Blue Carbon

Key Takeaways

- Blue carbon refers to carbon captured and stored by coastal ecosystems like mangroves, salt marshes, and seagrass, with soil carbon that can remain locked away for centuries to millennia.

- Blue carbon credits are a tiny but fast-growing segment of the voluntary carbon market (<1% of issuances), with limited project supply and premium prices typically in the mid‑$20s to low‑$30s per tCO2e.

- Scientific and MRV complexity means only a minority of blue carbon projects currently meet high-integrity thresholds; robust due diligence is essential to avoid greenwashing and future write-offs.

- For DACH corporates, blue carbon fits into Beyond Value Chain Mitigation and Oxford-aligned portfolios as a smaller, high-quality slice that combines climate mitigation with adaptation and biodiversity co-benefits.

- Sustainability leaders should define clear quality criteria, use multi-layer verification (including tools like Senken's Sustainability Integrity Index), and consider multi-year offtakes to secure scarce, premium blue carbon supply.

Blue carbon is carbon captured and stored by coastal vegetated ecosystems – specifically mangroves, salt marshes, and seagrass meadows – whose waterlogged soils lock carbon away for centuries to millennia. These ecosystems sequester carbon at rates comparable to or exceeding tropical forests, storing most of it belowground where low-oxygen conditions prevent decomposition. For DACH sustainability leads navigating CSRD audits, SBTi scrutiny, and internal risk committees, blue carbon represents both an opportunity and a minefield: a premium nature-based solution with strong co-benefits, but one where quality varies wildly and only a fraction of projects will survive rigorous due diligence.

This guide starts with the science – what blue carbon is, how these ecosystems work, and why they matter for climate mitigation. Then we move quickly into what matters for your strategy: integrity risks in the voluntary carbon market, current pricing and supply dynamics, and a practical roadmap to integrate blue carbon credits into Oxford-aligned, Beyond Value Chain Mitigation portfolios using the kind of multi-layer verification that keeps your claims defensible and your portfolio audit-ready.

