Gold Standard

Key Takeaways

- Gold Standard carbon credits carry strong governance and SDG integration, but quality varies significantly by methodology and vintage—metered cookstove projects and recent land-use removals with robust buffers outperform legacy grid renewables and survey-based household methods that have documented over-crediting issues.

- Under CSRD/ESRS E1-7, you must disclose every Gold Standard retirement with full disaggregation (reduction vs removal, standard, geography, vintage, Article 6 status), while EU consumer law bans generic "climate neutral" claims from September 2026 and German courts require in-ad explanation of any offsetting—making audit-ready documentation and conservative claim language non-negotiable.

- SBTi and Oxford Offsetting Principles position Gold Standard credits as a supplement to aggressive value-chain cuts, not a substitute: prioritise ICVCM CCP-labelled Gold Standard methodologies for near-term Beyond Value Chain Mitigation, then shift portfolio weight toward durable removals (biochar, enhanced weathering, engineered CDR) as you approach residual emissions by 2040–2050.

- A repeatable due diligence workflow—filtering by CCP eligibility, checking Article 6 registry labels, reviewing verification reports, and cross-referencing SDG impact evidence—protects you from greenwashing risk and prepares your purchases for external assurance; platforms like Senken's 600+ datapoint Sustainability Integrity Index automate this multi-layered screening so your team stays lean and audit-ready.

Introduction: Why Gold Standard Carbon Credits Are on Every DACH Sustainability Leader's Desk Right Now

Gold standard carbon credits are voluntary emission reductions or removals certified by Gold Standard for the Global Goals (GS4GG), a Swiss non-profit standard-setter whose governance model, public registry, and mandatory SDG co-benefit requirements have made it the go-to quality label for corporate buyers. If you're a Head of Sustainability at a DACH enterprise preparing for CSRD assurance in 2025–2026, you already know Gold Standard is "good"—the real question is how to use it without triggering greenwashing scrutiny from BaFin, failing ESRS disclosure tests, or undermining your SBTi-aligned net-zero roadmap.

This guide cuts through the 101 noise. You'll learn where Gold Standard credits fit in a science-based strategy (Beyond Value Chain Mitigation vs residual neutralisation), how to navigate intra-standard quality variation (not all Gold Standard methodologies are created equal—ICVCM's CCP decisions prove it), what CSRD/ESRS E1-7 and the new EU consumer rules mean for your claims and documentation, and how to build a lean, repeatable procurement workflow that survives audit and board review. By the end, you'll have a practical roadmap: the right Gold Standard project types for your 2025–2030 portfolio, a due diligence checklist you can hand to procurement today, and clear guidance on what you can—and cannot—say publicly about your purchases under German advertising law and EU green claims rules.

1. Gold Standard Carbon in One Page: What It Is and Why DACH Corporates Care Now

Gold Standard carbon credits are issued under the Gold Standard for the Global Goals (GS4GG), a Swiss-based NGO standard that certifies emission reductions and removals from projects worldwide. Founded in 2003 by WWF and other environmental organisations, Gold Standard operates with ISEAL-aligned governance, technical committees, and a public Impact Registry that tracks issuance, retirement, Article 6 authorisations, and SDG impact metrics. The programme spans clean cooking and household energy, renewable energy, land use and forestry, agriculture, and emerging engineered removals, all subject to cross-cutting safeguards on additionality, stakeholder engagement, and sustainable development contributions.

