SBTi

Key Takeaways

- SBTi has become the de facto proof that your climate targets are 1.5°C-aligned and credible under CSRD/ESRS—12,189 companies globally now use it to demonstrate Paris-compatible ambition to investors, auditors, and regulators.

- For large DACH companies, the real work isn't the SBTi form—it's building internal governance, robust Scope 1–3 data systems, and a value-chain decarbonisation plan that will survive board and auditor scrutiny in a compliance-first environment.

- SBTi's near-term and net-zero targets demand deep real reductions (typically ~4.2% p.a. for Scopes 1+2, ~90% total by 2050); carbon credits only come in for residual neutralisation and beyond value chain mitigation, and must meet extremely high quality standards to avoid greenwashing risk.

- A practical five-step roadmap—commit, measure, design, validate, integrate—gives you a concrete project plan you can plug directly into your climate transition plan, budget cycle, and CSRD reporting workstream, turning SBTi from a logo into an operational reality.

If you're a sustainability leader at a large DACH company, you've likely noticed a shift: climate targets are no longer just nice-to-have commitments buried in CSR reports. Under CSRD and ESRS E1, you must now explain how your targets are "compatible with limiting global warming to 1.5°C"—and investors, auditors, and increasingly your customers expect you to prove it. Enter the Science Based Targets initiative (SBTi): a global partnership between CDP, UN Global Compact, WRI, and WWF that translates climate science into corporate emission reduction targets aligned with the Paris Agreement. As of December 2025, over 12,000 companies worldwide have committed to or validated SBTi targets, making it the de facto standard for credible climate ambition. But here's the reality: SBTi isn't just about submitting a form and getting a badge. For organisations with over 1,000 employees navigating German supervisory board expectations, Swiss climate disclosure rules, or Austrian CSRD transposition, the real challenge is implementation—building the data infrastructure, Scope 3 strategy, governance model, and audit trail that makes your targets defensible. This guide cuts through the theory to show you exactly how to decide on SBTi, implement it in a large DACH corporate, and keep it greenwashing-proof and audit-ready from day one.

What is SBTi – and why it matters now for large DACH companies

Simple definition and who stands behind SBTi

The Science Based Targets initiative (SBTi) is a global standard-setter that helps companies set emissions reduction targets aligned with limiting global warming to 1.5°C. Born from a partnership between CDP, UN Global Compact, WRI, and WWF, SBTi has evolved into an independent charity with its own Technical Council and validation subsidiary, SBTi Services.

