Green Claims Directive

Key Takeaways

- The Green Claims Directive proposal is effectively paused after the Commission's 2025 withdrawal announcement, but the Empowering Consumers for the Green Transition Directive (ECGT) and national greenwashing rules still sharply tighten what you can claim—especially around climate and carbon.

- From September 2026, ECGT will ban generic green claims and offset-based product 'climate neutral' claims across the EU, forcing a fundamental redesign of how you talk about environmental performance and carbon credits.

- For large DACH companies, the immediate priority is to map all environmental and climate claims, identify high-risk wording (especially 'climate neutral' labels), and fix substantiation gaps before enforcement intensifies.

- You need an audit-ready substantiation system that links marketing claims to life-cycle data, CSRD/ESRS metrics, and—where relevant—high-integrity carbon credits, treating climate claims as a special risk class that demands transparent, defensible evidence.

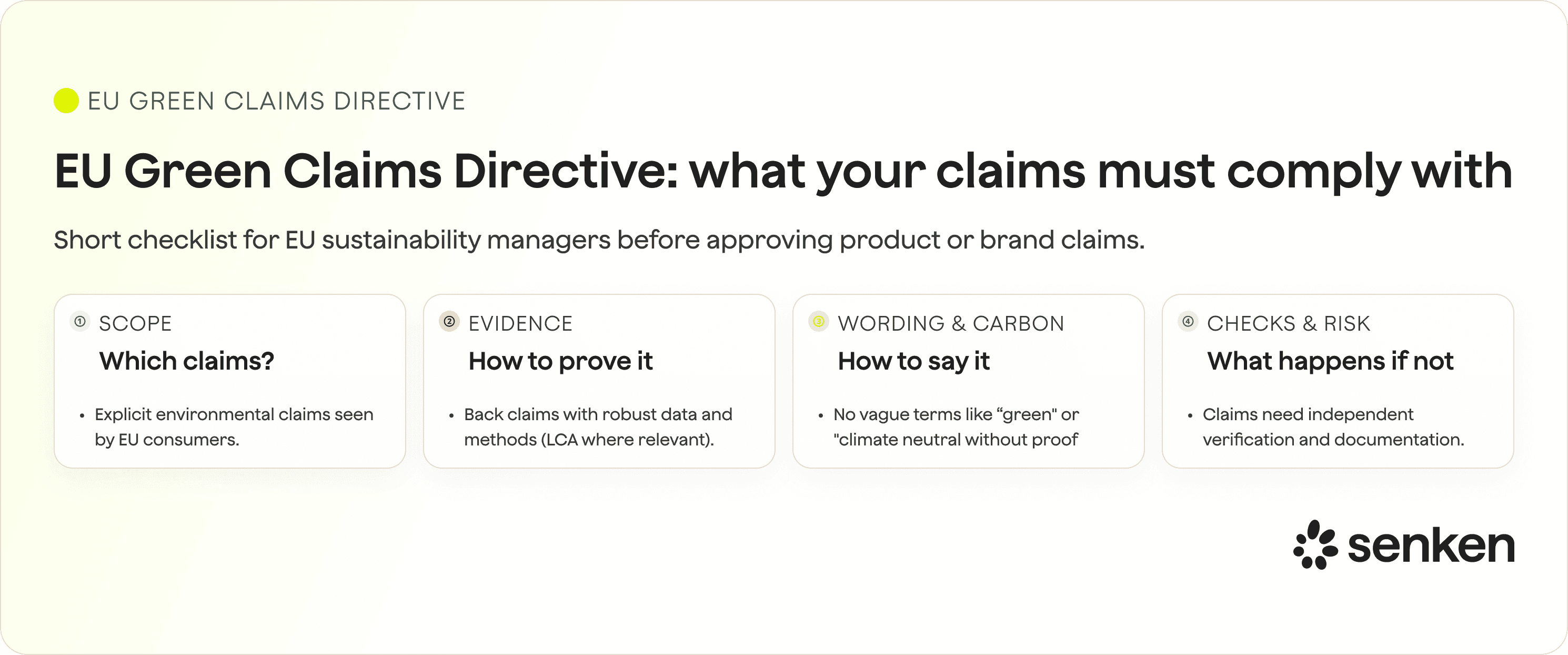

The Green Claims Directive was supposed to be the EU's answer to greenwashing: a harmonised set of rules requiring science-based substantiation, life-cycle assessment, and third-party verification for all explicit environmental claims and labels. In June 2025, the European Commission announced its intention to withdraw the proposal, effectively putting it on hold amid political concerns about administrative burden on small businesses. For many sustainability leaders, that felt like a reprieve—one less compliance deadline to worry about.