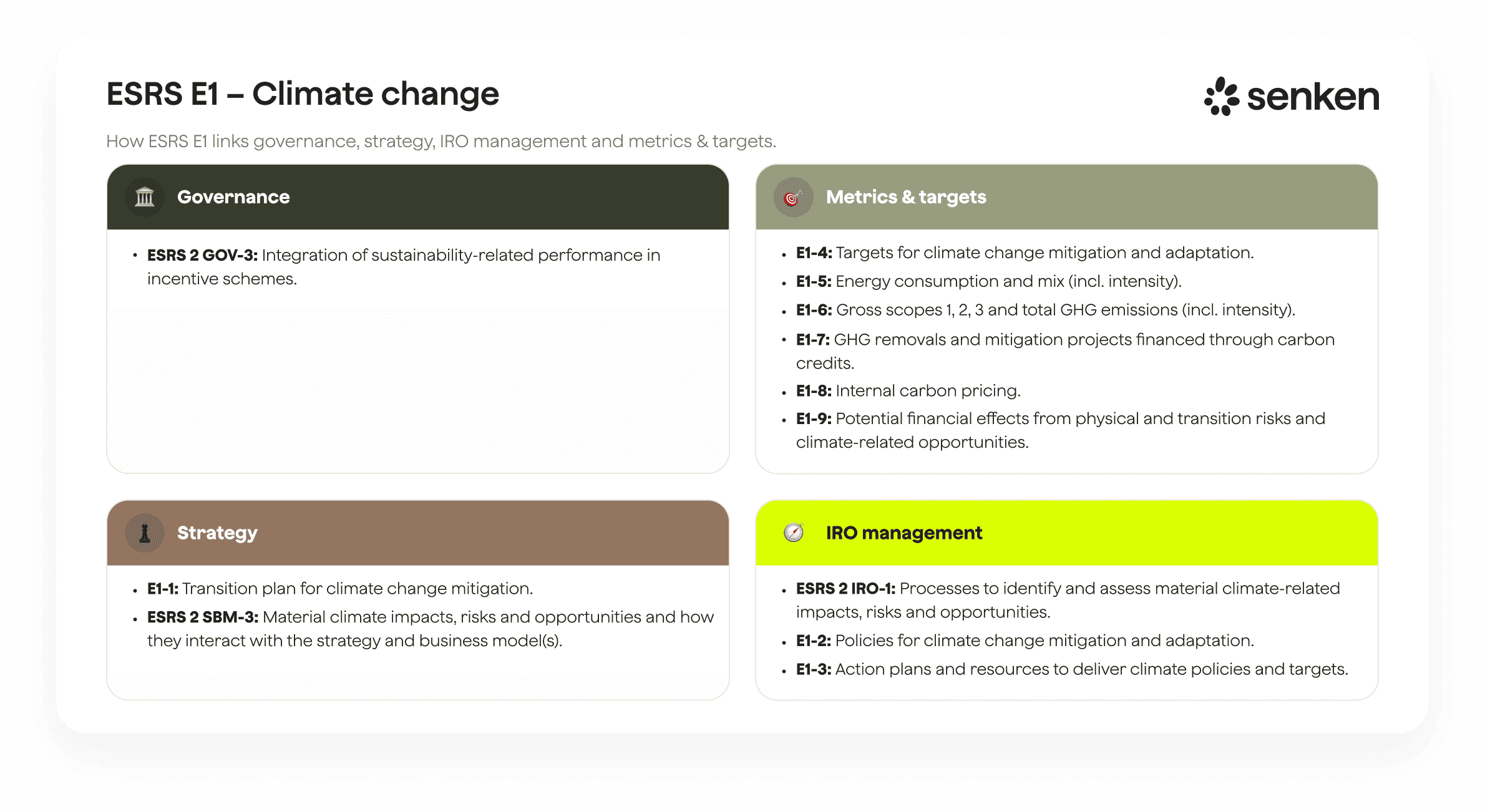

For large DACH corporates, Gold Standard has moved from sustainability nice-to-have to board-level priority for three converging reasons. First, CSRD and ESRS E1 now mandate disaggregated disclosure of carbon-credit use, including the standard employed, removal versus avoidance, corresponding-adjustment status, and geography.

Second, the EU Empowering Consumers Directive will ban generic "climate neutral" claims based solely on offsetting from September 2026, while German courts have ruled that any "klimaneutral" advertising must explain within the ad whether neutrality rests on reductions or compensations. Third, integrity frameworks like ICVCM's Core Carbon Principles and VCMI's Claims Code increasingly define what counts as high-quality supply and acceptable claims, pushing you to choose standards and methodologies that will survive audit and NGO scrutiny.

Gold Standard is CCP-Eligible at programme level and several of its methodologies have secured CCP approval, giving it a strong position in the tightening compliance landscape. However, quality within Gold Standard varies significantly by methodology, vintage, and project type. Independent evidence shows systematic over-crediting in parts of the clean-cooking portfolio, weak additionality in many legacy grid-connected renewables, and ongoing permanence and leakage risks in land-use and forestry despite Gold Standard's 20% buffer requirement. The label is not a guarantee; it is a starting point that still demands rigorous, multi-dimensional due diligence.