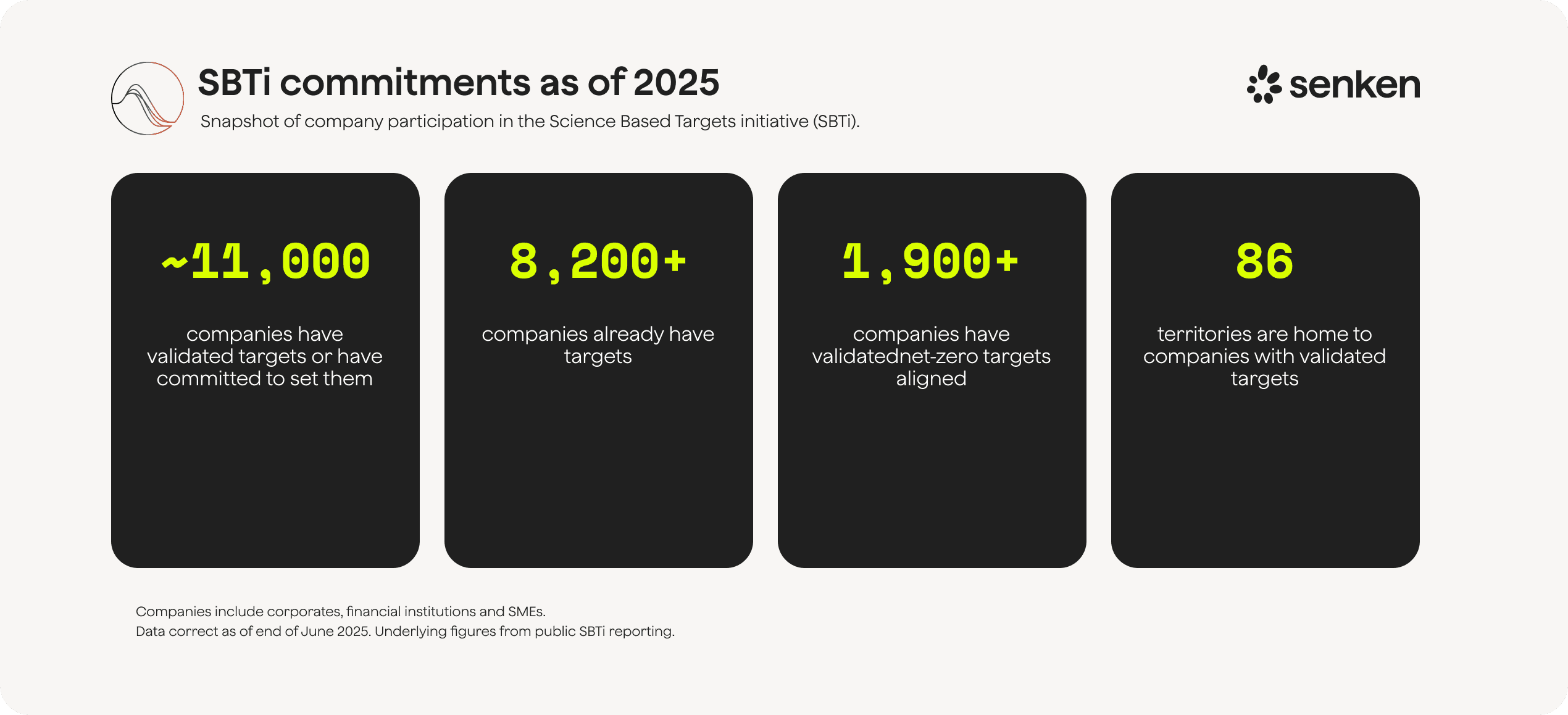

As of early December 2025, over 12,000 companies worldwide h

ave committed to or validated SBTi targets, including 2,290 with net-zero commitments . Growth has been explosive: validated near-term targets jumped 97% between end-2023 and mid-2025 , with companies with both near-term and net-zero targets up 227% in the same period. In the DACH region, you'll find many DAX, ATX, and SMI companies already validated, from Heidelberg Materials to Siemens.

SBTi translates IPCC climate science into corporate language. Instead of vague "net-zero" pledges, it defines how fast you must reduce emissions across Scopes 1, 2, and 3, what counts as progress, and what role carbon credits can (and cannot) play. This matters because it moves the conversation from "Should we commit?" to "How do we deliver?"