Here's the reality: even without the directive, the rules around green and climate claims just got much stricter. The Empowering Consumers for the Green Transition Directive (ECGT) is already law, banning generic environmental claims and offset-based 'climate neutral' product labels from September 2026. German courts are striking down vague climate-neutral marketing. Swiss authorities are challenging CO₂ compensation claims. And if you're running sustainability for a company with 1,000+ employees in DACH markets, you cannot afford to 'wait and see'. This article walks you through what's actually changing, what the Green Claims Directive would have required (and why that benchmark still matters), and—most importantly—the three-step playbook to clean up your claims, build audit-ready substantiation, and redesign how you use and talk about carbon credits so your climate strategy is defensible today and future-proof for whatever comes next.

Green Claims Directive in 2025: Simple definition and current status

What the Green Claims Directive was supposed to do

The Green Claims Directive was an EU proposal designed to set common, science-based rules for how companies make and back up environmental claims. Launched in March 2023, it aimed to tackle greenwashing by requiring life-cycle-based evidence for explicit environmental claims and eco-labels, plus mandatory third-party verification before you could use them in marketing. Think of it as the EU's attempt to turn vague "eco-friendly" badges into audit-ready, comparable statements that consumers and regulators could trust.

The proposal covered explicit environmental claims (like "biodegradable," "ocean-friendly," or "carbon neutral") and the proliferation of environmental labels. It would have required you to substantiate claims using recognised methodologies, demonstrate they go beyond legal baselines, disclose trade-offs, and submit to independent, accredited verification before making the claim public. The original draft also included penalties of at least 4% of annual turnover for violations, along with revenue confiscation and temporary exclusion from public procurement.

Where the file stands after the 2025 withdrawal announcement

In June 2025, the European Commission announced its intention to withdraw the Green Claims Directive. Trilogues between the Commission, Parliament, and Council were suspended, and the file effectively paused. The move followed political debates about scope (particularly the inclusion of micro-enterprises in the Council's mandate) and concerns about administrative burden under the Commission's simplification agenda.

For practical purposes, the Green Claims Directive is not coming into force anytime soon. But here's what matters: the level of rigour it set out remains the best benchmark for what "good" will look like when regulators, auditors, or NGOs scrutinise your environmental and climate claims. Even without this specific law, the direction of travel is clear. The Empowering Consumers for the Green Transition Directive (ECGT) is already in force, national consumer protection rules in Germany, Austria, and Switzerland are tightening, and your CSRD disclosures will be checked for consistency with your marketing. Treat the Green Claims Directive's requirements as your reference model, regardless of its formal status.

What still applies: ECGT and DACH enforcement on green and climate claims

Key ECGT bans every DACH sustainability lead must understand

The ECGT entered into force in March 2024. Member States must transpose it by March 2026, and it applies from September 2026. This is law, not a proposal on hold. The ECGT amends the EU's Unfair Commercial Practices Directive (UCPD) by adding new banned practices to the blacklist, and the ones most relevant to your work are:

- Generic environmental claims without recognised excellent environmental performance: Terms like "environmentally friendly," "climate friendly," "green," or "biodegradable" are prohibited unless you can demonstrate outstanding, relevant performance that's been certified or officially recognised.

- Offset-based product claims: Any claim that a product has a "neutral, reduced or positive impact in terms of greenhouse gas emissions" when it's based on offsetting is flatly banned. This kills product-level "climate neutral" or "CO₂ neutral" labels that rely on carbon credits.

- Misleading labels: Displaying a sustainability label that isn't based on a recognised certification scheme or established by public authorities is prohibited.

- Future environmental performance claims: Promises about future climate or environmental performance (like "net zero by 2030") must be backed by a clear, public, verifiable plan with concrete targets, regular independent third-party monitoring, and disclosed findings.

In simple terms, from late 2026, you cannot make vague green claims or slap a "carbon neutral" badge on a product because you bought offsets. If you talk about the future, you need an auditable roadmap.

How German, Austrian and Swiss cases are already shaping "climate neutral" marketing

DACH courts and regulators aren't waiting for EU-level harmonisation. On 27 June 2024, Germany's Federal Court of Justice (BGH) ruled that the term "klimaneutral" is inherently ambiguous. The court found that consumers may understand it as either actual emissions reductions or mere offsetting through carbon credits, and the two are not equivalent from a climate perspective. The ruling requires companies using the term to explain its concrete meaning—reduction, compensation, or both—directly in the advertisement itself, not via QR codes or links to separate websites.