2. Where Gold Standard Credits Fit in a CSRD- and SBTi-Aligned Net-Zero Strategy

2.1 Clarifying the Role of Gold Standard Credits in SBTi and Oxford Offsetting Principles

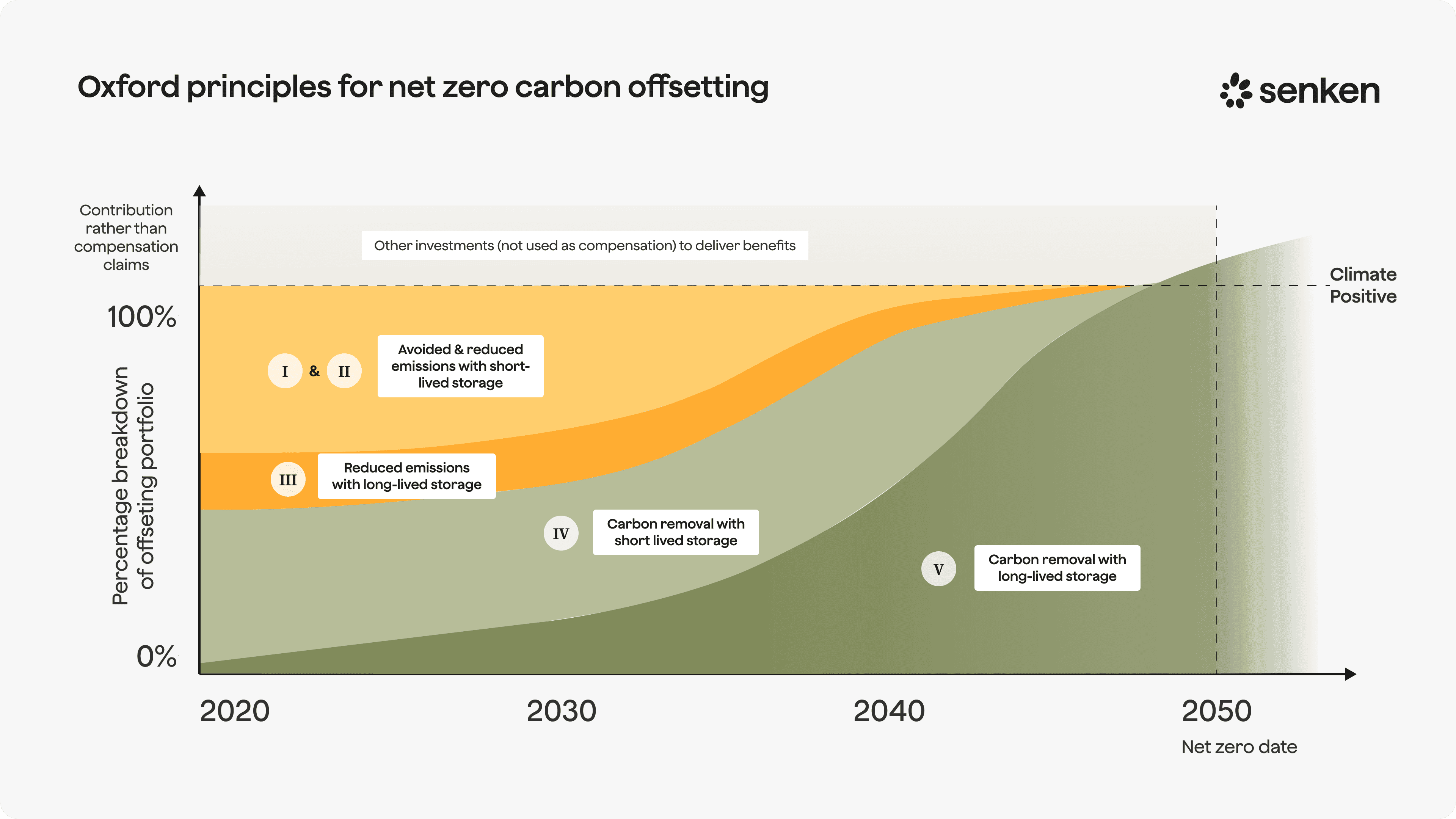

SBTi's Corporate Net-Zero Standard is unequivocal: carbon credits supplement, never substitute, value-chain decarbonisation. In practice, this means Gold Standard credits serve two distinct roles. First, Beyond Value Chain Mitigation (BVCM) allows you to finance high-integrity emission reductions or removals outside your footprint while you drive down Scope 1, 2, and 3 emissions on a science-based trajectory. BVCM is voluntary today but signals climate leadership and can be disclosed transparently in your transition plan. Second, once you reach the technical and economic limits of abatement, you may use credits to neutralise true residual emissions as part of a net-zero claim. SBTi's draft Net-Zero Standard v2 clarifies that residual neutralisation must increasingly rely on durable removals, not avoidance, and imposes stricter permanence and assurance expectations.