Voluntary standard – but de facto proof of 1.5°C alignment

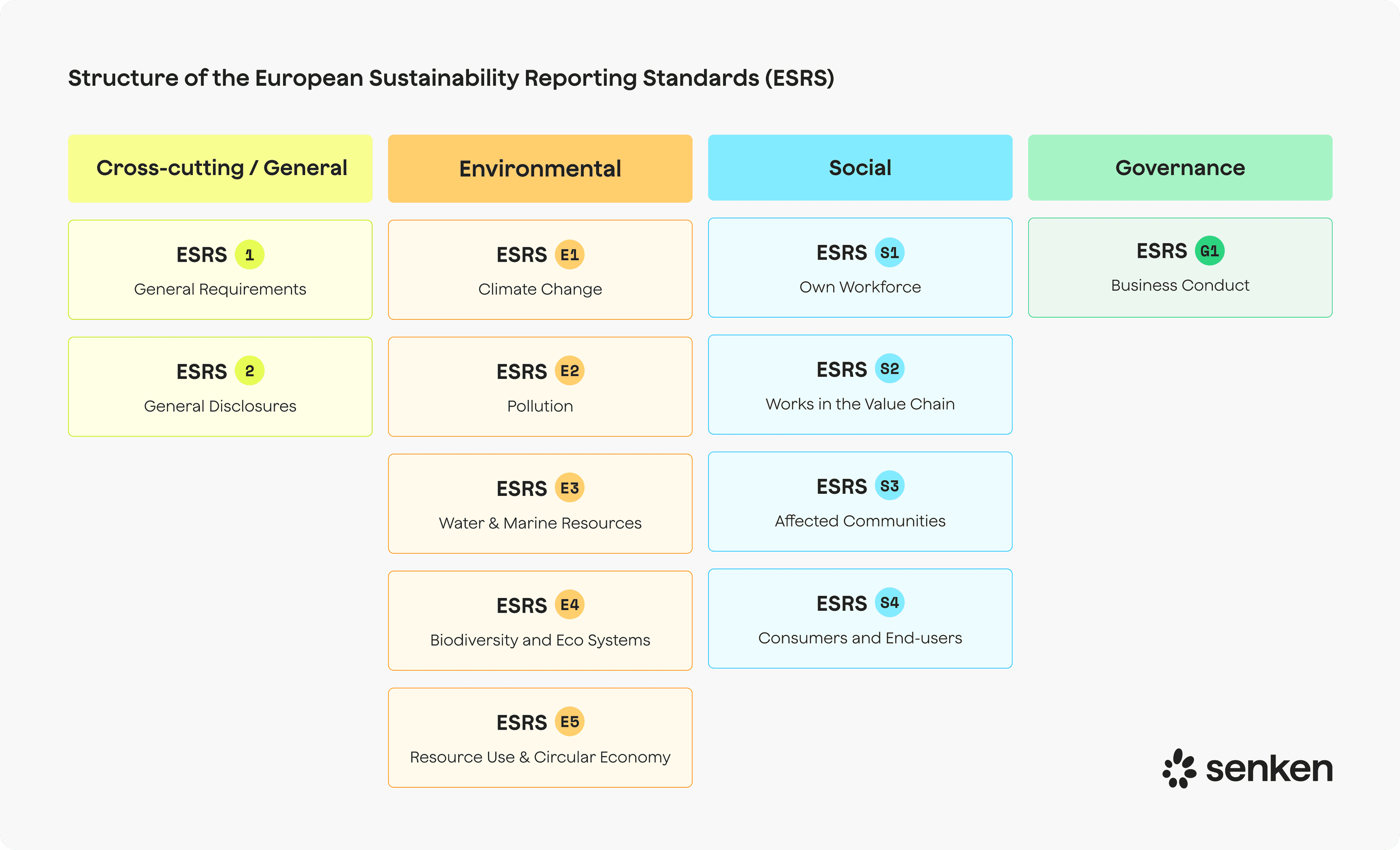

Here's the reality: SBTi is voluntary, but it has become the easiest way to prove your climate targets are Paris-aligned. CSRD's ESRS E1 explicitly requires companies to explain how their climate targets are "compatible with limiting global warming to 1.5°C." You can do that without SBTi, but investors, auditors, and lenders are increasingly expecting SBTi validation as proof.

For DACH corporates navigating CSRD, the German Corporate Governance Code's sustainability oversight requirements, and Swiss climate disclosure rules, SBTi offers a clear external benchmark. Banks and asset managers face tightened SBTi rules themselves , which flows downstream into financing and supplier expectations. In short, if you're a large company in Germany, Austria, or Switzerland, SBTi is not mandatory by law, but it's becoming a de facto standard for credibility.

The hook for you: this article isn't theory. It's a practical roadmap for deciding on SBTi, implementing it inside a complex organisation, and making it survive board scrutiny and CSRD audits.

