ICVCM

Key Takeaways

- ICVCM's Core Carbon Principles now set the global quality floor for voluntary carbon credits. If a credit isn't CCP-labelled, treat it as higher risk, especially under CSRD assurance and stricter EU greenwashing rules.

- The real work is operational: map your existing portfolio against CCP status, rewrite RFP language to require CCP-Eligible programs and prioritise CCP-Approved categories, and design a phased transition away from legacy methodologies that will never meet the threshold.

- CCP-aligned credits support more credible CSRD disclosures, SBTi Beyond Value Chain Mitigation strategies, and VCMI claims—but they don't replace aggressive in-house emissions reductions or eliminate the need for project-level due diligence.

- With only ~4% of 2024 issuance CCP-approved and prices running ~25% higher in approved categories, early movers who embed ICVCM into procurement now will avoid last-minute supply crunches and reputational exposure from stranded low-quality holdings.

If you're leading sustainability for a large DACH company, you've probably heard "ICVCM" and "Core Carbon Principles" mentioned in the same breath as CSRD, SBTi, and the EU's new greenwashing rules—but what do they actually mean for your carbon credit strategy between now and 2030?

Here's the short version: the Integrity Council for the Voluntary Carbon Market (ICVCM) is an independent, non-profit governance body that has created a global quality benchmark for voluntary carbon credits through ten Core Carbon Principles (CCPs). Credits that meet these principles earn a CCP label in registries like Verra and Gold Standard; those that don't are increasingly seen as higher-risk by auditors, investors, and regulators. As of late 2025, only a small fraction of credits carry the label, but the programs covering ~98% of market volume are now CCP-Eligible, and 30+ methodologies across nature, methane, and removals have been approved.

Why does this suddenly matter? Because 84% of credits on the market are considered high-risk, 68% of DAX40 companies have bought low-impact projects, and the EU's Empowering Consumers Directive bans generic "climate neutral" claims from September 2026. German courts have already ruled against vague offset-based marketing, and CSRD assurance is tightening the screws on what counts as audit-ready evidence. ICVCM isn't a regulatory mandate—but it's fast becoming the de facto standard your board, auditors, and stakeholders expect you to reference when justifying carbon credit use in your net-zero strategy and public reporting.

This isn't a theory piece. It's a practical playbook for DACH sustainability leaders who need to operationalise ICVCM inside procurement policies, risk frameworks, and CSRD disclosures—without getting lost in acronyms or waiting for perfect clarity that won't come.

ICVCM in simple terms: what it is and why DACH corporates care now

The Integrity Council for the Voluntary Carbon Market (ICVCM) is an independent governance body that sets a global quality benchmark for voluntary carbon credits through ten Core Carbon Principles (CCPs). Think of it as the threshold standard: credits from programs and methodologies that meet the CCPs can carry a CCP label in registries like Verra or Gold Standard, signaling they've passed rigorous tests for additionality, permanence, quantification, and transparency. As of late 2025, only a small fraction of global issuance carries the CCP label, but the programs that are CCP-Eligible already cover roughly 98% of historical market volume by retirements.

For large DACH companies preparing for CSRD assurance starting this year, ICVCM matters because it provides an auditable, science-backed answer to a question your board, auditors, and legal teams are asking: how do you know your carbon credits are credible? The EU's Empowering Consumers Directive, entering force in September 2026, bans generic "climate neutral" claims based on unverified offsetting. Meanwhile, German courts have ruled that "climate neutral" is ambiguous and must be clarified in advertising. In this environment, referencing ICVCM and CCP status in your procurement policy and CSRD disclosures is one of the fastest ways to de-risk the use of carbon credits.

The stakes are real. Senken's analysis shows that 68% of DAX40 companies bought credits from projects delivering no real climate impact, and German firms alone wasted over €70 million on low-quality offsets in recent years. ICVCM's rejections of most legacy renewables methodologies and tightening of cookstove and REDD+ rules are the market's response. If a credit is not CCP-labelled today, you should treat it as higher risk and plan to phase it out or ring-fence it from future claims.