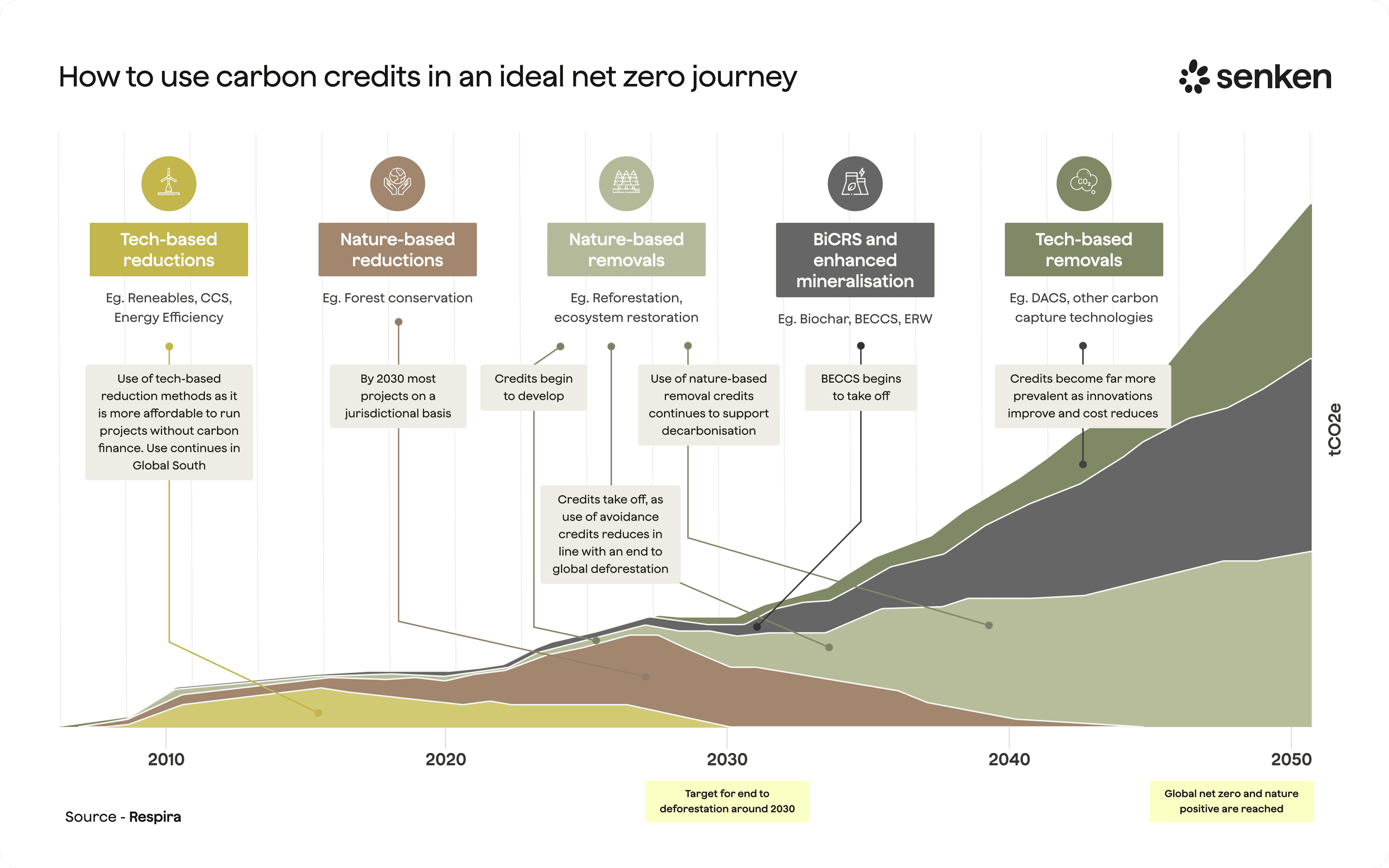

The Oxford Offsetting Principles map this timeline explicitly: prioritise radical emissions cuts now; shift from avoidance credits (renewable energy, efficient cookstoves) toward durable removals (biochar, enhanced weathering, engineered solutions) as you approach net zero; and ensure storage durability increases over time. For a large DACH enterprise with a 2040 or 2050 net-zero target, that means your 2025–2030 portfolio can sensibly blend high-integrity Gold Standard avoidance projects (metered clean cooking, robust nature-based solutions) with an increasing share of removals. By 2030–2040, the balance tips decisively toward long-lived removals, ideally those with CCP labels and storage durability of centuries to millennia.

Gold Standard's evolving methodology suite supports this glidepath. Its metered and measured cookstove methods align well with near-term BVCM; its 20% forestry buffer and new engineered-removal activity requirements provide a pathway to credible, long-duration carbon storage. The key is to design your procurement strategy today with that end-state in mind, locking in early access to CCP-approved categories and avoiding methodologies that will age poorly as integrity thresholds tighten.

2.2 Connecting Gold Standard Use to CSRD / ESRS E1-7 and EU Policy

ESRS E1-7 requires you to disclose all GHG removals and carbon-credit financing separately from gross emissions, with mandatory breakdowns: reduction versus removal; biogenic versus technological removals; the quality standard used; host country; and corresponding-adjustment status. For every Gold Standard retirement, you will need to record the project ID, methodology, vintage, removal type, registry link, CCP and CORSIA eligibility, Article 6 label (if present), and quantified SDG indicators. This data must sit in your ESRS tables and be available for limited or reasonable assurance, depending on your first reporting year under CSRD.

From September 2026, the Empowering Consumers Directive prohibits product or corporate claims of "climate neutral" or equivalent if they rest solely on offsetting, unless the claim specifies in-ad that it includes compensation and demonstrates outstanding environmental performance. In parallel, German case law (BGH, June 2024) holds that "klimaneutral" is ambiguous and must be clarified in the immediate context of the advertisement; QR codes or footnotes on websites are insufficient. For DACH companies, this means you cannot lead with a neutrality claim in product marketing or external communications unless you are prepared to explain your decarbonisation performance and the precise role of Gold Standard credits in a few clear sentences within the same visual or paragraph.