SBTi target types in plain language: near-term, net-zero and Scope 3

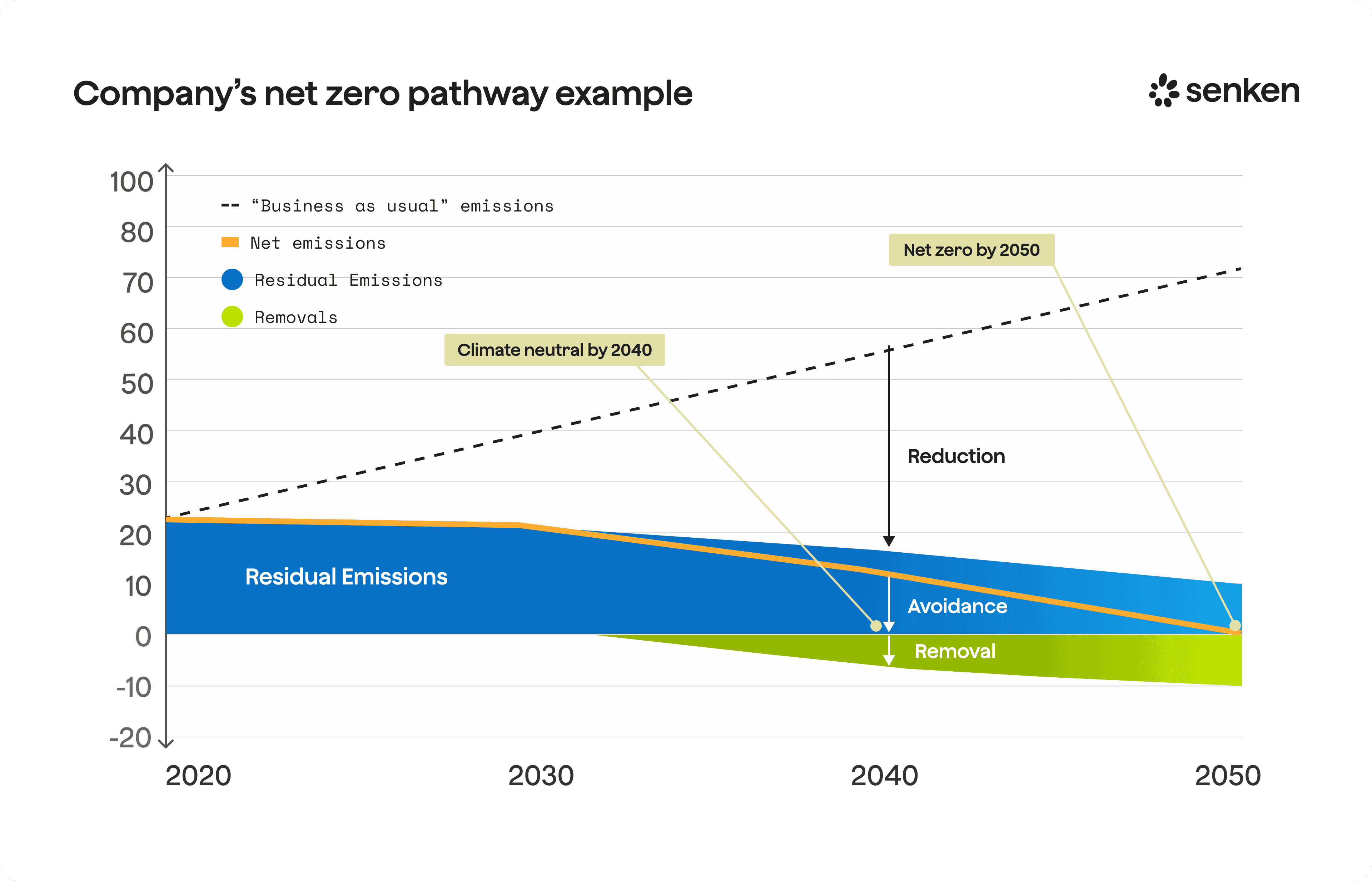

SBTi defines two main target horizons: near-term (5–10 years) and net-zero (to 2050). Near-term targets demand deep, immediate reductions. For 1.5°C alignment, that typically means cutting Scope 1 and 2 emissions by at least 4.2% per year on average, though companies with validated targets have been delivering 5.9–8.8% annual reductions in practice .

Net-zero targets under SBTi's Corporate Net-Zero Standard require reducing gross emissions by around 90% before 2050, with residual emissions (the final ~10%) neutralised through high-quality carbon removals. This is not offsetting your way out; it's near-complete decarbonisation first, then removals for what's left.

