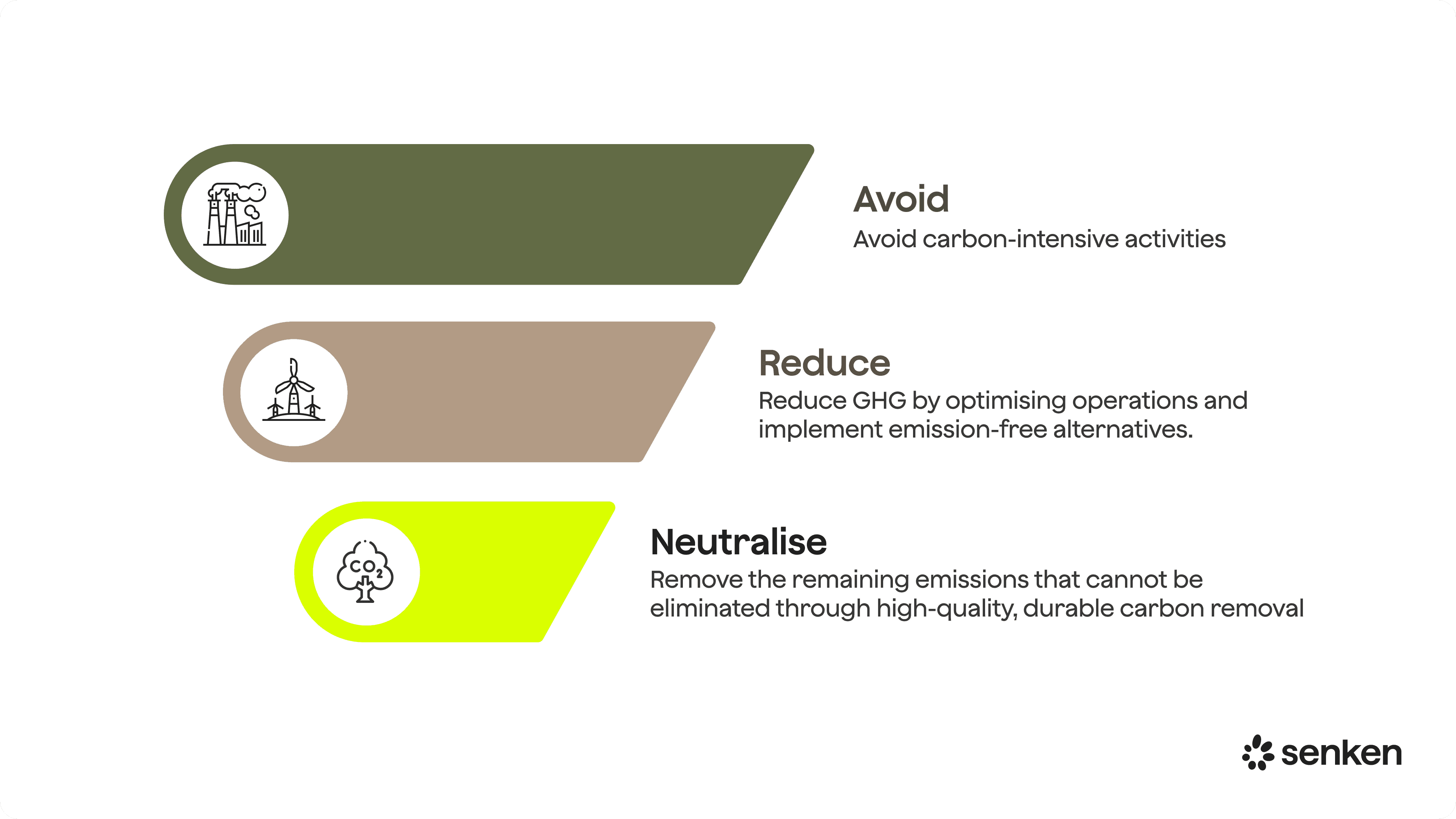

Reduction-first hierarchy: Does the claim prioritise in-house emissions reductions over compensation mechanisms like offsets? Credible climate strategies follow a mitigation hierarchy: avoid and reduce emissions first, then compensate only residual, hard-to-abate emissions with high-quality removals.