What is Blue Carbon

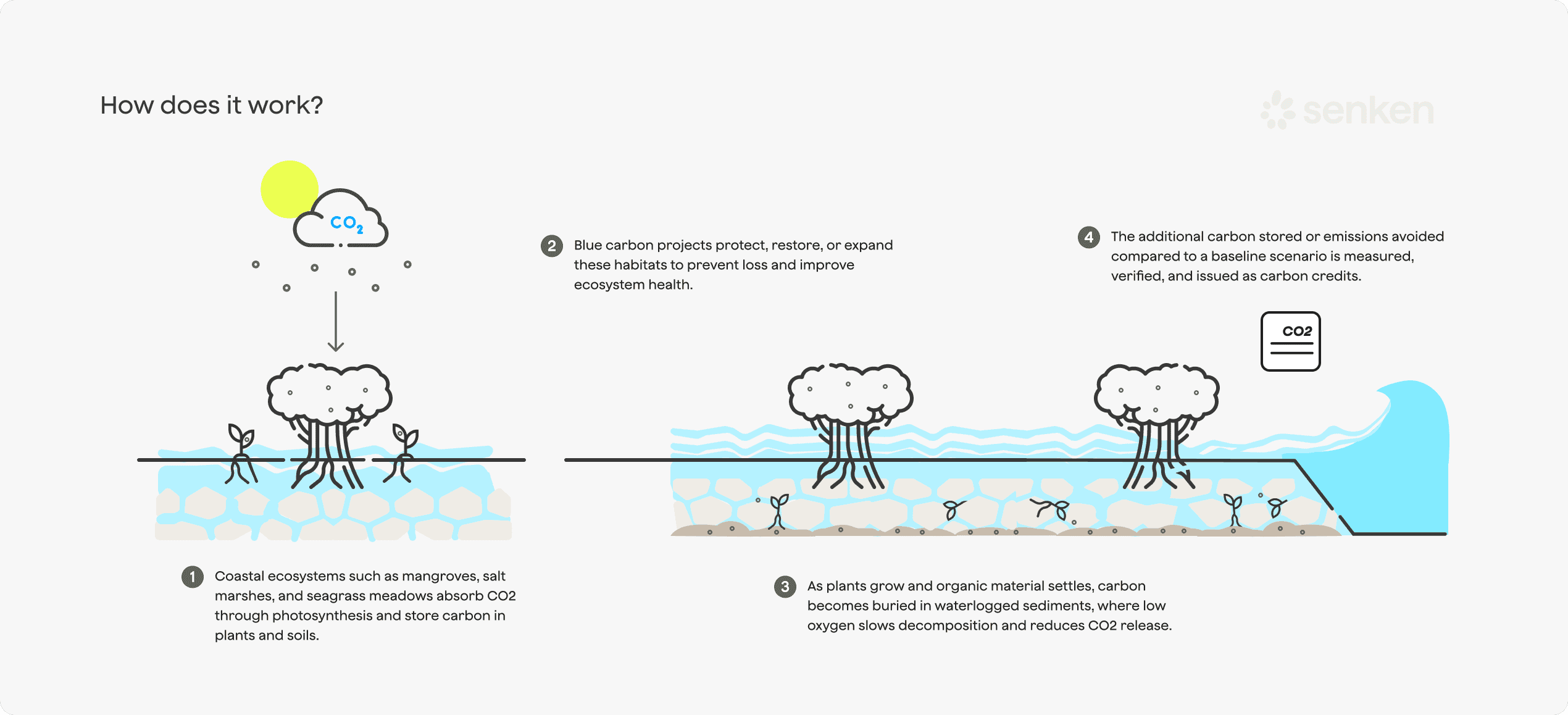

Blue carbon refers to carbon captured and stored by coastal and marine vegetated ecosystems, specifically mangroves, tidal salt marshes, and seagrass meadows. Unlike the broader ocean carbon cycle, blue carbon focuses on the thin coastal fringe where carbon sequestration can be measured, verified, and credited. These ecosystems trap atmospheric CO2 through photosynthesis and lock it away in waterlogged, oxygen-poor soils and sediments for centuries to millennia.

For corporate climate strategies, blue carbon matters because it combines high per-hectare sequestration rates with exceptionally long storage times. Independent scientific syntheses from NOAA and the Blue Carbon Initiative show that these coastal ecosystems store roughly three to five times more carbon per hectare than many terrestrial forests, with the majority held in soils rather than visible plant biomass. This makes them powerful tools for Beyond Value Chain Mitigation when integrated into credible, Oxford-aligned net zero portfolios.

The relevance to your role is straightforward. Blue carbon credits offer a defensible, high-integrity option that can survive CSRD audits, SBTi scrutiny, and board-level risk reviews, provided you apply robust due diligence. The challenge is that this is a scientifically complex and market-immature segment. Only a minority of blue carbon projects currently meet the integrity thresholds you need, so your procurement strategy must start with clear quality criteria and multi-layer verification.

What Are Blue Carbon Ecosystems

Three primary coastal ecosystems are recognized in carbon credit methodologies: mangroves, tidal salt marshes, and seagrass meadows. Each has distinct ecological characteristics, but they share the capacity to trap carbon in waterlogged sediments where decomposition is drastically slowed.

Mangroves and Blue Mangrove Forests

Mangroves are salt-tolerant trees and shrubs found along tropical and subtropical coastlines. Their dense root systems stabilize sediments and create low-oxygen environments where organic matter accumulates rather than decomposing. Mangrove soils can store carbon for millennia, making them the dominant source of blue carbon credits today. Projects like Delta Blue Carbon in Pakistan (the world's largest blue carbon initiative, covering ~350,000 hectares) and Vida Manglar in Colombia (the first to fully quantify and monetize mangrove carbon under Verra) demonstrate the scale and rigor possible in this category.

Tidal Marshes and Salt Marshes

Tidal marshes, often called salt marshes in temperate zones, are vegetated wetlands flooded regularly by tides. They occur in North America, Europe, Australia, and other temperate coastlines. The grasses and sedges that dominate these ecosystems build thick organic soils over time. While individual marsh plants may only live a few years, the carbon they capture can remain locked in sediment for centuries. Tidal marsh restoration projects are emerging under methodologies like Verra's VM0033 and Australia's ACCU tidal restoration method, though they remain a smaller share of the market than mangroves.

Seagrass Meadows

Seagrasses are underwater flowering plants found in shallow coastal waters across both tropical and temperate regions. They grow on sandy or muddy seafloors and trap organic particles in their root mats and surrounding sediments. Seagrass meadows are highly productive carbon sinks, but they are also extremely vulnerable to dredging, pollution, and warming waters. Crediting seagrass projects requires specialized MRV, and the number of active projects is still limited compared to mangrove and marsh initiatives.