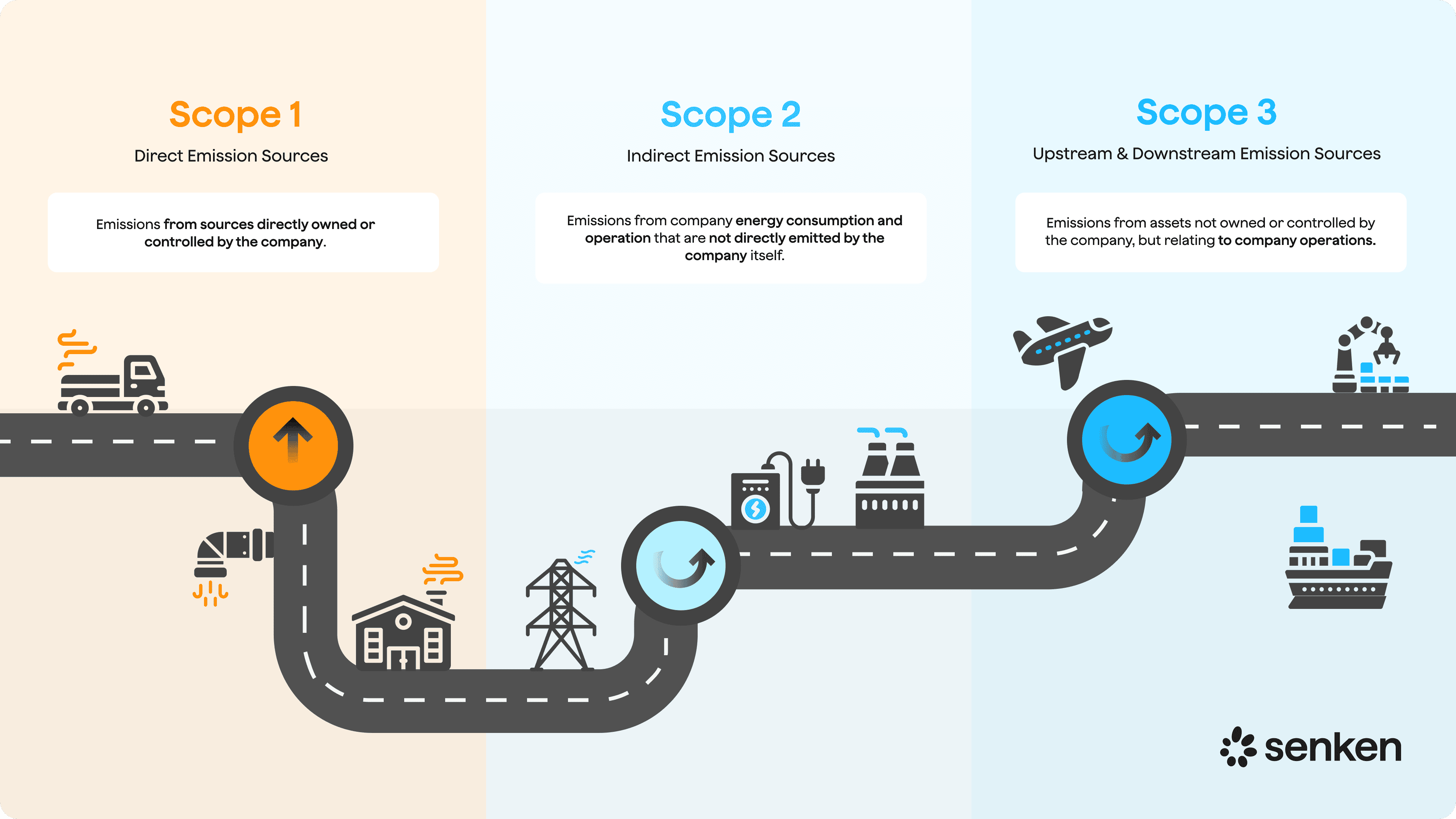

Scope 3 is where it gets real. If your value chain emissions (Scope 3) represent 40% or more of your total footprint—which they almost certainly do if you're in manufacturing, finance, telecoms, or services—you must set a Scope 3 target. That target must cover at least 67% of your total Scope 3 emissions, either through direct reduction targets or through supplier engagement (getting your suppliers to set their own SBTi targets). This isn't optional; it's the validation gatekeeper.

SBTi also publishes sector-specific pathways for steel, cement, maritime, chemicals, and others. If your industry has dedicated guidance, use it; if not, the cross-sector absolute contraction method applies. The practical takeaway: ambitious targets are table stakes, and Scope 3 is where your internal team will spend most of their time.