Data and methodology traceability: Can you provide a clear evidence trail from the claim back to underlying data, calculation methodologies, and third-party verification? If your CFO or external auditor asked for the substantiation file tomorrow, could you produce it within hours?

Carbon-credit quality checks (when offsets are involved): If the claim references carbon credits, can you demonstrate additionality (the project wouldn't have happened without carbon finance), permanence (storage duration >200 years for removals, per Oxford Principles), robust baselines (verified and not disputed), leakage mitigation, and third-party verification aligned with ICVCM Core Carbon Principles and VCMI Claims Code?

Convert this six-point checklist into a simple internal template. Require every major climate or environmental claim to pass through it, with sign-off from Sustainability, Legal, and Finance before publication.

Governance, sign-off and substantiation files that stand up to assurance

A good framework is useless without the governance structures to enforce it. Three elements make the difference.

Cross-functional claim review: Establish a standing working group with clear ownership from Sustainability (scientific credibility and data), Legal (compliance and liability), Communications (messaging and channels), and Finance (materiality and assurance). This isn't about slowing down; it's about ensuring the right expertise reviews claims before they create exposure. Use a RACI matrix to clarify who is Responsible, Accountable, Consulted, and Informed for each claim type.

Substantiation files: For every material environmental or climate claim, maintain a structured evidence file containing: the full claim text and where it appears; underlying data sources and calculations; methodology documentation; third-party verification or assurance reports; internal approval records; and any assumptions, limitations, or caveats. This file should be audit-ready and version-controlled. Under CSRD, your external assurance provider will request exactly this level of documentation.

Alignment with reporting cycles: Synchronise your communications calendar with your sustainability data close and reporting schedule. Avoid making new quantitative claims in the months before your annual report unless you have real-time data to back them. Many greenwashing risks emerge from mismatches between what Marketing says in Q1 and what Sustainability can actually substantiate when the report is finalised in Q2.

These governance steps help sustainability teams move from being the "department of no" to being the function that enables confident, ambitious climate storytelling because the evidence base is unassailable.

Using carbon credits without greenwashing: quality, transparency and how Senken helps

Carbon credits are not inherently greenwashing. The risk comes from poor project quality, weak integrity standards, and over-claiming their role in net-zero strategies. Used responsibly, carbon credits are a necessary tool for addressing residual emissions and scaling climate finance to the Global South.

Reduction-first, credits for residual only: Follow the mitigation hierarchy explicitly. Set science-based reduction targets (ideally validated by SBTi), prioritise operational and supply-chain decarbonisation, and use high-integrity carbon removals only for the emissions you genuinely cannot eliminate in the near term. This aligns with the Oxford Principles for Net-Zero-Aligned Offsetting and the UN HLEG recommendations.