Is Kelp a Blue Carbon Ecosystem

Kelp forests sequester carbon through rapid growth, but they are not consistently included in blue carbon accounting. The challenge is permanence. When kelp dies, much of its biomass is transported by currents and may decompose in the water column rather than accumulating in sediments. Scientific and accounting uncertainties around long-term storage mean that kelp is not yet creditable under most blue carbon methodologies. If kelp projects appear in your pipeline, treat them as experimental and ask for robust evidence on storage pathways before committing budget.

How Blue Carbon Ecosystems Store Carbon

Understanding the storage mechanism is essential for evaluating project quality and permanence. Blue carbon ecosystems don't just capture CO2; they lock it in place through a combination of biological uptake and geological processes.

Carbon Sequestration in Coastal Sediments

The majority of blue carbon is stored belowground. Plants take up CO2 through photosynthesis, but in waterlogged coastal soils, the lack of oxygen prevents organic matter from decomposing quickly. Dead roots, leaves, and trapped organic particles accumulate in layers of sediment. Over time, these layers build up meters of carbon-rich soil. Disturbance, whether from dredging, drainage, or development, can expose these sediments to oxygen and rapidly release centuries of stored carbon back to the atmosphere.

Aboveground vs Belowground Carbon Storage

The table below summarizes where carbon is held in blue carbon ecosystems and the relative permanence of each pool:

| Storage Pool | Description | Permanence |

|---|---|---|

| Aboveground biomass | Stems, leaves, and branches of mangroves, marsh grasses, or seagrass shoots | Short term (<50 years) |

| Belowground biomass | Roots and rhizomes anchoring plants in sediment | Medium term (50-100 years) |

| Sediment and soil carbon | Organic matter accumulated in waterlogged, low-oxygen soils over centuries | Long term (100s to 1000s of years) |

For corporate buyers, the key takeaway is that the long-lived storage is in the soil. Projects that focus only on aboveground biomass or fail to protect sediments from disturbance are higher risk.

How Biosequestration Works in Coastal Systems

Biosequestration in blue carbon ecosystems is the process by which plants absorb CO2 from the atmosphere and convert it into organic carbon through photosynthesis. In coastal settings, this carbon is then trapped in sediments where microbial activity is suppressed by low oxygen levels. The result is a natural carbon capture and storage system that can operate for millennia, as long as the ecosystem remains intact and hydrologically connected to tidal flows. This durability is what makes blue carbon attractive for portfolio strategies that emphasize permanence and co-benefits alongside emission reductions.