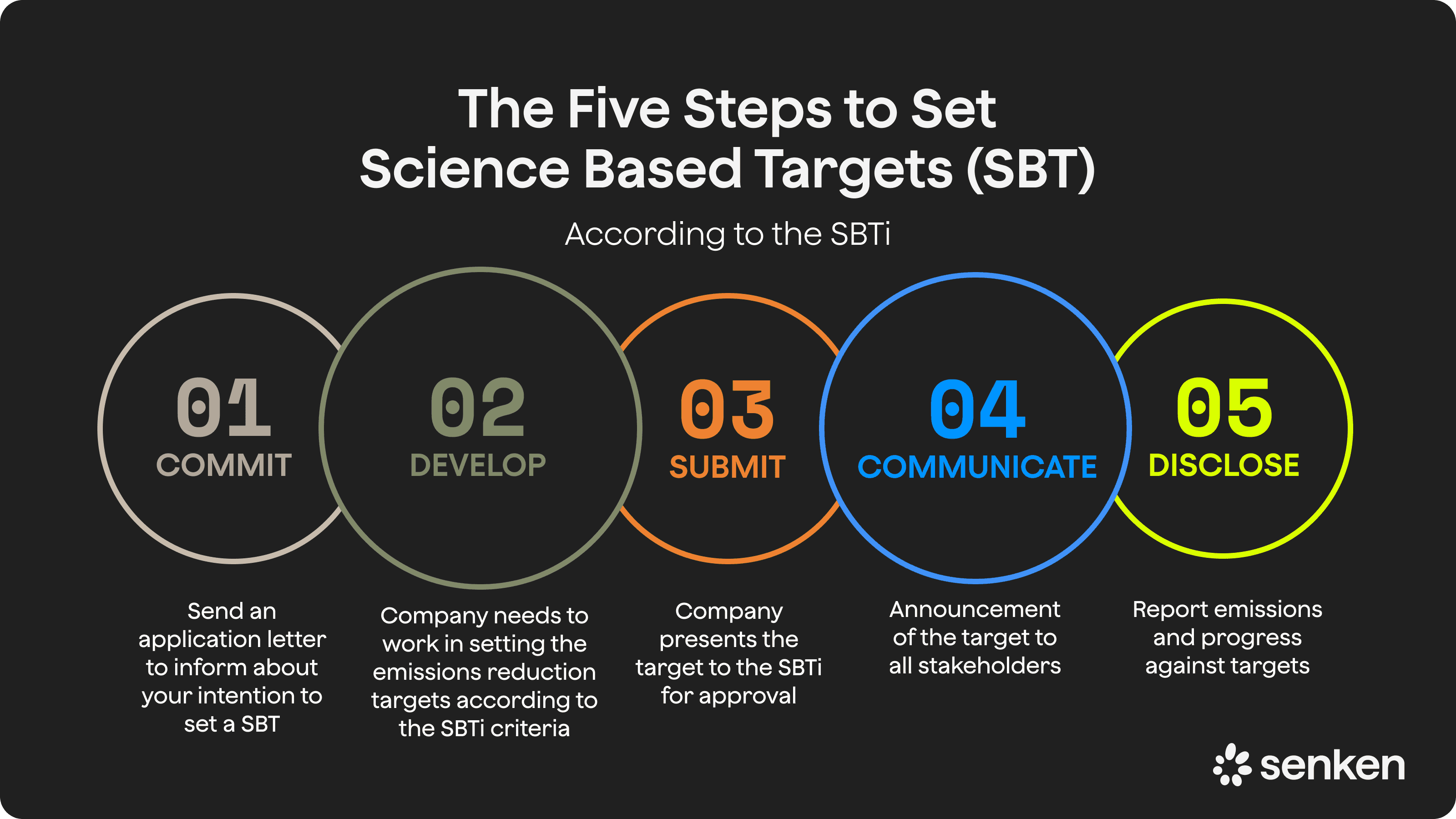

A five-step roadmap from SBTi commitment to implementation in a DACH corporate

Step 1: Decide, scope and set up cross-functional governance

Start with an internal decision memo for your board or management team. Outline why SBTi matters (CSRD/ESRS alignment, investor expectations, supply chain pressure), what resources you'll need, and a realistic timeline. For a large DACH company, expect 12–18 months from commitment to validated targets if you're starting from scratch.

Set up governance early. This isn't a sustainability-only project. You need finance (for capex modelling and EU Taxonomy alignment), risk and legal (for controls and claims), procurement (for Scope 3 supplier engagement), IT (for data systems), and HR or works council representation (especially in Germany, where operational changes may require consultation). Assign clear owners per scope and per workstream.

Typical failure mode: treating SBTi as a compliance exercise owned solely by sustainability. It's a business transformation that touches budgets, procurement contracts, product design, and reporting. Get executive sponsorship and cross-functional buy-in from day one.

Step 2: Build a robust Scope 1–3 baseline and data model

You can't set science-based targets without a credible emissions inventory. Use the GHG Protocol to measure Scopes 1, 2, and 3. For Scope 2, SBTi requires dual reporting (location-based and market-based), but you'll track progress against market-based figures, so renewable electricity procurement matters.

Scope 3 is the hard part. Run a screening across all 15 categories (purchased goods, capital goods, upstream transport, business travel, employee commuting, downstream use, etc.). For each material category, prioritise: start with spend-based estimates where you lack primary data, then build a 3–5 year roadmap to shift to activity-based and eventually supplier-specific data. The goal is "good enough to start" and improving over time, not perfection on day one.

Invest in data infrastructure: automate data flows from ERP, procurement, and travel systems. For suppliers, design data requests early and test with a few pilot partners before rolling out broadly. Document your methodology, assumptions, and data quality tier by category—auditors will ask.

Typical failure mode: waiting for perfect data before committing. Start with what you have, validate the baseline, and show your improvement plan. SBTi and CSRD both expect transparency about data limitations.

Step 3: Design science-based targets using SBTi methods

Model your targets using SBTi's Sectoral Decarbonization Approach (SDA) or absolute contraction method, depending on your sector. For Scopes 1+2, aim for at least 4.2% p.a. For Scope 3, if you're covering ≥67% via supplier engagement, define a supplier target-setting KPI (e.g., "suppliers representing 67% of Scope 3 emissions will set SBTs within five years"). If you're setting reduction targets directly, model category-specific pathways.

Link targets to real levers: renewable PPAs, energy efficiency capex, product redesign, supplier contract clauses, logistics optimisation, downstream product-use efficiency. Run scenarios with finance to understand capex needs and EU Taxonomy eligibility. This is where you turn the SBTi ambition level into an internal transition plan with budget lines.

For net-zero, plan your residual emission profile (what's left at 2050) and your neutralisation strategy. Map where you'll source high-quality removals and when. Don't over-rely on future tech; show near-term action.

Typical failure mode: setting targets that look good on paper but have no operational plan or budget behind them. Targets without levers fail validation or, worse, pass validation but fail delivery.

Step 4: Navigate SBTi validation and feedback

Submit your targets via the SBTi Services portal. In October 2024, SBTi scaled up its validation capacity with a dedicated subsidiary , but expect a multi-month review. SBTi will check your baseline, ambition level, Scope 3 coverage, and supporting documentation.

Common feedback points: insufficient Scope 3 coverage, unclear baseline year justification, targets not steep enough for 1.5°C, or weak evidence for data quality. Respond promptly with additional evidence or adjust your targets. This is a technical dialogue; assign a lead who understands the methodology.