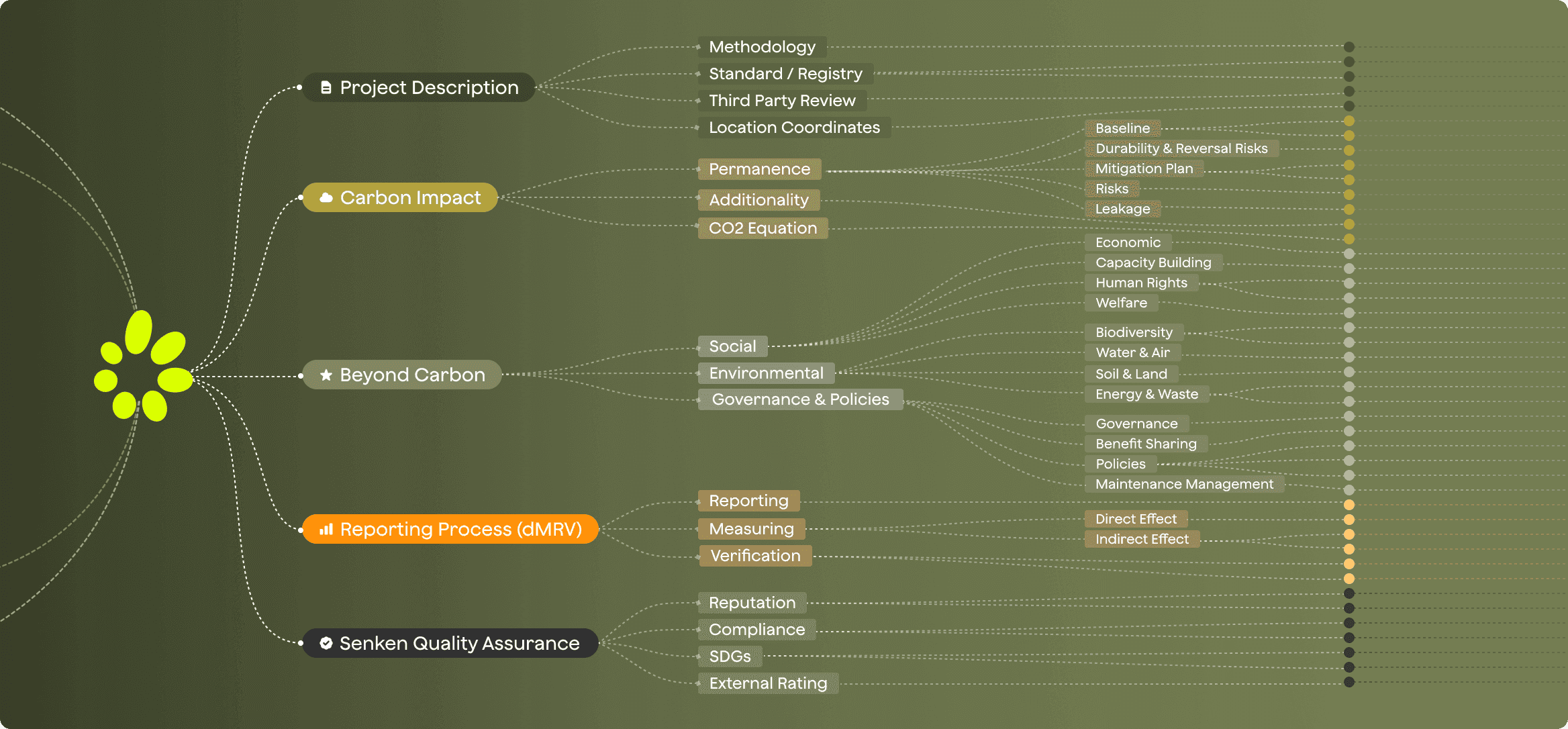

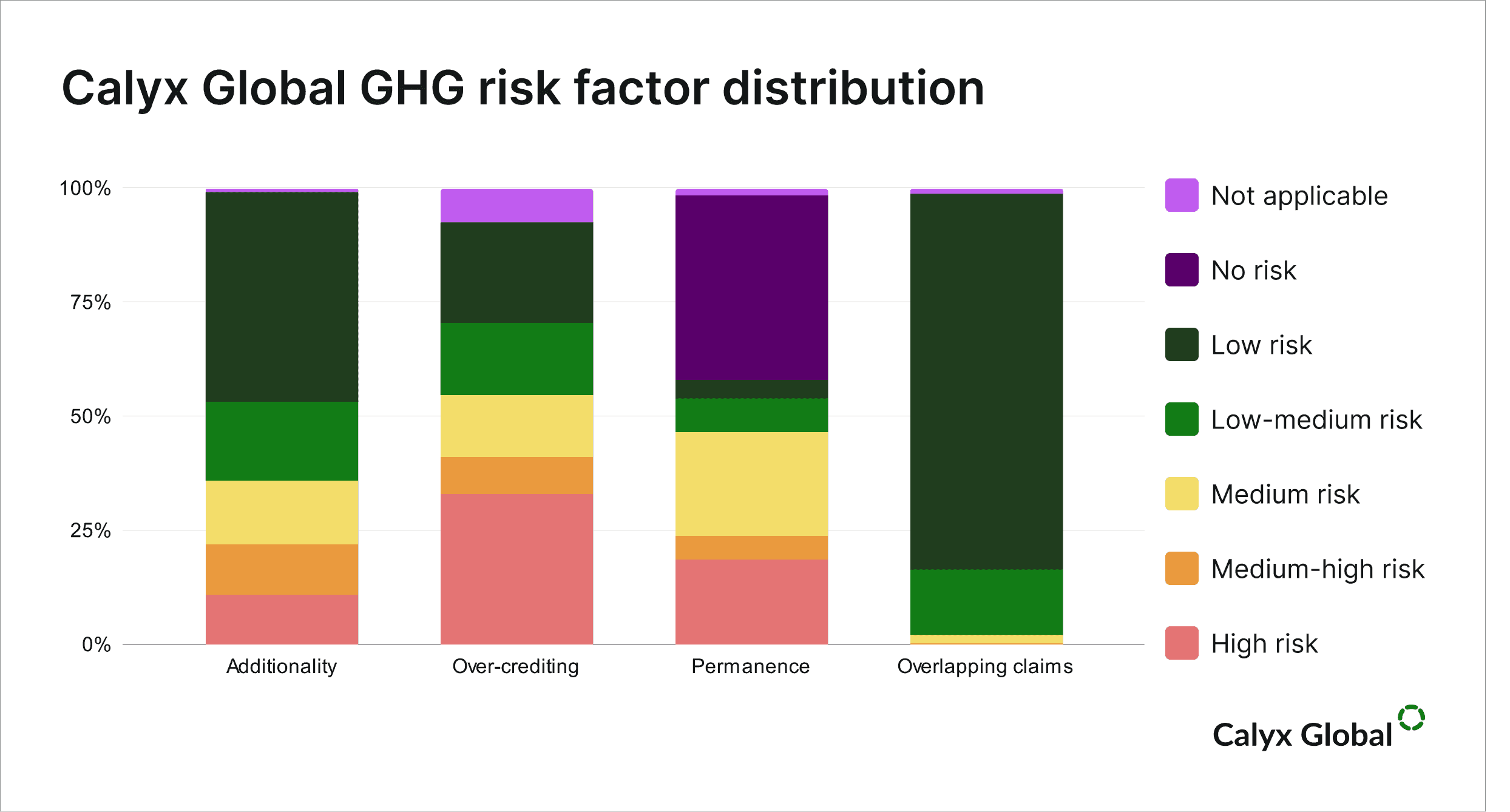

Uncompromising quality standards: Not all credits are created equal. The Max Planck Institute found that 84% of carbon credits are high-risk, and analysis of DAX40 companies showed 68% ended up supporting projects with no real climate impact. To evidence "high-integrity," layer multiple checks: independent verification by recognised registries (Verra, Gold Standard, Puro.earth), alignment with ICVCM Core Carbon Principles, positive ratings from third-party agencies (BeZero, Sylvera), robust digital MRV (measurement, reporting, verification), and adherence to VCMI Claims Code guidance on credit usage and communication. Senken's Sustainability Integrity Index operationalises this by assessing projects across 600+ data points spanning additionality, permanence, leakage, co-benefits, and compliance, accepting fewer than 5% of assessed projects into portfolios.

Full transparency and traceability: Publish detailed information about the credits you purchase: project names and locations, methodologies, vintage, registry serial numbers, verification bodies, and retirement records. Disclose this in your sustainability report and make supporting documentation available on request. Transparency is your strongest defence against greenwashing allegations and is increasingly expected under CSRD reporting standards.

This approach transforms carbon credits from a reputational liability into a credible component of your net-zero strategy. When you can show auditors, regulators, and boards that every credit in your portfolio meets rigorous integrity standards and is used only for residual emissions within a science-based transition plan, you de-risk your climate claims completely. Tools like Senken's evidence packs and portfolio design support exactly this: moving from opinion and marketing narratives to audit-ready, science-backed proof of impact.