ICROA

Key Takeaways

- ICROA's Code of Best Practice remains a practical template for carbon credit procurement rules even as the organisation winds down by late 2026—translate its six core principles (real, verified, permanent, additional, unique, conservative) directly into your RFP criteria and supplier contracts.

- ICROA accreditation audits providers and programmes, not individual projects; you still need project-level due diligence aligned with ICVCM Core Carbon Principles and third-party ratings to avoid quality risk.

- Replace "ICROA-approved" references in internal policies with an explicit integrity stack: ICVCM for credit quality, VCMI for claims discipline, SBTi for abatement-first hierarchy, and ICROA-style controls for vendor conduct and documentation.

- Under CSRD (ESRS E1), carbon credits cannot offset your Scope 1–3 totals or count toward target achievement—ICROA-aligned traceability and retirement records help you meet disclosure requirements and defend against greenwashing claims under EU consumer law.

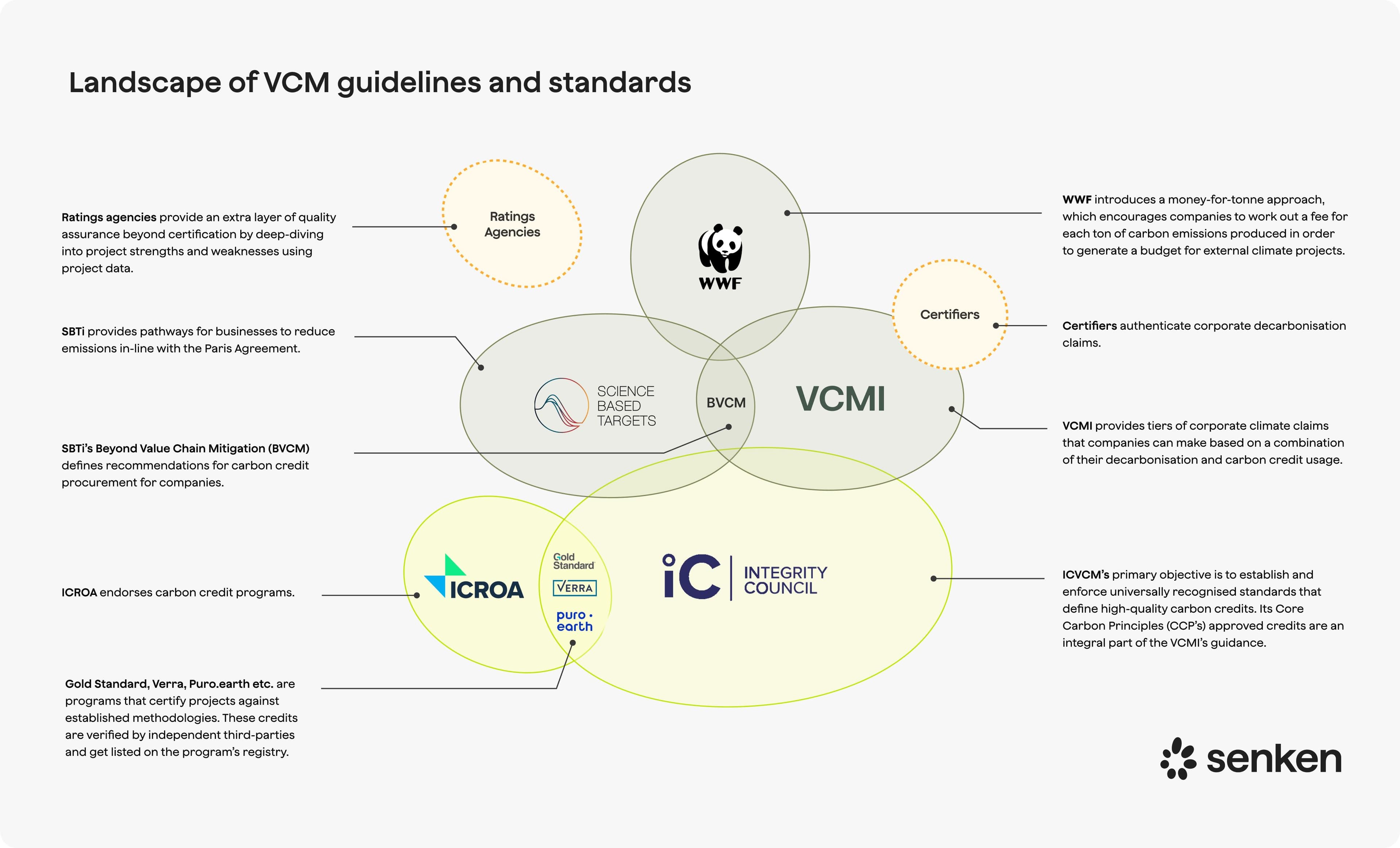

ICROA, the International Carbon Reduction and Offset Alliance, has been the voluntary carbon market's longest-running quality benchmark for offset providers. If you've seen "ICROA-accredited" on a supplier deck or referenced it in your internal offset policy, you're not alone: for over a decade, ICROA has set conduct standards and endorsed crediting programmes that corporate buyers trust. But in December 2025, ICROA announced it would wind down operations by late 2026, handing the integrity baton to newer frameworks like ICVCM and VCMI.

For DACH sustainability leaders, this raises urgent questions: What does ICROA accreditation actually guarantee—and what doesn't it cover? How do you turn ICROA's principles into concrete procurement rules and contract clauses today? And how do you transition to a post-ICROA world without rebuilding your entire offset strategy from scratch—especially under CSRD's strict disclosure requirements and tightening EU greenwashing enforcement?

This guide unpacks ICROA's Code of Best Practice, shows you how to operationalise its quality criteria in RFPs and governance frameworks, and maps out a practical transition plan that keeps your carbon credit procurement audit-ready and future-proof.

ICROA in 2025: What It Is and Why Corporates Should Still Care

ICROA, the International Carbon Reduction and Offset Alliance, is an initiative within the International Emissions Trading Association (IETA) that sets conduct standards for carbon credit providers and endorses crediting programmes. When you see "ICROA-approved" on a supplier deck, it means the provider has passed an annual third-party audit against the ICROA Code of Best Practice. When a programme is "ICROA-endorsed," it has met baseline governance and quality criteria at the programme level.