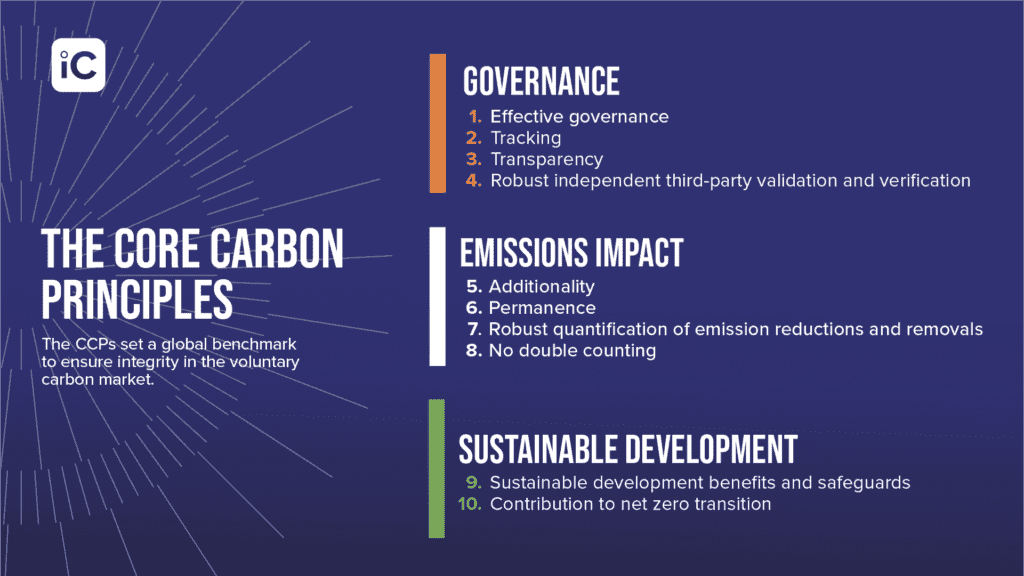

Core Carbon Principles: your new minimum quality bar for carbon credits

The 10 CCPs in three buyer-friendly buckets

The Core Carbon Principles break down into three clusters that map neatly to your due diligence checklist:

Governance & tracking: Programs must have effective governance (CCP 1), track credits in secure registries (CCP 2), ensure transparency with public documentation (CCP 3), and use robust independent third-party validation and verification (CCP 4). What this means for you: demand registry screenshots showing CCP labels, methodology version numbers, and auditor details. No transparency, no purchase.

Emissions impact & additionality: Credits must be robustly quantified (CCP 5), avoid double counting (CCP 6), be additional (CCP 8), and ensure permanence with compensation mechanisms for reversals (CCP 9). What this means for you: insist on conservative baselines, buffer pools that match reversal risk, and monitoring plans that extend over 100 years for nature-based projects or use geological storage for engineered removals.

Sustainable development & safeguards: Projects must deliver sustainable development benefits and safeguards (CCP 7) and contribute to net-zero transition without locking in high-carbon pathways (CCP 10). What this means for you: look for co-benefits documentation, community engagement evidence, and alignment with SDGs. Avoid projects that displace emissions problems or undermine Paris-aligned policy.