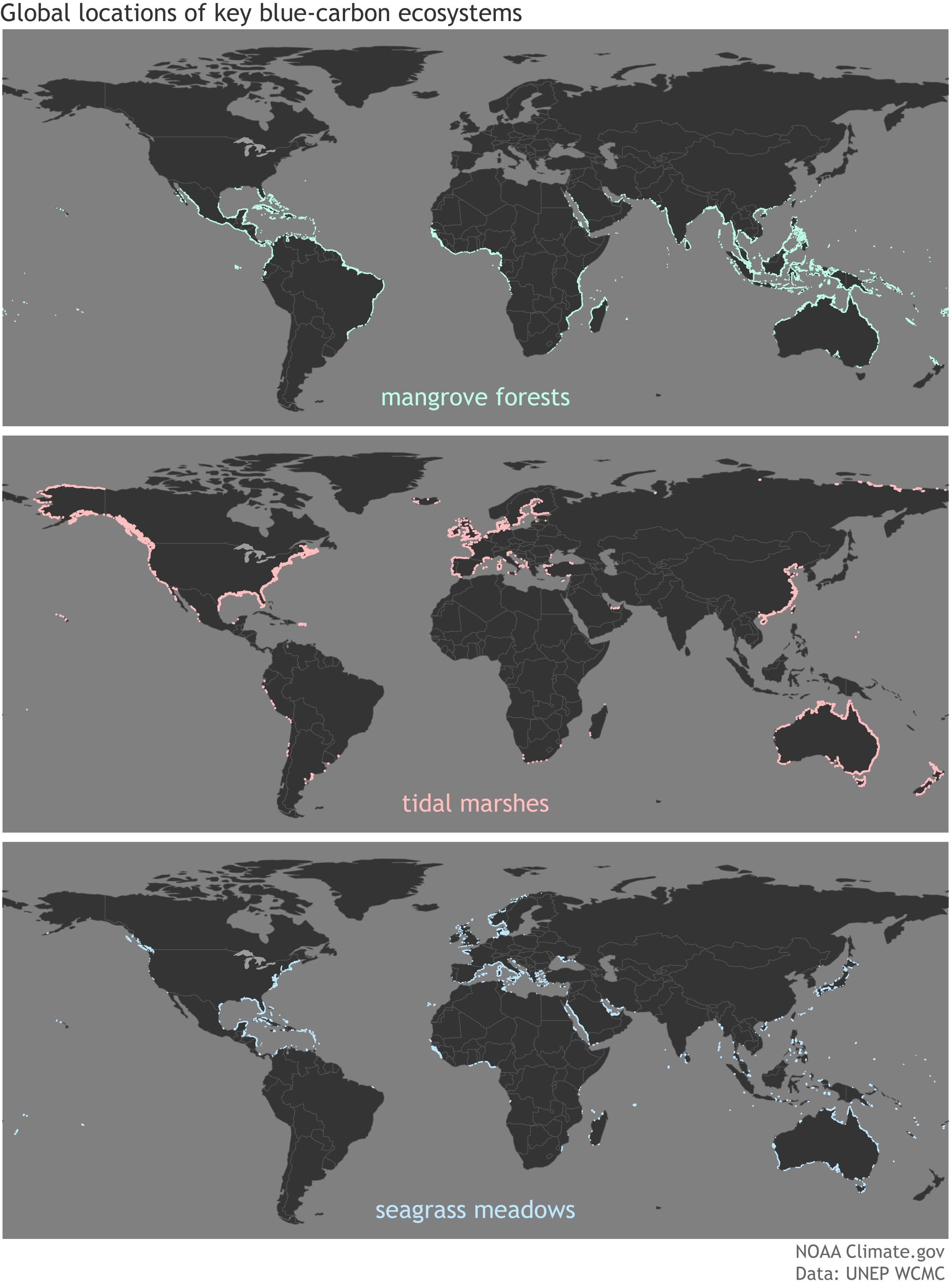

Where Are Blue Carbon Ecosystems Found

Blue carbon ecosystems are geographically concentrated in specific coastal zones, which has implications for project sourcing, regional diversification, and co-benefit alignment.

Tropical and Subtropical Coastlines

Mangroves thrive along tropical and subtropical coasts, with major concentrations in Southeast Asia (Indonesia, Thailand, Vietnam), West Africa (Nigeria, Senegal), Latin America (Colombia, Brazil, Ecuador), and parts of Oceania. These regions host the largest mangrove forests and, consequently, the majority of blue carbon projects in the market today. Projects like Delta Blue Carbon in Pakistan's Indus Delta and Vida Manglar in Colombia's Cispatá Bay illustrate how large-scale restoration and conservation can be combined with community governance and revenue-sharing models.

Temperate Coastal Regions

Salt marshes and some seagrass meadows are found in temperate zones, including the Atlantic coasts of North America and Europe, the coasts of southern Australia and New Zealand, and the temperate waters of East Asia. These systems support high carbon storage but face pressures from coastal development, agriculture, and pollution. Temperate blue carbon projects are emerging under standards like Verra's VM0033 and national compliance schemes such as Australia's ACCU tidal restoration method.

Global Hotspots for Blue Carbon

Several regions stand out as blue carbon hotspots where high storage capacity and project viability converge: the Sundarbans spanning India and Bangladesh, the deltas of major rivers in Southeast Asia, the Caribbean mangrove belts, and the extensive coastal wetlands of East Africa. Many of these hotspots lie in emerging markets, making carbon finance a potentially catalytic source of funding for coastal protection, just transition, and community development. For DACH corporates focused on ESG narratives that include social and biodiversity co-benefits, these geographies offer compelling stories alongside climate impact.

Blue Carbon vs Green Carbon

Green carbon refers to carbon stored in terrestrial ecosystems like forests, grasslands, and agricultural soils. Blue carbon is the coastal counterpart. Both are essential for climate mitigation, but they differ in sequestration speed, storage location, area, and vulnerability.

Blue carbon ecosystems often sequester carbon faster per hectare and store more of it in long-lived sediments. However, they cover far less area globally and are highly vulnerable to disturbance and development. A single drainage project or coastal construction can release centuries of stored carbon within years. Green carbon projects, by contrast, typically spread across larger landscapes and face different risk profiles such as fire, pests, and land-use change.