Once validated, your targets are public on SBTi's dashboard. You're then required to report progress annually via CDP or directly to SBTi. SBTi enforces commitment deadlines—companies that miss the 24-month target submission window lose their commitment status .

Typical failure mode: treating validation as the finish line. Validation is the start. The real work is annual delivery, public reporting, and re-validation every five years.

Step 5: Embed targets into strategy, budgets and reporting

Integrate SBTi targets into your CSRD/ESRS E1 climate transition plan. Map each target to specific investments, capex plans, and operational changes. Link to EU Taxonomy KPIs where relevant (e.g., capex aligned with climate mitigation). Embed target KPIs into management dashboards and, if appropriate, link executive remuneration to progress (ESRS GOV-3 asks for this).

Build internal controls around emissions data. Treat GHG data with the same rigour as financial data: define roles, approval workflows, documentation trails, and periodic reviews. Your external auditor will assess CSRD disclosures under limited assurance, which means they'll test the process, not re-calculate every number, but weak controls will trigger qualifications.

Communicate progress transparently. Update stakeholders on wins (e.g., renewable PPAs signed, supplier SBTs secured) and setbacks. If you're off track, explain why and what you're doing about it. CSRD and SBTi both value honesty over greenwashing.

Typical failure mode: treating SBTi as a reporting exercise disconnected from business planning. Targets need teeth—budget, accountability, and consequences when milestones slip.

Scope 3 in practice: data, suppliers and real decarbonisation levers

Prioritising Scope 3 categories and dealing with data gaps

Run a Scope 3 hotspot analysis. For most DACH industrials, the biggest categories are purchased goods and services, capital goods, and downstream use of sold products. For services or finance, business travel, investments, and financed emissions dominate.

Quantify each category, even roughly, and rank by size and data availability. Focus your near-term effort on the 2–4 categories that drive 80%+ of Scope 3. For these, build a plan to shift from spend-based factors to activity data (units purchased, distance travelled) and then to supplier-specific data over 3–5 years.

For smaller categories, document your estimation approach and revisit periodically. SBTi doesn't expect perfection; it expects a credible baseline, a coverage threshold met, and a realistic improvement roadmap.

Supplier engagement models that meet SBTi's 67% rule

SBTi's supplier engagement guidance lays out how to get suppliers to commit to science-based targets themselves . Start by identifying your largest suppliers by emissions (usually a subset of spend). Engage them early: share your SBTi commitment, explain why it matters, and offer support (workshops, data templates, co-investment where feasible).

Embed SBTi language in tenders and contracts: "Suppliers representing >50% of Scope 3 Category X emissions are expected to commit to SBTi targets within two years and validate within five years." Make it a KPI in supplier scorecards. For strategic suppliers, co-develop decarbonisation roadmaps—joint capex on efficiency, shared renewable energy, or product redesign.

In the DACH context, your mid-cap supplier base is sophisticated but resource-constrained. Offer practical help: templates, connections to SBTi resources, or even financing for efficiency upgrades. Treat supplier engagement as partnership, not policing.

Internal levers: procurement, product design and logistics

Beyond supplier targets, you have direct levers. In procurement, shift specifications toward low-carbon materials (recycled content, green steel/cement, bio-based inputs). Use procurement volume to negotiate renewable-powered production or low-carbon logistics.

In product design, design for longevity, repairability, and end-of-life recycling. For downstream use, improve energy efficiency of products (if you sell equipment, vehicles, or buildings) or shift business models (product-as-a-service to extend lifetimes).

In logistics, optimise routes, shift modes (rail over road, sea over air), and work with carriers on fleet electrification or alternative fuels. For business travel, tighten policies and default to virtual where possible. These are unglamorous but high-impact.

Carbon credits under SBTi: reductions first, then high-quality removals

What SBTi allows today for offsets, EACs and neutralisation

Let's be clear: SBTi does not allow offsets to meet near-term or long-term reduction targets. Your Scope 1, 2, and 3 targets must be delivered through real emissions cuts, not by buying credits. This is the core principle and it's non-negotiable.

In April 2024, after public controversy, SBTi's Board reaffirmed that no change had been made to standards on environmental attribute certificates (EACs) for Scope 3 without due process . The second draft of the Corporate Net-Zero Standard V2, released in November 2025, explores limited, evidence-based use of certain instruments for Scope 3, but maintains the hierarchy: reductions first, always.

Where credits do come in: neutralisation of residual emissions at the net-zero point (the ~10% you can't eliminate by 2050) and beyond value chain mitigation (BVCM), which is additional climate finance you fund outside your own value chain. BVCM is encouraged but not required and does not count toward your reduction targets.

For residuals, only high-durability carbon removals qualify —think biochar, enhanced weathering, direct air capture, not short-lived forestry offsets. The bar for quality is high, and rightly so.