How to read CCP labels: CCP-Eligible vs CCP-Approved

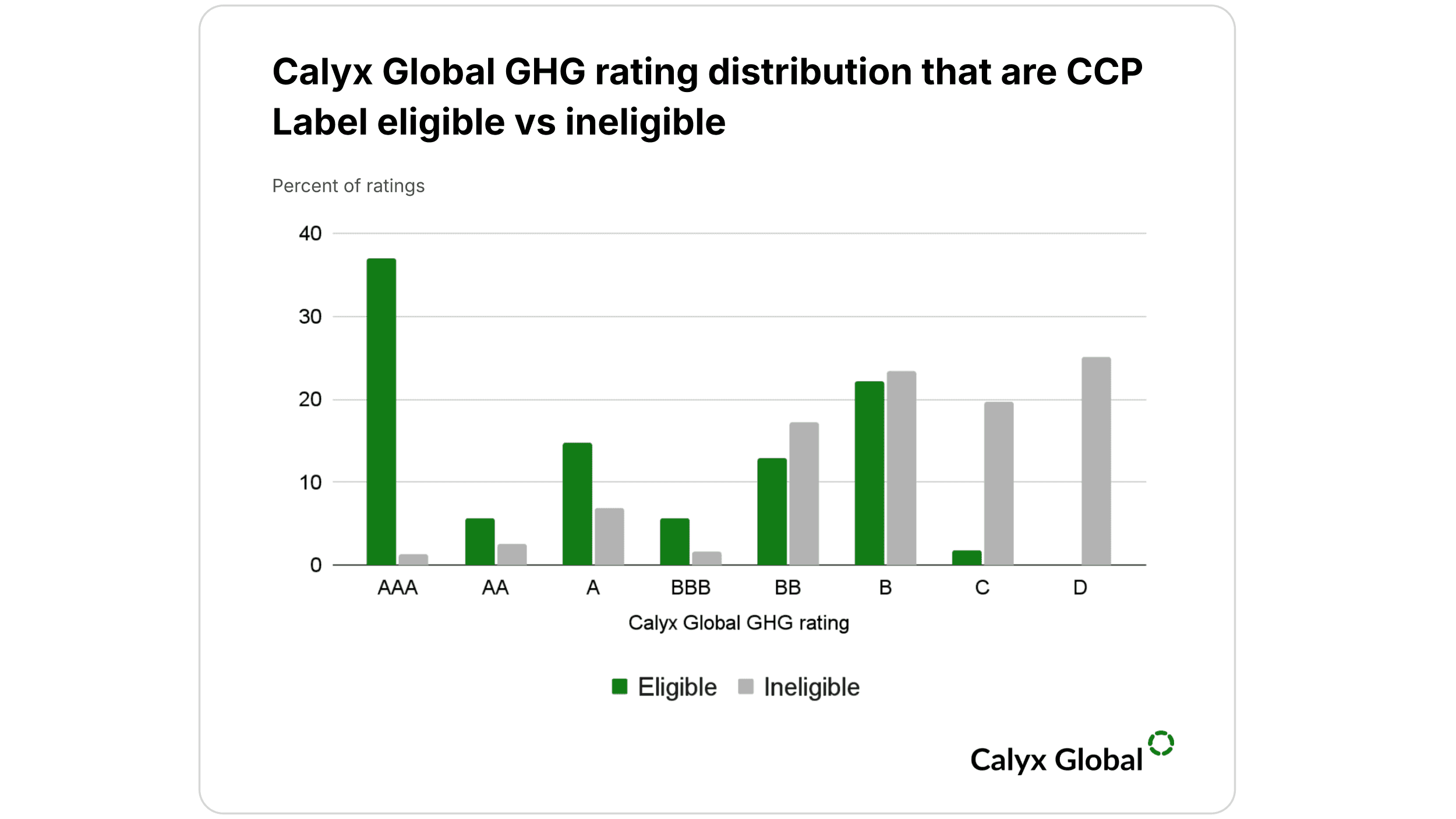

ICVCM uses a two-tick system. First, a crediting program (Verra, Gold Standard, ACR, CAR, ART, Isometric) must be CCP-Eligible at the program level, meaning its rules, governance, and registry meet CCPs 1 to 4. Second, specific methodologies or categories within that program must be CCP-Approved, confirming they meet all ten CCPs including additionality and permanence. Only when both ticks are in place can issued credits carry the CCP label in the registry.