Follow-on cases in lower German courts have reinforced this. For instance, the Hamburg Regional Court held that claims like "CO₂-neutral" or "CO₂-Ausgleich" mislead consumers unless the ad specifies the extent and form of reductions or compensation, names the certification standard, and identifies the verifier. Meanwhile, Swiss enforcement through the Federal Competition Commission (SECO) and the Swiss Fairness Commission (SLK) has led to the removal of "klimaneutral" and "CO₂-neutral" claims in multiple campaigns, with the SLK publishing stricter guidance in 2023 requiring robust evidence and clarity upfront.

The takeaway for your team: in DACH, assume that any climate-related claim requires in-ad clarification, robust substantiation, and evidence that offsets (if used) are high-quality and transparently disclosed. Generic "climate neutral" product labelling without these elements is a legal and reputational risk you cannot afford to take.

Step 1: Audit your current environmental and climate claims portfolio

Start by mapping what you actually say in the market. Most large companies discover they have dozens or even hundreds of environmental and climate claims scattered across packaging, websites, social media, campaigns, brochures, and point-of-sale materials. The first step is to bring them all into one place so you can assess risk and prioritise action.

Run a pragmatic four-step audit:

- Inventory all claims: Work with Marketing, Brand, and regional teams to list every environmental or climate statement you make. Include product labels, website copy, advertising campaigns, app content, and third-party eco-labels you display.

- Classify by type: Sort claims into categories. For example:

- Generic environmental (e.g., "sustainable," "eco-friendly")

- Specific attribute (e.g., "made with 30% recycled plastic")

- Climate and carbon (e.g., "carbon neutral," "climate positive," "net zero")

- Future-oriented (e.g., "net zero by 2030")

- Label-based (e.g., displaying an eco-label badge)

- Flag high-risk categories: Use the ECGT blacklist and recent DACH case law to identify claims that are high-risk. Generic green claims, offset-based neutrality claims, and weak future promises should be at the top of your review list.

- Assess substantiation gaps: For each claim, ask: Do we have the data, methodology, and documentation to defend this in an audit or court challenge? Is the evidence current (updated within the past five years)? Is it centrally stored and accessible?

A simple claims-risk matrix (claim type × legal risk × business criticality) can help you triage. For a company with more than 1,000 employees, this audit can be done in a few weeks using existing tools, with Sustainability leading a cross-functional task force that includes Legal, Marketing, and Procurement. The goal is not perfection on day one—it's visibility and a prioritised action plan.

Step 2: Build audit-ready substantiation and documentation systems

What "good" substantiation looks like in a 1,000+ employee company

Once you know what you're claiming, you need to prove it. The Green Claims Directive's original requirements offer a clear template, even if the directive itself is paused. Each claim should have a standard claim file that includes:

- Scope and wording: The exact claim as it appears in market, including the channel and date range.

- Life-cycle boundary: Which stages (raw materials, production, distribution, use, end-of-life) are covered, and which are excluded.

- Data sources and methodology: The LCA study, carbon footprint tool, or other assessment methodology you used. Include version numbers, data quality (primary vs secondary), and any assumptions.

- Performance benchmark: Evidence that the claim goes beyond legal requirements and common industry practice in your sector.

- Trade-off analysis: Any negative impacts in other environmental areas (e.g., a "recyclable" package that's heavier and increases transport emissions).

- Treatment of offsets: If you use carbon credits, a clear statement of how much impact comes from in-house reductions vs external credits, and full documentation of credit quality (see section 6).

- Verifier reports: Any third-party audit or certification that backs the claim.

- Review dates and owners: Who is responsible for updating the file, and when was it last reviewed (ideally, no older than five years).

Store these files in a centralised, audit-ready repository. Many companies use a combination of a document management system (SharePoint, Confluence) and a specialised ESG data platform to ensure traceability and version control.

Connecting claim files to CSRD data and carbon credit evidence

Your substantiation system should not operate in isolation. Link your claim files to your CSRD/ESRS disclosures, particularly your GHG inventory, transition plan, and environmental metrics. This ensures consistency: if your marketing says "30% emissions reduction since 2020," your ESRS E1 disclosure should tell the same story with the same data.

For carbon credit claims, go further. Use platforms that provide project-level transparency and traceability. For example, Senken's Sustainability Integrity Index evaluates carbon projects using over 600 data points, covering additionality, permanence, MRV quality, and co-benefits. Each project in your portfolio should come with an evidence pack that includes the project design document, verification reports, external ratings (from agencies like BeZero or Sylvera), and alignment with standards like ICVCM's Core Carbon Principles. This documentation should be linked directly into your claim files, so if a regulator or auditor asks, "What's behind your 'climate contribution' statement?" you can produce a full audit trail in hours, not weeks.