In December 2025, ICROA announced it will wind down operations by late 2026, pointing to the ICVCM and VCMI as successors for market integrity. For DACH sustainability leaders, this creates a practical question: can you still use ICROA as a reference point today, and what should replace it tomorrow?

The answer is yes and yes. ICROA's Code of Best Practice remains a solid reference point for your internal carbon credit quality rules and legacy contracts , even as the formal accreditation programme sunsets. The controls embedded in the Code, such as ex-post verification, registry traceability, and retirement discipline, align closely with what your auditors and procurement teams need under CSRD. Rather than treating ICROA as a trust label, treat it as a design template for the quality criteria and vendor controls you'll hard-code into your own governance.

The transition also offers a strategic opportunity: moving from label-based trust to an evidence-based integrity stack built on ICVCM, VCMI, SBTi, and internal policies gives you more control, better audit defence, and future-proof compliance.

What ICROA Accreditation Actually Signals for Your Carbon Credit Procurement

ICROA Approval means a provider follows the ICROA Code of Best Practice, including using only endorsed programmes, proper retirement discipline, rules for forward selling and client communications, but it does not certify each individual project or guarantee that every credit is low-risk .

Here's what sits behind an ICROA-approved provider:

Programme sourcing: Providers must transact only from ICROA-Endorsed or Conditionally Endorsed programmes, with narrow exceptions . Ex-ante or temporary units "do not meet ICROA's requirements on verification and permanence" and may not be retired .

Retirement and claims discipline: Credits used for voluntary compensation must be retired in a recognized third-party registry, in advance of any claim or with documented risk substantiation .

Forward delivery controls: For credits sold in advance of verification, providers must either guarantee delivery/replacement or maintain portfolio safeguards, with disclosure at point of sale .

Verification and monitoring: All credits must be measured, monitored, and verified ex-post; verification is to ISO 14064-3 "reasonable level of assurance"; programmes must oversee verifiers with sector-specific accreditation .

What ICROA does not do is audit individual projects. ICROA Approval is explicitly granted on a non-reliance basis and "does not confirm, accredit or verify any particular business activity, project or service offering" . You still need project-level due diligence, third-party ratings, and alignment with ICVCM Core Carbon Principles to filter out over-credited or high-reversal-risk projects.

In practice, treat ICROA Approval as a floor for provider conduct and programme choice, not a ceiling for quality assurance.