Examples help: Verra's landfill gas methodologies (ACM0001, AMS-III.G) are CCP-Approved, so credits from Verra landfill projects using those versions can be labelled. Verra's VM0048 REDD+ methodology is also approved, but many older REDD+ approaches are still under assessment or rejected. Gold Standard's metered cookstove methodology is approved; simplified approaches that lack rigorous monitoring are not. Isometric's biochar and Direct Air Capture pathways are approved, reflecting high permanence and MRV standards. Meanwhile, ICVCM explicitly rejected most grid-connected renewables methodologies, removing a large chunk of legacy supply from eligibility.

Your internal rule of thumb: no CCP label means no high-integrity claim. But even with a CCP label, you still need project-level due diligence. ICVCM sets the floor; independent ratings, developer track records, and local safeguards checks remain essential to manage residual risk.

What ICVCM changes in your carbon credit strategy for 2025–2030

Start with a portfolio health check. If your current holdings lean heavily on pre-2020 renewables (wind, solar, hydro) or simplified cookstoves, you're sitting on credits that ICVCM has either rejected or placed under tighter scrutiny. These won't receive CCP labels and are increasingly seen by auditors, investors, and NGOs as reputational liabilities. For CSRD reporting, you'll need to explain why you hold them and how they fit (or don't fit) into your transition plan and target accounting.

Market data confirms the shift. S&P Global recorded only 13.16 million CCP-approved credits issued in 2024, roughly 4% of total issuance. Ecosystem Marketplace found that CCP-approved categories like landfill gas saw prices rise about 35% in H2 2024, with volumes up 149% year-on-year as buyers chased quality. ICVCM's own 2025 Impact Report cites an average 25% price premium for CCP-labelled credits.

Three strategic shifts to plan now:

Prioritise CCP-approved categories even at a premium. Accept that high-integrity credits cost more and that availability is limited. Build procurement budgets around €20–50/tonne for nature-based CCP-approved projects and €50–250+ for durable removals like biochar or enhanced weathering. Lock in multi-year offtakes where possible to secure supply and stabilise costs.

Redefine "acceptable" for the board. Update your carbon credit policy to state that CCP-Eligible programs and CCP-Approved categories are your baseline, not an aspiration. Make it clear that non-CCP credits are transitional holdings, not strategic assets. This shift in internal language matters when procurement, legal, and communications are aligning on RFPs and external claims.

Design a managed transition, not a cliff edge. If you have multi-year contracts for non-CCP credits, map expiry dates and plan replacement procurement 18 to 24 months ahead. Use non-CCP holdings for internal footprint accounting where transparency permits, but avoid tying them to public claims or SBTi/VCMI frameworks. By 2027, aim for a portfolio that is majority CCP-aligned and fully CCP-compliant by 2030.

Step 1: Map and rate your existing portfolio against ICVCM

Pull a full list of credits you've purchased or retired since 2023. For each batch, record the registry, program, project ID, methodology, vintage, and volume. Cross-reference against ICVCM's Assessment Status page to tag each holding as CCP-Approved, CCP-Eligible (program only), under assessment, or does not meet. If you're holding Verra ACM0002 renewables or AMS-I.D cookstoves, flag them as non-CCP and schedule a conversation with procurement and legal about how to handle them in your next CSRD report.

Run this exercise as a joint session with procurement, sustainability, and risk. The output should be a simple portfolio dashboard: X tonnes CCP-approved, Y tonnes CCP-Eligible but category pending, Z tonnes non-CCP. Use this to set a phase-out target, for example 80% CCP-aligned by end 2026, 100% by 2030.

Step 2: Rewrite policies, RFPs and supplier questionnaires

Your procurement policy should now include a mandatory ICVCM clause: "All carbon credits must originate from CCP-Eligible programs. Credits from CCP-Approved categories receive priority; non-CCP credits require written justification and executive sign-off, and may only be used for internal accounting, not public claims."

In RFPs, add these questions for suppliers:

- Confirm the program (Verra, Gold Standard, ACR, etc.) and its CCP-Eligibility status.