Step 3: Governance: Embedding green and climate claims into your workflows

Even the best substantiation system is useless if Marketing launches a campaign before Legal and Sustainability have reviewed the claim. You need clear decision rights, approval workflows, and escalation paths built into your organisation.

A lean governance model for large DACH corporates:

- Sustainability owns the claims policy and sets the evidence standards. You define what "good enough" substantiation looks like and maintain the central repository.

- Legal/Compliance interprets ECGT, national consumer protection law, and DACH case law. They provide sign-off on high-risk claims and flag regulatory changes.

- Marketing and Brand own channel execution and creative. They bring claims into the workflow early, before creative is locked, and ensure regional teams comply with the policy.

- Procurement ensures suppliers (including carbon credit providers) deliver the data and documentation you need to back claims.

Embed claim checks into existing workflows. Most large companies already have brand councils, legal sign-off processes, and ESG governance committees under CSRD. Integrate green claim reviews into these forums rather than creating a new, parallel structure. For example:

- Add a "green claim check" gate in your campaign approval workflow, where Marketing must submit the claim, evidence summary, and risk assessment before creative production.

- Define escalation rules: any claim involving carbon credits, "climate neutral" language, or forward-looking net zero promises should be escalated to the Head of Sustainability and General Counsel for joint review.

- Set a policy on when external verification is required. For high-value or high-visibility claims (e.g., sustainability reports, major ad campaigns, product launches), mandate third-party assurance.

The risk context justifies this rigour. The withdrawn Green Claims Directive envisaged fines of at least 4% of turnover for misleading claims, and ECGT enforcement will be handled by national consumer protection authorities with similar penalty powers. Treat green and climate claims with the same internal control seriousness you apply to financial disclosures.

Climate and carbon credit claims: Using credits without greenwashing in the ECGT era

From "climate neutral" to transparent climate contribution language

The ECGT and DACH case law have fundamentally changed the rules for climate and carbon credit claims. Under ECGT, product-level claims that a good or service is "climate neutral," "CO₂ neutral," or has a "reduced greenhouse gas footprint" based on offsetting are banned from September 2026. The German BGH has reinforced that offsetting and in-value-chain reductions are not equivalent, and consumers must be told clearly which you're doing.

What this means in practice:

- Stop using simple "carbon neutral product" or "CO₂-neutral service" labels if they rely on offsets. These will not survive ECGT enforcement.

- Instead, describe what you've actually done: "We have reduced emissions by X% compared to [baseline year] through [specific measures], and we support [type of carbon removal project] to address residual emissions. Full details: [link]."

- Be transparent about the role of credits: make it clear in the claim itself (or immediately adjacent text) if and how you use carbon credits, what type (avoidance vs removal, temporary vs durable), and how they are verified.

- Favour durable removals (e.g., biochar, direct air capture, long-lived forestry) over short-lived avoidance credits, especially for any forward-looking net zero narrative.

Leading standards like the Science Based Targets initiative (SBTi) Corporate Net-Zero Standard require deep in-value-chain reductions first (at least 90% below baseline for scope 1, 2, and relevant scope 3 emissions) before you can use carbon removals to neutralise residuals. This hierarchy—reduce, then remove—should shape your messaging. Don't claim neutrality; claim progress plus contribution.

Setting quality and documentation rules for carbon credit suppliers

If you use carbon credits, you need rigorous due diligence. Research shows that 68% of DAX40 companies that purchased credits ended up with portfolios including projects with no real climate impact, and 84% of credits on the voluntary market carry high integrity risks. To avoid becoming the next greenwashing case study, apply a strict supplier checklist:

- Prioritise in-value-chain reductions: Follow SBTi or equivalent. Credits should never replace decarbonisation, only complement it.

- Favour durable removals and ICVCM-aligned credits: Look for projects that meet the Integrity Council for the Voluntary Carbon Market's Core Carbon Principles, and prioritise removals with storage horizons of 200+ years (aligned with the Oxford Principles).

- Demand full project documentation: Your supplier should provide the project design document, baseline and additionality analysis, monitoring reports, and independent verification statements. Platforms like Senken provide this traceability as standard, with evidence packs ready for audits.

- Regularly reassess quality: Use tools like Senken's Sustainability Integrity Index, which evaluates projects on 600+ data points across carbon impact, MRV, co-benefits, and compliance, or the "Before You Buy: 10 Key Questions" framework to stress-test your portfolio at least annually.

- Align with CSRD: Ensure your carbon credit use is disclosed in your sustainability report and linked to your climate strategy, so marketing and reporting tell a consistent story.

By treating carbon credit procurement as a strategic, compliance-critical activity—not a box-ticking purchasing exercise—you turn a greenwashing risk into a defensible, transparent element of your net zero pathway.