Turning the ICROA Code of Best Practice into RFPs, Contracts, and Internal Policies

Translating "real, verified, permanent, additional, unique, conservative" into buyer evidence

Each ICROA principle has a corresponding evidence package that procurement and legal teams can request:

Real and verified: Methodologies must include baseline setting, leakage assessment, conservative estimation, and baseline recalculation each crediting renewal . Ask for ex-post issuance certificates, ISO 14064-3 verification reports, and verifier accreditation proof (ISO 14065).

Additional: Programmes must require legal/regulatory additionality analysis plus at least one of financial, common-practice, barrier or benchmark approaches . Request documentation of the additionality test applied, evidence submitted, and programme approval.

Permanent: For reversal-risk projects, programmes must require multi-decadal commitments, risk mitigation plans, and a risk-backstop mechanism (e.g., buffer pool) that replaces reversed credits . Ask for buffer pool contribution percentages, reversal event history, and monitoring frequency.

Unique: Registries must assign unique serial numbers and disclose unit status ("issued/retired/cancelled") with public project documentation . Require registry links, serial numbers, and confirmation of Climate Action Data Trust connectivity to check for double use.

Conservative: Baselines must be recalculated periodically, and credits must reflect conservative estimation to avoid over-crediting. Request methodology documents and verification statements that confirm conservativeness tests.

Sample RFP questions and contract clauses you can re-use

RFP eligibility criteria:

- Are all credits sourced from ICROA-Endorsed or CCP-Eligible programmes? List programmes and confirmation.

- Are ex-ante or temporary units excluded from retirement? Confirm in writing.

- Provide registry links, unique serial numbers, and retirement certificates for sample transactions.

Contract clauses:

- Retirement timing: Credits shall be retired in [registry name] prior to any public claim by Buyer, with retirement certificate delivered within [X] days.

- Replacement guarantee: If credits are unissued at delivery date, Seller guarantees replacement from [specified programme list] or refund at purchase price plus [X]%.

- Documentation delivery: Seller shall provide verification reports, additionality assessments, buffer pool statements, and registry screenshots within [X] days of request.

These clauses operationalise ICROA-derived controls and give your procurement team audit-ready evidence. When combined with project-level screening tools like Senken's Sustainability Integrity Index, which assesses 600+ data points across additionality, permanence, leakage, MRV, and compliance, you create a layered verification system that stands up to CSRD assurance and board scrutiny.

Planning for ICROA's 2026 Wind-Down: Building a Post-ICROA Integrity Stack

What changes (and what doesn't) when ICROA disappears

ICROA announced it will wind down operations by late 2026, with no detailed buyer transition guidance issued beyond signaling that ICVCM and VCMI are "well placed to continue the work that ICROA began" .

For your contracts and policies: references to "ICROA-approved providers" will become obsolete, but the underlying standards (Verra, Gold Standard, ACR, Puro.earth) and ISO-based verification remain. What disappears is the ongoing ICROA audit and label; what persists are the programme-level requirements and verification protocols.

Practical steps for existing commitments:

- Review policies: Search internal documents for "ICROA-approved" or "ICROA-endorsed" language and flag for update by Q3 2026.

- Amend contracts: For multi-year offtake agreements referencing ICROA, add an amendment specifying successor quality criteria (e.g., "credits must meet ICVCM CCP standards and align with VCMI Claims Code").

- Communicate with providers: Ask current suppliers how they plan to demonstrate quality post-ICROA. Providers who can't articulate a transition plan may lack robust internal controls.

Using ICVCM, VCMI, SBTi and internal policies as your new guardrails

Build a simple integrity stack with four layers:

Layer 1: Unit and methodology quality (ICVCM CCP): ICVCM's Core Carbon Principles provide category-level quality assessment . Require that credits come from CCP-Approved categories and methodologies. This replaces ICROA's programme endorsement as your primary quality gate at the unit level.

Layer 2: Provider conduct and traceability (ICROA-style controls): Even without the ICROA label, hard-code the Code's operational requirements into vendor contracts: ex-post issuance only, retirement before claims, forward-delivery guarantees, unique serial numbers, and public registry links.

Layer 3: Claims integrity (VCMI): VCMI's Claims Code of Practice and Scope 3 Action Code define when and how corporate buyers can use credits to make credible claims . Align your external communications and sustainability reports with VCMI guidance, which explicitly limits credit use to addressing residual or Scope 3 gaps, not as a substitute for abatement.