For corporate portfolios, blue carbon should be positioned as complementary to, not a replacement for, terrestrial projects. It functions as a high-integrity, high-co-benefit slice that supports adaptation and biodiversity narratives alongside other nature-based and technological removals. The Oxford Principles emphasize gradually increasing the share of long-lived removals over time; blue carbon management, with its intermediate durability (up to 1,000 years), fits naturally into this transition strategy alongside reforestation, peatland restoration, and early-stage tech removals like biochar and enhanced weathering.

What Are the Threats to Blue Carbon Ecosystems

Blue carbon ecosystems face multiple, interconnected threats that sustainability leaders must understand in order to assess project additionality and permanence risk.

Coastal Development and Habitat Conversion

The most direct threat is physical conversion: mangroves cleared for aquaculture ponds, marshes drained for agriculture, seagrass beds dredged for ports or tourism infrastructure, and wetlands filled for urban expansion. These activities not only halt future carbon sequestration but also disturb sediments, rapidly releasing stored carbon. This "double impact" is a core rationale for avoided-loss blue carbon projects, which demonstrate that without intervention and carbon finance, conversion would proceed.

Climate Change and Sea Level Rise

Climate-driven pressures include sea level rise that can drown ecosystems if they cannot migrate inland (often blocked by development), warming waters that stress species, and increased storm intensity that can erode or physically destroy habitats. Blue carbon projects must account for these long-term risks in their permanence planning, including buffer pools and adaptive management strategies.

Pollution and Water Quality Degradation

Nutrient loading from agricultural runoff, sedimentation from upstream land clearing, and industrial contaminants all reduce ecosystem health and carbon sequestration capacity. Poor water quality can weaken plant growth, increase disease, and shift community composition toward less productive species. Projects in heavily impacted watersheds carry higher baseline and permanence risks.

What Happens When Blue Carbon Ecosystems Are Destroyed

When blue carbon ecosystems are destroyed, they shift from carbon sinks to significant sources. Centuries of stored soil carbon can be released within a few years through oxidation, microbial decomposition, and erosion. This loss is essentially irreversible on human timescales. For buyers, this underscores why additionality, permanence guarantees, and robust monitoring are non-negotiable in blue carbon project due diligence.

Benefits and Challenges of Protecting Blue Carbon

Blue carbon projects deliver compelling co-benefits but come with scientific and operational complexity that requires careful evaluation.

Co-benefits Beyond Carbon Sequestration

Blue carbon ecosystems provide coastal protection by buffering storm surges and reducing erosion, support fisheries by serving as nursery habitats, improve water quality through filtration, and maintain high biodiversity. Many projects also generate direct livelihood benefits for coastal communities, from sustainable fisheries to eco-tourism to project employment. For corporates seeking credits that align with adaptation, nature, and SDG narratives, these co-benefits are a strategic advantage. However, they also mean that exaggerated or unverified co-benefit claims can amplify reputational risk if projects underdeliver.

Scientific Measurement Challenges

Measuring blue carbon is technically demanding. Soil carbon stocks vary spatially even within a single project site, requiring intensive sampling and modeling. Baselines differ across geographies, and long-term datasets are limited in some regions. Projects must model complex soil carbon dynamics, track land-use change and leakage (e.g., aquaculture shifting to adjacent areas), and maintain rigorous MRV over decades. Independent market analyses from agencies like BeZero and Calyx Global note that only a subset of blue carbon projects are actively issuing credits, and quality varies widely.

Verification and Credibility Concerns

Even technically sound projects can face credibility challenges if MRV is opaque, if baseline assumptions are aggressive, or if there are governance or tenure disputes. Recent scrutiny from ratings agencies and bodies like ICVCM has raised the bar for what constitutes a high-integrity blue carbon credit. For buyers, this means that registry labels alone are insufficient. You need multi-layer verification, including independent ratings, methodology-level approval (such as ICVCM Core Carbon Principles), and ideally a platform or partner that evaluates hundreds of data points per project to identify the top performers.

Blue Carbon in the Voluntary Carbon Market

Blue carbon remains a tiny but fast-growing segment of the voluntary carbon market, characterized by limited supply, premium pricing, and evolving standards.

How Blue Carbon Credits Work

Blue carbon credits are typically generated through two pathways: conservation or avoided loss (preventing emissions from ecosystem destruction) and restoration or new sequestration (replanting and hydrological restoration). Each credit represents one metric ton of CO2 equivalent either avoided or removed. The credits are verified, issued, and tracked through registries, then retired by buyers to support net zero or beyond value chain mitigation claims. Because most blue carbon storage is in soils, the MRV must account for sediment carbon stocks, growth rates, and long-term permanence, making the process more data-intensive than many terrestrial forest projects.