- Provide the methodology name and version, and confirm CCP-Approved status or explain if under assessment.

- Supply registry evidence (serial numbers, retirement certificates) showing CCP labels where applicable.

- Disclose any project-level controversies, rating agency scores, and permanence/reversal insurance arrangements.

- Describe MRV approach, verification body accreditation, and monitoring frequency.

Include a standard contract clause requiring replacement or refund if a project loses CCP approval, is decertified, or suffers uncovered reversal. Senken's clients use this language to protect against stranded assets and shifting ICVCM decisions.

Step 3: Design a CCP-first portfolio and phased transition plan

Build your forward procurement around a 70/30 or 60/40 split: durable removals (biochar, enhanced weathering, DAC) for long-term credibility and nature-based solutions (ARR, IFM, regenerative agriculture) for cost efficiency and co-benefits. All projects must be CCP-approved or on a clear path to approval.

For existing non-CCP holdings, create three buckets. Bucket A (use with transparency): high-quality non-CCP credits where methodology updates are pending; disclose them in CSRD as transitional, with a note that they do not carry CCP labels. Bucket B (ring-fence): legacy credits you'll retire for internal accounting but not link to public claims or SBTi beyond value chain mitigation. Bucket C (phase out): low-integrity or reputationally risky credits; stop retiring them and let contracts expire without renewal.

Set quarterly checkpoints to review ICVCM's updated assessment status and adjust procurement priorities. Market intelligence from Senken or rating agencies can help you spot emerging CCP-approved supply before it sells out.

Step 4: Set up monitoring, documentation and internal governance

Establish a simple internal system to track CCP status: a shared spreadsheet or module in your ERP that logs program, category, methodology version, CCP label status, and registry link for every credit batch. Update this each quarter as ICVCM publishes new decisions.

Assign ownership: your Head of Sustainability should chair a quarterly carbon credit governance meeting with procurement, legal, finance, and communications. Agenda items: portfolio CCP status, upcoming RFPs, claim language review, CSRD data pack updates. Minutes and decisions should be documented for audit trails.

For CSRD, your evidence pack should include: procurement contracts, registry retirement certificates with CCP labels visible, methodology documentation, verification reports, and a narrative explaining your CCP-first policy and transition plan. Senken automates much of this by delivering CSRD-ready documentation bundles with each purchase, saving weeks of manual evidence gathering.

Using ICVCM to strengthen CSRD, SBTi/BVCM and VCMI reporting

ESRS E1 requires you to report gross Scopes 1, 2, and 3 separately, then disclose any "GHG mitigation projects financed through carbon credits" in a distinct line (E1-7). Credits cannot be netted against your gross emissions. You must describe the nature of the projects (avoidance vs removals), quantities, vintages, registries, and whether you've applied recognised quality standards.

Here's where ICVCM comes in. State in your disclosure: "We apply the ICVCM Core Carbon Principles as our quality benchmark. X% of credits retired in [year] are CCP-approved; the remainder are CCP-Eligible (program-level) and under methodology assessment, or held as transitional assets with no associated public claims." This language shows auditors and investors that you have a coherent quality framework and a plan, reducing greenwashing risk.

Document everything. Attach registry screenshots showing CCP labels, link to ICVCM assessment status, and include a short table mapping your portfolio to CCP categories. This audit-ready pack proves you've done due diligence and aren't relying on marketing materials.

SBTi and Beyond Value Chain Mitigation: where CCP-aligned credits fit

SBTi's Net-Zero Standard 2.0 draft, expected to finalise in 2025–2026, introduces interim removal targets starting at roughly 0.5–2.8% of total emissions in 2030, scaling to 10% by 2050. While SBTi's near-term targets focus on in-boundary reductions, Beyond Value Chain Mitigation (BVCM) allows companies to finance mitigation beyond their own value chains as a voluntary complement. CCP-aligned credits are emerging as the quality floor for any BVCM investments.