Layer 4: Target-setting and abatement-first (SBTi): SBTi continues to confine carbon-credit use to taking responsibility for ongoing/residual emissions and beyond-value-chain mitigation, not as a substitute for required abatement . Use SBTi's Net-Zero Standard v2 guidance to define when credits enter your strategy (after demonstrable progress on Scope 1, 2, and 3 reductions).

Rewrite your internal offset policy to reference these four layers explicitly. For example: "Credits must be CCP-Approved, verified to ISO 14064-3, retired prior to claims as per VCMI guidance, and used only for residual emissions in line with SBTi." This formula is future-proof, auditable, and independent of any single label.

Platforms like Senken operationalise this stack by pre-screening projects against ICVCM and CSRD criteria, providing CSRD-ready evidence packs, and ensuring traceability from purchase to retirement.

Using ICROA-Style Controls to Stay Safe Under CSRD and EU Consumer Law

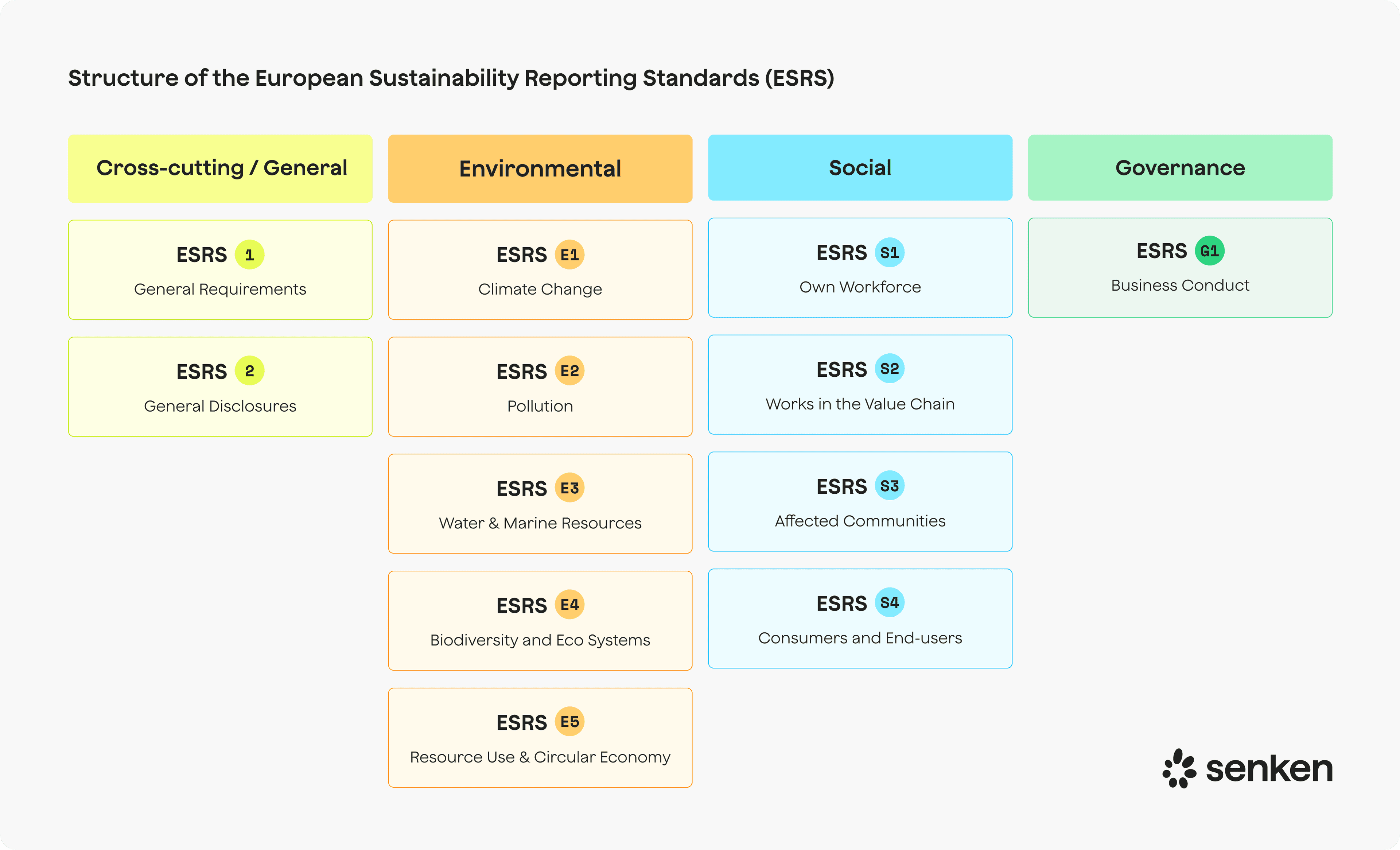

Under CSRD/ESRS E1, carbon credits must be disclosed separately and cannot be counted against Scope 1-3 totals or target achievement. E1-7 also requires disclosing the quality standards of credits, the share with corresponding adjustments, and tabular reporting of cancellations and future cancellations.

ICROA-derived controls help you meet these requirements:

Traceability and unique serial numbers support the ESRS E1-7 requirement to report credits separately with full transparency. Your auditor will ask for registry links, retirement certificates, and serial numbers; these are standard under ICROA-endorsed programmes.

Ex-post verification and permanence buffers provide the quality evidence you must disclose under E1-7. When you state "credits meet ISO 14064-3 and include buffer pool safeguards," you're operationalising ICROA-style permanence requirements in CSRD language.

Retirement-before-claims discipline protects you under EU consumer law. The Empowering Consumers for the Green Transition Directive restricts the use of environmental labels not based on recognized certification and specifically addresses claims relying on offsetting that may mislead consumers . Generic "climate neutral" claims based on offsets alone are increasingly indefensible, even with ICROA-aligned credits. Pair retirement evidence with clear, conservative language: "We have purchased and retired X tonnes of high-quality carbon removal credits to address residual emissions" is safer than "climate neutral."

Documentation for assurance: Under CSRD assurance, auditors will test ESRS-aligned disclosures, including credit quality information and corresponding adjustments, rather than rely on a provider's ICROA label . Build a documentation pack for each credit vintage: verification report, additionality assessment, buffer pool confirmation, registry screenshot, and corresponding adjustment status. This evidence base, derived from ICROA-style controls, gives your assurance provider what they need without requiring the ICROA label itself.