Major Standards and Certification Bodies

Several standards and methodologies govern blue carbon crediting:

- Verra VCS operates VM0033 (Methodology for Tidal Wetland and Seagrass Restoration), which is widely used for mangrove, tidal marsh, and seagrass projects. Verra also enables blue carbon conservation under REDD+ frameworks. Roughly 99% of blue carbon issuance to date has been through Verra-registered projects, predominantly mangroves.

- American Carbon Registry (ACR) offers coastal and deltaic wetland restoration methodologies applicable to avoided loss, hydrologic management, and afforestation/reforestation of wetlands.

- Plan Vivo certifies community-led projects, including pioneering blue carbon examples like Mikoko Pamoja in Kenya, where 117 hectares of mangrove deliver ~2,000 tCO2e per year with proceeds reinvested in local development.

- Gold Standard released a Sustainable Management of Mangroves methodology in 2024, adding a new pathway for mangrove projects under its registry.

- National compliance schemes like Australia's ACCU Scheme include a tidal restoration method for blue carbon ecosystems, enabling issuance of compliance-grade credits.

- BCarbon operates a Blue Carbon Protocol used for coastal projects in North America, currently in version 2.2 public consultation.

Methodology-level approval under the ICVCM Core Carbon Principles is becoming an important external integrity signal. As of 2024, virtually all major registries (Verra, ACR, Gold Standard) have program-level CCP approval, and methodology-level labels are being phased in across categories.