Practically, treat Gold Standard credits as an input to your transition plan and BVCM narrative, not as a licence to claim neutrality in consumer-facing channels. Frame their use as "supporting high-integrity climate projects" or "financing emissions reductions and removals beyond our value chain" while you execute aggressive reduction targets. Reserve any neutralisation language for residual emissions backed by durable removals, disclosed transparently, and reviewed by legal and compliance before publication. BaFin's heightened focus on greenwashing in sustainability marketing reinforces that conservative, evidence-backed claims are the only safe path in the DACH regulatory environment.

3. Not All Gold Standard Credits Are Equal: Methodologies, Risks, and Integrity Labels

3.1 Key Gold Standard Project Types and Where Risk Concentrates

Gold Standard's portfolio divides into five broad categories, each with distinct risk profiles. Clean cooking and household energy projects distribute efficient cookstoves or cleaner fuels to reduce fuelwood consumption and emissions. Independent peer-reviewed analysis found pervasive over-crediting across the cookstove sector, driven by over-stated adoption rates, stacking (households using both old and new stoves), and inflated assumptions about the fraction of non-renewable biomass. Critically, Gold Standard's metered and measured methodologies performed best in that assessment, with roughly 1.5× over-crediting versus 10× for survey-based approaches. ICVCM has since approved Gold Standard's TPDDTEC v4.0 and Metered & Measured cookstove methods for CCP labelling, while disapproving older household methods that lacked robust monitoring. The lesson: within Gold Standard clean cooking, methodology version and monitoring approach matter enormously.

Grid-connected renewable energy credits face widespread additionality concerns, particularly for projects registered years ago in countries with supportive policy environments and falling technology costs. Analysis shows that around one-third of voluntary-market credits, heavily weighted toward renewables, fail ICVCM's CCP additionality tests. Many legacy Gold Standard renewable projects fall into this category. Gold Standard's 2025–2026 rule updates strengthen additionality requirements and baseline conservativeness, but vintages issued before those updates carry heightened risk. If your portfolio includes pre-2024 Gold Standard grid renewables, expect scrutiny and consider whether they meet your internal integrity bar.

Land use, forestry, and agriculture projects offer co-benefits but bring permanence, leakage, and baseline uncertainty. Gold Standard mandates a 20% pooled buffer for forestry and has published dedicated risk and capacity guidelines for agriculture and blue carbon. These are comparatively conservative tools, but they cannot eliminate reversal risk (fire, disease, policy change) or fully resolve debates about whether baselines appropriately reflect business-as-usual deforestation or land-use change. Engineered removals (biochar, enhanced weathering, carbon mineralisation, and others) are newer in Gold Standard's portfolio; the programme has published activity requirements with reversal-risk provisions and net-removal accounting, but real-world performance data is still emerging. These methods align best with Oxford Principles' durability trajectory and SBTi's future requirements, making them strategically important despite higher current costs.

3.2 Using ICVCM, CCP Labels, and Article 6 Information as Filters

ICVCM's CCP framework provides the most widely recognised quality threshold in today's market. Gold Standard is CCP-Eligible at programme level, meaning its governance, standard-setting procedures, and registry meet ICVCM's baseline expectations. However, CCP eligibility is assessed at the category and methodology level as well. To date, ICVCM has approved specific Gold Standard cookstove methodologies and continues to assess other categories; many legacy methods and project types remain under review or have been found non-compliant. For procurement, this translates into a simple first filter: prioritise Gold Standard credits from CCP-approved methodologies and categories wherever possible, and apply heightened due diligence to any credits that lack that label.

VCMI's Claims Code ties corporate claims to CCP-approved or CORSIA-eligible credits, reinforcing the link between supply-side quality and demand-side credibility. If you intend to make public claims about your use of Gold Standard credits, or if you expect stakeholders to ask whether your credits are "high integrity," CCP approval is increasingly the answer they are looking for. It also future-proofs your portfolio: as integrity standards tighten and regulators lean on established benchmarks, CCP-labelled credits are far less likely to become stranded or reputationally risky.

Article 6 authorisation and corresponding adjustments add another layer. Gold Standard's Impact Registry labels credits that have been authorised by the host country under Article 6.2 or 6.4, triggering a corresponding adjustment so the emission reduction or removal is not double-counted toward that country's NDC. For corporate voluntary use, corresponding adjustments are not universally required, but they change your claim architecture. Credits with authorisation and adjustments can support "offsetting" or "neutralisation" framing under certain conditions (and still within SBTi and VCMI guardrails); credits without adjustments are better framed as "contributions" that support the host country's climate goals without altering your own inventory. In practice, track Article 6 status in your documentation and tailor your internal and external language accordingly. As the Article 6 market matures, expect increasing scrutiny on whether you are using adjusted or non-adjusted units and what claims you attach to each.