Designing a high-integrity carbon credit strategy for residuals and BVCM

If you plan to use credits for neutralisation later or BVCM now, quality is everything. Start with the ICVCM Core Carbon Principles as a baseline. Look for projects with transparent MRV, third-party verification, strong additionality evidence, and permanence guarantees (ideally 1,000+ years for tech-based removals, robust legal/financial safeguards for nature-based).

This is where Senken's Sustainability Integrity Index comes in. Our 600+ datapoint framework filters the market to the top 5% of credits. We assess additionality using AI models and geospatial data, verify permanence and leakage risks, check social and environmental co-benefits, and screen for compliance and reputational red flags. Every project is rated across five categories, and only the highest-scoring credits make it into portfolios.

Why does this matter for SBTi and CSRD? Because a low-quality credit undermines your entire climate claim. Under CSRD, auditors will ask: "How do you know this credit represents real, additional, permanent carbon removal?" If your answer is "the registry said so," that's not enough. You need project-level due diligence, transparent documentation, and alignment with emerging standards (ICVCM, SBTi principles, EU Green Claims rules).

Build a documentation trail: project description, methodology, verification reports, third-party ratings (e.g., BeZero, Sylvera), retirement certificates, and legal title. For CSRD, treat carbon credit procurement with the same rigour as a major capital investment. Senken provides CSRD-ready evidence packs that connect each credit to verified impact, so you can defend your claims to auditors, NGOs, and the board.

Making SBTi work with CSRD, ESRS E1 and DACH governance

Mapping SBTi targets to ESRS E1 and EU Taxonomy

ESRS E1 requires a climate transition plan that explains how your targets are 1.5°C-compatible. SBTi validation gives you that proof point. Map your SBTi near-term and net-zero targets directly into ESRS E1-1 (transition plan narrative) and E1-4 (GHG emission targets). Disclose your base year, target years, scopes covered, ambition level, and progress metrics.

Link your targets to action: in the transition plan, describe the capex, opex, and R&D investments that will deliver your SBTi pathway. Cross-reference these to your EU Taxonomy KPIs (Article 8 CapEx, OpEx, and Turnover disclosures). If your SBTi plan includes renewable energy, electrification, or green products, show how much of that capex is Taxonomy-aligned. This creates a consistent story from target to investment to disclosure.

For Scope 2, note that ESRS requires dual reporting (location- and market-based), matching SBTi's approach. For Scope 3, ESRS E1-6 asks for value chain emissions by category. Use your SBTi inventory as the foundation and ensure your Scope 3 coverage story (≥67% for SBTi, all material categories for ESRS) is consistent.

Governance, works councils and audit-ready evidence

In Germany, the updated Corporate Governance Code (DCGK 2022) embeds sustainability into board duties. Supervisory boards must integrate environmental and social objectives into strategy, planning, and risk management , and sustainability performance can be linked to executive pay. Your SBTi targets should be part of the supervisory board's annual oversight agenda: review progress, approve major investments, and escalate if delivery is off track.

Works councils (Betriebsräte) have a say on operational environmental protection measures under BetrVG. When SBTi drives changes to production processes, procurement, or workplace practices (e.g., travel policy), consult early. Frame it as job security through future-proofing, not as cost-cutting.

Build audit-ready evidence from day one. Document your baseline methodology, target-setting calculations, and progress tracking. Maintain a central repository for emissions data sources, supplier engagement records, and carbon credit due diligence. External auditors will sample-test disclosures for CSRD limited assurance; weak or missing documentation will delay sign-off and damage credibility.

90-day action checklist for DACH sustainability leaders

Here's your starter plan:

Days 1–30: Decision and scoping

- Draft internal business case for SBTi (CSRD/ESRS alignment, investor/lender expectations, competitive positioning)

- Secure executive sponsor and initial budget

- Map internal stakeholders (finance, risk, legal, procurement, operations, HR/works council)

- Assess current emissions data availability and gaps

Days 31–60: Baseline and governance

- Commission or update Scope 1–3 inventory using GHG Protocol

- Run Scope 3 hotspot analysis and prioritise 2–4 material categories

- Set up cross-functional governance (steering committee, working groups)

- Draft target-setting methodology and run initial scenarios

Days 61–90: Target design and validation prep

- Model near-term and net-zero targets using SBTi methods

- Identify decarbonisation levers and link to capex/budget cycles

- Outline Scope 3 supplier engagement approach and pilot with 3–5 key suppliers

- Begin SBTi Services submission documentation

- Define initial stance on carbon credits: residuals and BVCM only, quality criteria, and procurement approach

This checklist gets you from "Should we do SBTi?" to "We have a costed plan and we're ready to commit" in three months. Use it in board papers, project kick-offs, and internal alignment meetings.