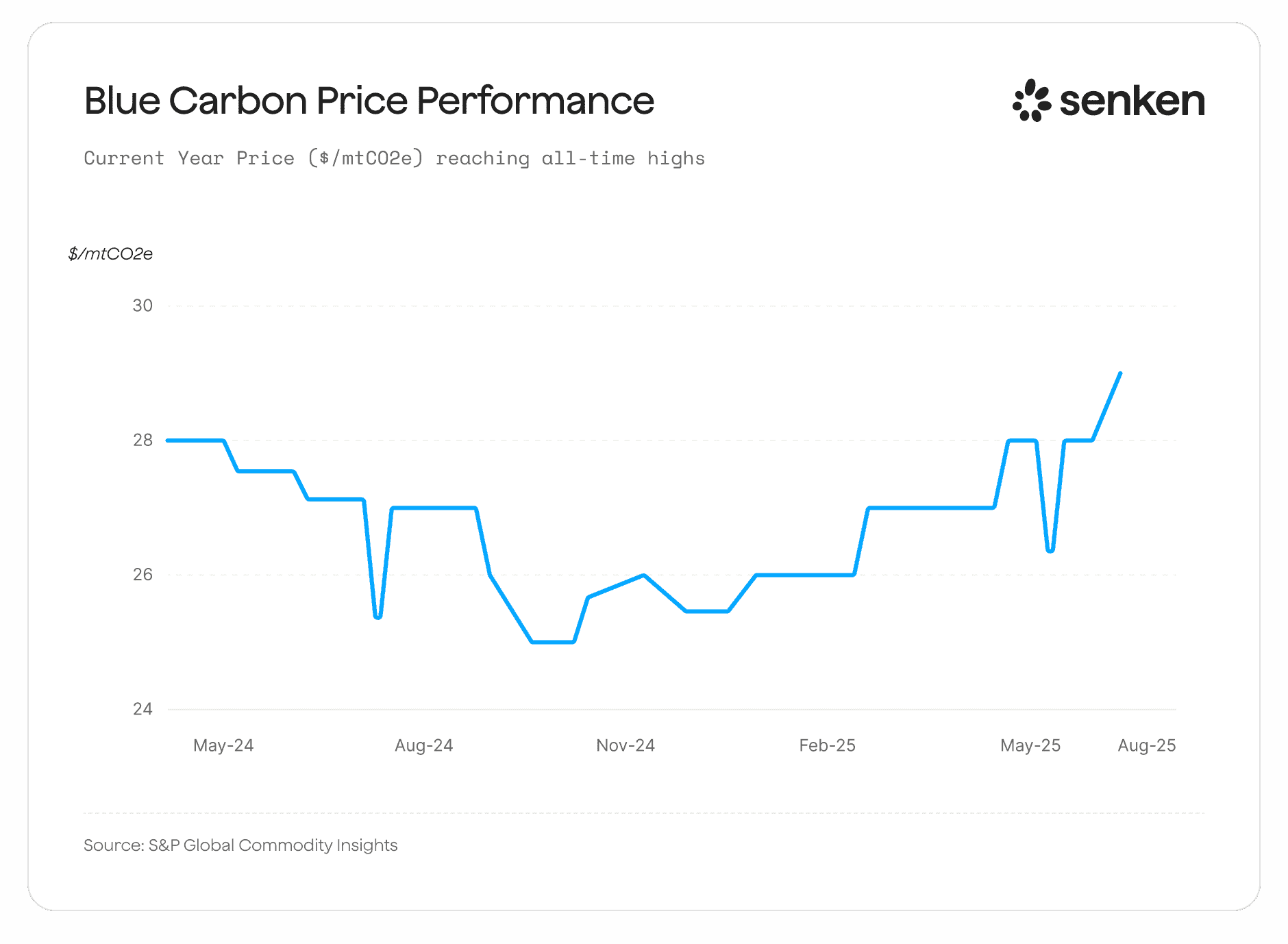

Current Pricing and Market Trends

Blue carbon credits command a price premium due to their scarcity, high integrity perception, and strong co-benefits. Independent market intelligence shows that blue carbon represents roughly 0.2 to 0.35% of total VCM issuances as of 2025, with approximately 6 to 7 million credits issued and around 3 to 4 million retired. Only about 10 projects are actively issuing credits, and nearly all issuance is from mangrove systems.

Recent price discovery offers useful benchmarks. A landmark Climate Impact X auction in November 2022 cleared 250,000 tons from Delta Blue Carbon (vintage 2021) at $27.80 per ton, with 30% of bid volume at $35 per ton or higher. S&P Global Commodity Insights launched dedicated Blue Carbon price assessments in March 2024, with assessed prices averaging in the mid-$20s in late 2024 ($25.25/tCO2e in December 2024) and reaching a record $29.30/tCO2e in August 2025 amid tight secondary-market supply. Early community projects like Vida Manglar reported first-round sales around $15 per ton in 2021 as they introduced fully quantified mangrove credits.

For DACH sustainability leads, these figures mean you should expect to pay in the mid-$20s to low-$30s per tCO2e for high-quality blue carbon credits, with prices likely to rise as demand increases and supply remains constrained. Multi-year offtake agreements can provide price and volume certainty, which is especially valuable in a segment where spot availability is limited.

How to Evaluate Blue Carbon Project Quality

Rigorous due diligence is essential. The complexity of blue carbon MRV and the market evidence that a large share of credits across the VCM are high-risk means you cannot rely on registry labels alone.

Key Quality Indicators for Buyers

Your quality checklist should cover:

- Additionality: Would conservation or restoration happen without carbon finance? Look for clear documentation of the baseline threat and financial additionality.

- Credible baselines and leakage assessment: Are baseline scenarios realistic, or are they inflated to maximize credits? Is there a plan to monitor and mitigate leakage (e.g., displacement of aquaculture or agriculture)?

- Permanence strategies: What mechanisms ensure carbon stays stored? Look for legal protection, long-term management commitments, buffer pools, and reversal risk insurance. Deep research stresses that disturbance can rapidly release long-stored soil carbon, so permanence is non-negotiable.

- Robust MRV for soil and biomass carbon: Does the project use field sampling, remote sensing, and validated models to quantify soil carbon? Is the MRV plan transparent and independently verified?

- Community participation and FPIC: Are local communities involved in project design and governance? Is there a benefit-sharing mechanism? Projects like Vida Manglar return 92% of revenues to communities, which strengthens social sustainability and reduces reversal risk.

- Independent ratings and methodology approval: Does the project score well with agencies like BeZero, Sylvera, or Calyx Global? Is the methodology approved under ICVCM Core Carbon Principles?

Senken's Sustainability Integrity Index evaluates over 600 data points across these dimensions, providing a systematic way to screen for the top-tier projects that will withstand audit and stakeholder scrutiny.

Common Risks and Red Flags to Avoid

Watch for these warning signs:

- Aggressive or opaque baselines that overstate the "business as usual" threat.

- Over-reliance on untested or proprietary MRV models without third-party validation.

- Thin or unrealistic long-term management plans with no clear funding or governance.