4. A Lean Due Diligence and Procurement Workflow for Gold Standard Projects

4.1 Practical Due Diligence Checklist for Gold Standard Credits

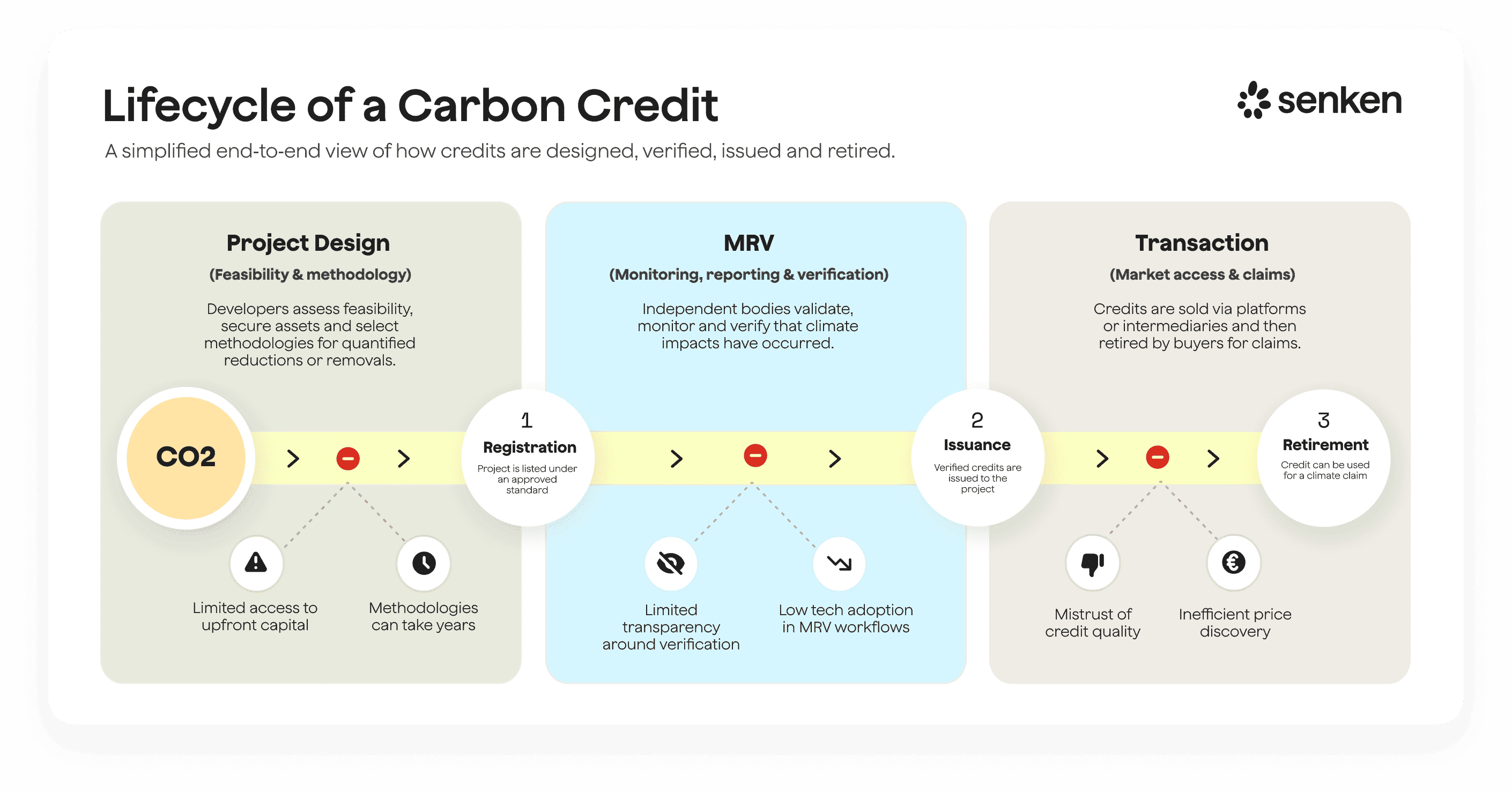

Even within Gold Standard's governance framework, project-level quality varies. A lean but robust due diligence checklist should cover six dimensions. First, programme and methodology eligibility: confirm the project is registered under Gold Standard for the Global Goals, check the methodology name and version, and verify whether that methodology is CCP-approved or pending. Cross-reference ICVCM's published decisions and Gold Standard's own announcements to ensure you are not buying from a disapproved or legacy category.

Second, additionality and baseline: review the project design document (PDD) for the additionality case. For renewable energy, scrutinise whether the project would have proceeded without carbon finance, especially if it is located in a country with feed-in tariffs, tax credits, or regulatory mandates. For cookstoves, check whether the baseline assumes 100% non-renewable biomass or uses a regionally calibrated fNRB factor; projects with inflated fNRB drive over-crediting. For land use, assess whether the baseline deforestation or degradation scenario is credible given local land tenure, economic drivers, and historical trends.

Third, permanence, leakage, and monitoring: for forestry and soil carbon, confirm the buffer contribution (Gold Standard's 20% for A/R; check project-specific risk assessments under the Risks & Capacities guidelines) and look for third-party digital MRV (satellite monitoring, remote sensing) that can detect reversals or leakage in near real time. For biochar and engineered removals, verify storage durability claims (centuries to millennia) and the methodology's approach to quantifying net removal after accounting for process emissions and energy inputs.