What this means in practice: you cannot use credits to meet your SBTi near-term reduction targets. But if you're financing removals or high-quality avoidance as part of your broader climate contribution, CCP-approved credits are the minimum standard to cite credibly. Document the volumes separately in your SBTi progress report, note that they are additional to your target pathway, and reference ICVCM to justify quality.

VCMI claims: combining supply-side CCPs with demand-side rules

The Voluntary Carbon Markets Initiative (VCMI) defines claims that companies can make when using carbon credits (for example, "Carbon Neutral", "Net Zero Aligned"). VCMI explicitly requires credits to meet high-integrity supply-side standards, and ICVCM's CCPs are the recognised benchmark. To make a VCMI claim, you also need to meet demand-side conditions: aggressive decarbonisation aligned with 1.5°C, transparent reporting, and regular updates.

The practical takeaway: CCP-approved credits are necessary but not sufficient for VCMI claims. You also need to show rapid emissions reductions, a credible transition plan, and proper disclosure under CSRD or equivalent frameworks. Combining CCP-aligned procurement with VCMI claim architecture gives you a defensible, joined-up narrative for investors and customers.

A final note on EU consumer law: even with CCP-approved credits, generic "carbon neutral" labels on consumer products are banned under the Empowering Consumers Directive unless you can demonstrate outstanding environmental performance across the product's life cycle. CCP labels help substantiate your claim, but they don't make broad neutrality claims automatically safe. Be precise, be specific, and keep legal counsel in the loop.

Managing non-CCP credits and working with partners like Senken

You'll inevitably face non-CCP credits, whether legacy holdings or supply gaps in niche geographies. Here's a pragmatic decision framework. Use with transparency: if a project is high-quality and the methodology is under ICVCM assessment or a program update is pending, you can retire these credits for internal footprint accounting and disclose them in CSRD with clear language that they do not yet carry CCP labels. Reframe: shift your narrative from "offsets" to "financed mitigation" or "climate contribution," separating these credits from core decarbonisation claims. Ring-fence: allocate non-CCP holdings to past commitments or internal purposes, but don't tie them to forward-looking SBTi or VCMI frameworks. Phase out: for credits rated poorly by agencies like BeZero or Sylvera, or projects with known controversies, stop retiring and let contracts expire.

The challenge is supply. Senken's internal analysis shows that fewer than 5% of projects meet its 600+ datapoint Sustainability Integrity Index threshold, which goes beyond ICVCM's minimum to assess leakage, community safeguards, biodiversity co-benefits, and developer reputation. Market research confirms tight high-quality supply and rising prices, making early, structured transition planning essential. Waiting until 2027 or 2028 to pivot means last-minute panic buying at premium prices with limited choice.

This is where a partner like Senken can operationalise ICVCM for you. Senken's five-step verification process starts with basic project details (methodology, registry, location), then layers in 350 datapoints on carbon impact (additionality, permanence, quantification), 105 on beyond-carbon benefits (social, environmental, governance), 90 on reporting and MRV transparency, and 78 on compliance and reputation, including explicit checks against ICVCM CCP status and CSRD readiness. The result: a pre-screened portfolio where every project is CCP-aligned and built for audit scrutiny, with CSRD-ready documentation delivered as standard.

Senken also manages the procurement complexity. You get access to CCP-approved supply across biochar, enhanced weathering, ARR, IFM, and regenerative agriculture; multi-year offtake agreements that lock in price and volume; and impact dashboards that translate technical MRV data into board-ready visuals. Clients like Vodafone Germany and Deutsche Telekom use Senken to balance scientific rigour with practical procurement constraints, confident that their portfolios will stand up to evolving ICVCM assessments, CSRD assurance, and stakeholder scrutiny.

The shift to CCP-aligned credits isn't just about compliance. It's about building a portfolio that supports your long-term climate strategy, protects your brand, and aligns with the direction of European regulation and investor expectations. ICVCM provides the framework; partners like Senken help you implement it at pace, with confidence, and without the operational burden of doing it all in-house.