- Lack of clear land tenure or community consent, which increases risk of conflict and reversal.

- Weak community engagement or missing benefit-sharing arrangements.

- Poor or missing ratings from independent agencies, or projects that avoid third-party review.

If any of these red flags appear, treat the project as high-risk and either walk away or demand additional evidence and guarantees before committing budget.

Building Blue Carbon into a Diversified Carbon Portfolio

Blue carbon should be positioned as a smaller, premium slice within an Oxford-aligned, diversified portfolio. Use it to complement other nature-based removals (reforestation, peatland restoration, regenerative agriculture) and early-stage technological removals (biochar, enhanced weathering), while gradually increasing the share of very long-lived removals over time.

Practical steps:

- Size the allocation appropriately: Given limited supply and premium pricing, blue carbon might represent 5 to 15% of your annual offset or BVCM budget, not the majority.

- Diversify by region and ecosystem type: Spread exposure across mangrove, marsh, and seagrass projects, and across different geographies to reduce concentration risk.

- Use multi-year offtakes where possible: Securing volume and price through forward contracts or multi-year agreements gives you budget predictability and access to scarce supply.

- Align with internal quality and reporting criteria: Make sure your blue carbon credits meet your CSRD, SBTi, and board-level risk standards, and that you have audit-ready documentation linking each credit from issuance to retirement.

This approach allows you to capture the strategic value of blue carbon (high integrity, strong co-benefits, adaptation narrative) while managing cost and supply constraints.

How to Get Started with Blue Carbon Credits

Implementing a blue carbon strategy requires structured planning and the right procurement partners. Here's a roadmap tailored to DACH sustainability leaders.

Clarify the Role of Blue Carbon in Your Strategy

Start by defining where blue carbon fits in your net zero roadmap. Position it explicitly as Beyond Value Chain Mitigation, aligned with SBTi guidance and the Oxford Offsetting Principles. Make clear internally that blue carbon credits are not a substitute for in-value-chain emissions reductions; they are a tool to support credible net zero claims, demonstrate leadership on adaptation and biodiversity, and manage residual emissions responsibly. This framing is essential for board, audit, and communications alignment.

Set Quality and Reporting Criteria

Define internal quality criteria that reflect your regulatory obligations (CSRD, EU Green Claims), your climate commitments (SBTi), and your board's risk appetite. Specify minimum durability thresholds (e.g., conventional removals with 100+ year permanence), acceptable standards (e.g., Verra VM0033, Gold Standard mangrove), required co-benefit levels (e.g., CCB certification, SDG alignment), and exclusions (e.g., no projects with poor ratings, no aggressive baselines). Document these criteria so that procurement, legal, and sustainability teams have a shared reference point.

Choose Procurement Partners and Contract Structures

Select procurement partners who provide deep integrity assessments rather than just brokering registry credits. Look for platforms that evaluate projects across hundreds of data points (carbon impact, additionality, leakage, permanence, co-benefits, MRV quality, compliance), provide independent ratings, and can build Oxford-aligned portfolios tailored to your needs. Senken's approach, combining the Sustainability Integrity Index with end-to-end procurement and CSRD-ready reporting, is designed for exactly this purpose.

Consider contract structures carefully. Given blue carbon's supply constraints and price trajectory, multi-year offtake agreements offer volume security and cost stability. Typical procurement timelines can be as short as 3 to 4 weeks from onboarding to purchase, but building a strategic, diversified portfolio benefits from early engagement and iterative refinement.

Prepare for Audit-Ready Reporting and Claims

Ensure you have the documentation and governance processes needed to make defensible claims. This includes:

- A clear link from each credit purchased to its retirement, with registry serial numbers and vintage years.

- Transparent reporting of volume, price, project details, and verification standards in your sustainability report and CSRD disclosures.

- Internal sign-off processes that involve sustainability, legal, finance, and communications teams before credits are retired and claims are made publicly.

- Evidence packs that bundle project documentation, third-party ratings, methodology summaries, and impact metrics in a format your auditors can review efficiently.

Platforms like Senken provide CSRD-ready evidence packs and impact dashboards to simplify this reporting burden and reduce audit friction.

If you're ready to assess your current portfolio exposure, define blue carbon quality criteria, or explore how to secure a high-integrity blue carbon supply, book a conversation with Senken's team at senken.io. We'll help you build an audit-ready, diversified portfolio that thoughtfully includes blue carbon as part of a credible, Oxford-aligned net zero strategy.