Fourth, SDG impact and safeguards: Gold Standard's SDG Impact Tool provides audited indicators across social, environmental, and governance dimensions. Review the project's SDG profile in the registry and ask for evidence that safeguards (gender, stakeholder consultation, grievance mechanisms) are implemented, not just documented. Fifth, Article 6 and CORSIA status: note whether the credit carries an Article 6 authorisation label and whether it is CORSIA-eligible if you have any aviation-related use cases. Finally, external ratings and reputation: cross-check the project against independent rating agencies (BeZero, Sylvera) if available, and scan recent press and NGO reports for any controversies or governance red flags.

This checklist translates integrity frameworks into questions you can ask suppliers or assess via registry data. A platform like Senken's, which applies a 600+ datapoint Sustainability Integrity Index across these dimensions, operationalises this scrutiny at scale and flags high-risk projects before they enter your shortlist.

4.2 From Project Screening to Purchase, Retirement, and ESRS Documentation

A repeatable procurement workflow has six stages.

Stage 1: Policy definition – document your internal criteria (acceptable standards, methodologies, geographies, minimum CCP or external rating, SDG alignment with corporate ESG priorities) and secure sign-off from sustainability, procurement, legal, and communications.

This policy becomes your North Star and your defence in any future audit or challenge.

Stage 2: Longlisting – generate a candidate pool via registry searches, platforms like Senken, or direct supplier outreach. Apply your policy filters (Gold Standard + CCP-eligible categories, vintage constraints, geography) to narrow the list.

Stage 3: Due diligence – run the checklist above on each shortlisted project. Capture your findings in a standardised scorecard or evidence pack so the assessment is transparent and auditable. For high-value or high-visibility purchases, consider commissioning independent technical review or leveraging Senken's Integrity Index scores.

Stage 4: Legal and compliance review – have your legal and communications teams review the intended use, claim language, and contractual terms (delivery, title transfer, retirement instructions, warranties). Confirm that the credit retirement will be registered in your company's name in the Gold Standard Impact Registry and that you will receive serialised retirement certificates. Stage 5: Purchase and retirement – execute the transaction, retire the credits promptly (do not hold them as inventory unless you have a documented, board-approved reason), and secure all transaction records and certificates.

Stage 6: ESRS documentation and reporting – for each retirement, compile the ESRS E1-7 datapoints: project ID, methodology, vintage, reduction/removal type, biogenic/technological classification, standard (Gold Standard), host country, CCP/CORSIA status, Article 6 label, and SDG indicators. Store this in a central evidence repository accessible to your CSRD assurance provider. Update your E1-7 tables annually and maintain an audit trail linking each tonne retired to the registry and to your sustainability report disclosure. This discipline turns ad hoc credit buying into a governed, compliance-ready process that scales as your volumes grow and regulatory expectations intensify.

5. Designing a Future-Proof Gold Standard Credit Portfolio for a Large Enterprise

5.1 Balancing Avoidance and Removals Over Time

Portfolio construction starts with a time-phased allocation that reflects your net-zero trajectory and the evolving guidance from SBTi and Oxford. For the 2025–2030 transition phase, a pragmatic split might allocate 60–70% to high-integrity avoidance (CCP-approved Gold Standard cookstoves, select nature-based solutions with strong additionality) and 30–40% to removals (biochar, soil carbon, early-stage engineered methods). This blend lets you access lower-cost avoidance credits for near-term BVCM while building exposure to the removal methodologies that will anchor your end-state portfolio.

From 2030 onward, reverse the ratio: target 60–80% removals, prioritising those with storage durability exceeding 1,000 years (biochar, enhanced weathering, mineralisation, DAC if cost-competitive), and reserve 20–40% for nature-based removals or high-co-benefit avoidance projects that deliver exceptional SDG outcomes. This glidepath aligns with the Oxford Principles' call to shift toward permanence and with SBTi's expectation that residual neutralisation will rely on durable removals rather than temporary or avoidance-based offsets.

Within each category, diversify by methodology and geography to manage concentration risk. Avoid over-reliance on a single project type (e.g., all cookstoves or all forestry) or a single host country, both of which expose you to methodology-specific controversies or sovereign policy changes. Spread your Gold Standard portfolio across 3–5 methodologies and 3–5 geographies, ensuring each meets your CCP and due diligence criteria. This diversification protects your strategy if a particular methodology falls out of favour or a project faces reversal or reputational issues.

5.2 Allocation by Geography, Co-Benefits, and Risk Appetite

Geography matters for both impact narrative and regulatory alignment. Many DACH corporates value regional or near-regional projects for stakeholder storytelling and supply-chain co-benefits; Gold Standard credits from European biochar or land-use projects can meet that preference, though supply is limited and pricing is often higher. Alternatively, a globally diversified portfolio (Sub-Saharan Africa for cookstoves and agroforestry, South Asia for biochar, Latin America for nature-based solutions) maximises access to high-integrity, cost-efficient supply while delivering strong SDG co-benefits in the Global South.