ICROA-style controls are necessary but not sufficient. They provide the evidence foundation; CSRD and VCMI provide the disclosure and claims framework.

Practical Checklists and Next Steps for DACH Sustainability Leaders

ICROA-informed buyer checklist:

- Programme eligibility: Credits from CCP-Eligible or ICROA-Endorsed programmes; no ex-ante or temporary units.

- Additionality and permanence evidence: Documented additionality tests (financial, regulatory, common-practice); buffer pool contributions and reversal monitoring for nature-based projects.

- Verification and MRV: ISO 14064-3 verification by ISO 14065-accredited verifiers; evidence of site visits and independent oversight.

- Registry and traceability: Unique serial numbers; public registry links; retirement certificates naming your company as beneficiary.

- Forward-delivery terms: Delivery guarantees or portfolio reserves; clear replacement rules; disclosure of issuance risk.

- ESRS E1 alignment: Separate disclosure of credits; no netting against Scope 1-3; documentation of quality standards and corresponding adjustments.

Supplier red flags:

- Refusal to provide registry links or serial numbers.

- Credits from legacy renewable energy or cookstove methodologies rejected by ICVCM.

- No third-party ratings (BeZero, Sylvera, Renoster) or ratings below BBB.

- Lack of digital MRV or ongoing monitoring for nature-based projects.

- Generic "climate neutral" marketing without VCMI-aligned disclosures.

Next steps (3-6 months):

- Audit existing policies and contracts: Search for "ICROA-approved" language; prepare amendments to reference ICVCM, VCMI, and SBTi.

- Update RFP templates: Embed the buyer checklist above into your standard vendor questionnaire.

- Map current portfolio: Score existing credits against ICVCM CCP eligibility, third-party ratings, and ESRS E1 requirements. Identify which credits may not meet future standards.

- Build internal documentation standards: Define what evidence procurement must collect (verification reports, additionality assessments, registry screenshots) and where it's stored for assurance.

- Engage a specialist partner: For teams without deep technical capacity, platforms like Senken handle project-level due diligence, SII scoring, and CSRD-ready documentation, translating ICROA-level rigor into a scalable, auditable process.

By mid-2026, you should have an ICROA-independent quality framework that satisfies your board, auditors, and regulators, and positions you ahead of peers still relying on labels alone.