Co-benefit alignment offers another allocation lever. If your corporate ESG priorities emphasise gender equity, energy access, and livelihoods, weight your portfolio toward Gold Standard clean-cooking and community energy projects with documented SDG 5, 7, and 8 impacts. If nature and biodiversity rank highest, favour forestry and agroforestry projects with biodiversity safeguards and verified habitat benefits. Gold Standard's SDG Impact Tool and registry fields let you screen and report on these dimensions, turning your credit portfolio into a tangible ESG contribution that resonates with investors, employees, and customers.

Finally, calibrate risk appetite and pricing. CCP-approved, high-durability removals with strong external ratings will command premium prices (often 2–3× the cost of non-CCP avoidance credits), but they carry far lower greenwashing and stranding risk. If your internal stakeholders or board are risk-averse or if you face significant NGO or media scrutiny, bias your portfolio toward these higher-cost, higher-integrity options. If budget constraints are tight and you have strong internal due diligence capacity, you can prudently include some non-CCP but still-rigorous Gold Standard credits (e.g., well-documented forestry with third-party MRV) while transparently disclosing their status in your reporting. The key is to make that trade-off explicitly, document the rationale, and review the balance annually as market integrity standards and your own risk profile evolve.

6. Using Gold Standard Credits Without Greenwashing: Claims, Reporting, and Audit Readiness

6.1 Safe Claim Architecture for DACH Companies

The first rule of claims is clarity: separate what you have achieved through operational decarbonisation from what you are financing through credits. In all internal and external communications, lead with your absolute emissions reductions and science-based targets, then explain that you are using Gold Standard credits to support climate action beyond your value chain or to address residual emissions that cannot yet be eliminated. Avoid standalone "climate neutral" or "net zero" product claims unless you can demonstrate (a) radical reductions in the product's lifecycle emissions, (b) residual neutralisation with durable removals, and (c) transparent, in-ad disclosure of the methodology and credit use.

For voluntary corporate use, favour contribution framing over offsetting language, especially if your Gold Standard credits do not carry Article 6 corresponding adjustments. A contribution claim states that you are financing verified emissions reductions or removals that support the host country's climate goals, without asserting that those reductions "cancel out" your own emissions. This framing is legally safer under the Empowering Consumers Directive and German case law, and it aligns with VCMI's Claims Code for non-adjusted credits. If you do hold Article 6-authorised, adjusted credits and wish to frame them as offsetting or neutralisation, ensure that framing appears only in contexts where you can also disclose your gross emissions, reduction trajectory, and the proportion of residuals addressed by credits—typically your annual sustainability report or CSRD filing, not consumer marketing materials.

Internally, establish a sign-off process for any public claim involving Gold Standard credits. Route draft language through sustainability, legal, and communications, with a checklist covering: Does the claim match the volume and type of credits retired? Does it disclose the role of credits versus reductions? Does it comply with the Empowering Consumers Directive and German advertising standards? Is supporting evidence (retirement certificates, project documentation) available for audit? This governance layer catches greenwashing risk before it reaches external stakeholders.

6.2 Preparing for CSRD Assurance and Regulator Scrutiny

CSRD assurance providers will test whether your E1-7 disclosures on carbon credits are complete, accurate, and supported by evidence. For each Gold Standard retirement, they will expect to see: the retirement certificate with unique serial numbers, project ID, and retirement date; the project design document and monitoring reports (or links to registry entries) substantiating the claimed emission reductions or removals; evidence of CCP or CORSIA eligibility if you assert high-integrity status; Article 6 labels from the registry if you claim corresponding adjustments; and quantified SDG indicators if you report co-benefits in your sustainability narrative. Organise this evidence by vintage and project in a central repository (a secure folder structure or a platform like Senken's that automates traceability) so auditors can sample and verify your disclosures efficiently.

Beyond CSRD, anticipate scrutiny from BaFin (if you are a regulated financial institution), consumer protection agencies enforcing the Empowering Consumers Directive, and environmental NGOs tracking corporate climate claims. Prepare a defensive briefing document that explains your net-zero strategy, the role of Gold Standard credits within it, how you selected projects (reference your due diligence checklist and CCP filters), and how you frame claims in marketing and reporting. This document should be approved by your legal team and readily available if a regulator or NGO makes an inquiry.

Finally, review and refresh your Gold Standard portfolio and claim language annually. Integrity standards evolve, methodologies are reassessed, and regulatory expectations tighten. What passed muster in 2024 may not in 2027. Schedule a yearly governance review where you re-run due diligence on existing commitments, check for any CCP or ICVCM updates affecting your methodologies, update your ESRS documentation templates, and adjust claim language to reflect current best practice. This discipline ensures that your Gold Standard strategy remains a managed, evidence-based component of your transition plan rather than a latent reputational risk waiting to surface in an audit or public challenge.