CBAM

Key Takeaways

- CBAM is not just a customs issue—it's a new carbon cost line that needs joint ownership across sustainability, procurement, finance, customs, and IT to avoid compliance gaps and budget surprises.

- Build a lean 12–24 month roadmap by focusing on four workstreams: scoping your exposure, fixing data and systems, engaging suppliers for primary emissions data, and setting up internal controls that satisfy both CBAM and CSRD assurance.

- High-quality, installation-level emissions data will become mandatory from 2026—treat 2025 as a data rehearsal so you're not scrambling when verification requirements kick in.

- Simple, transparent CBAM cost models based on EU ETS prices help you quantify exposure for key materials (steel, aluminium, fertilisers) and steer procurement and decarbonisation decisions before costs escalate through 2034.

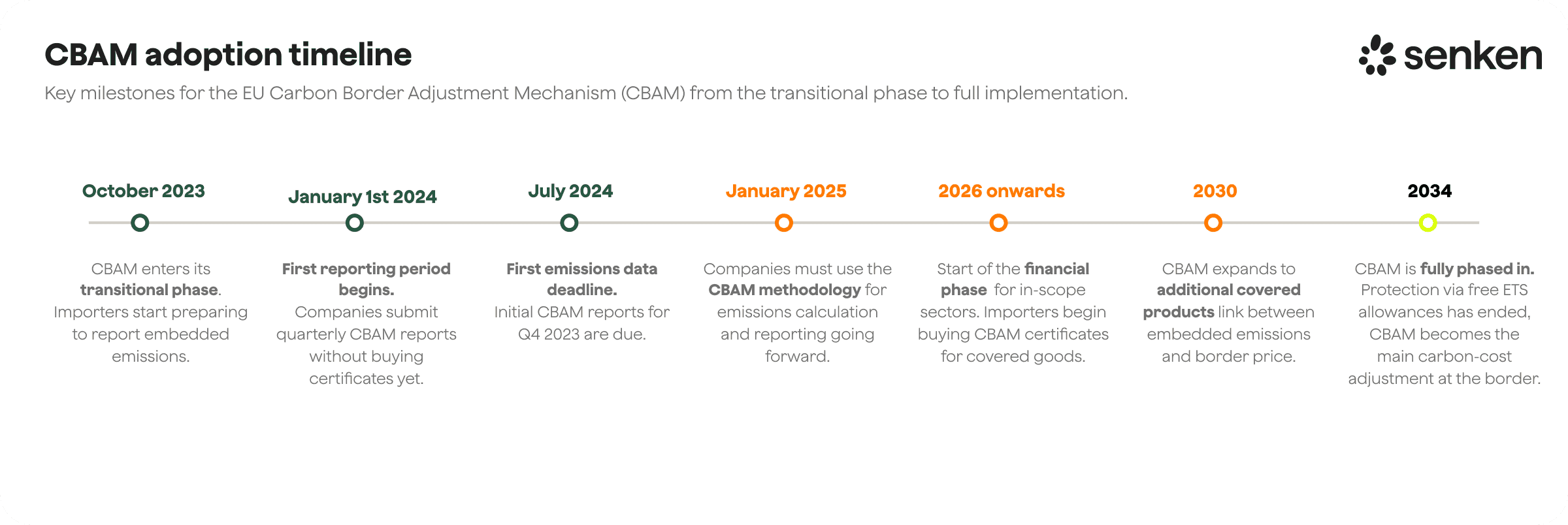

From 1 January 2026, every tonne of steel, aluminium, fertiliser, cement, electricity, or hydrogen you import into the EU will carry a carbon price at the border. That's the EU Carbon Border Adjustment Mechanism (CBAM) in plain language: a regulatory instrument designed to prevent carbon leakage by ensuring that imports face the same carbon cost as goods produced inside the EU under the Emissions Trading System (EU ETS). The transitional reporting phase (October 2023 to December 2025) gave companies time to understand their exposure and test their data systems. Now, the definitive phase is here—annual declarations, verified embedded emissions, and certificate purchases linked to EU ETS prices, with free-allocation phase-out ramping up through 2034.

For large manufacturers and importers in Germany, Austria, and Switzerland, CBAM is more than a legal obligation—it's a structural shift in how you price materials, engage suppliers, and plan decarbonisation. This guide gives you what you actually need: a governance blueprint, a 12–24 month roadmap, a simple CBAM cost formula, and a clear view on how CBAM reinforces your CSRD and supply chain strategy. In ten minutes, you'll have the operating model to turn CBAM from a compliance headache into a strategic lever.

CBAM regulation in five minutes: what it is, who it hits, and why it matters in DACH

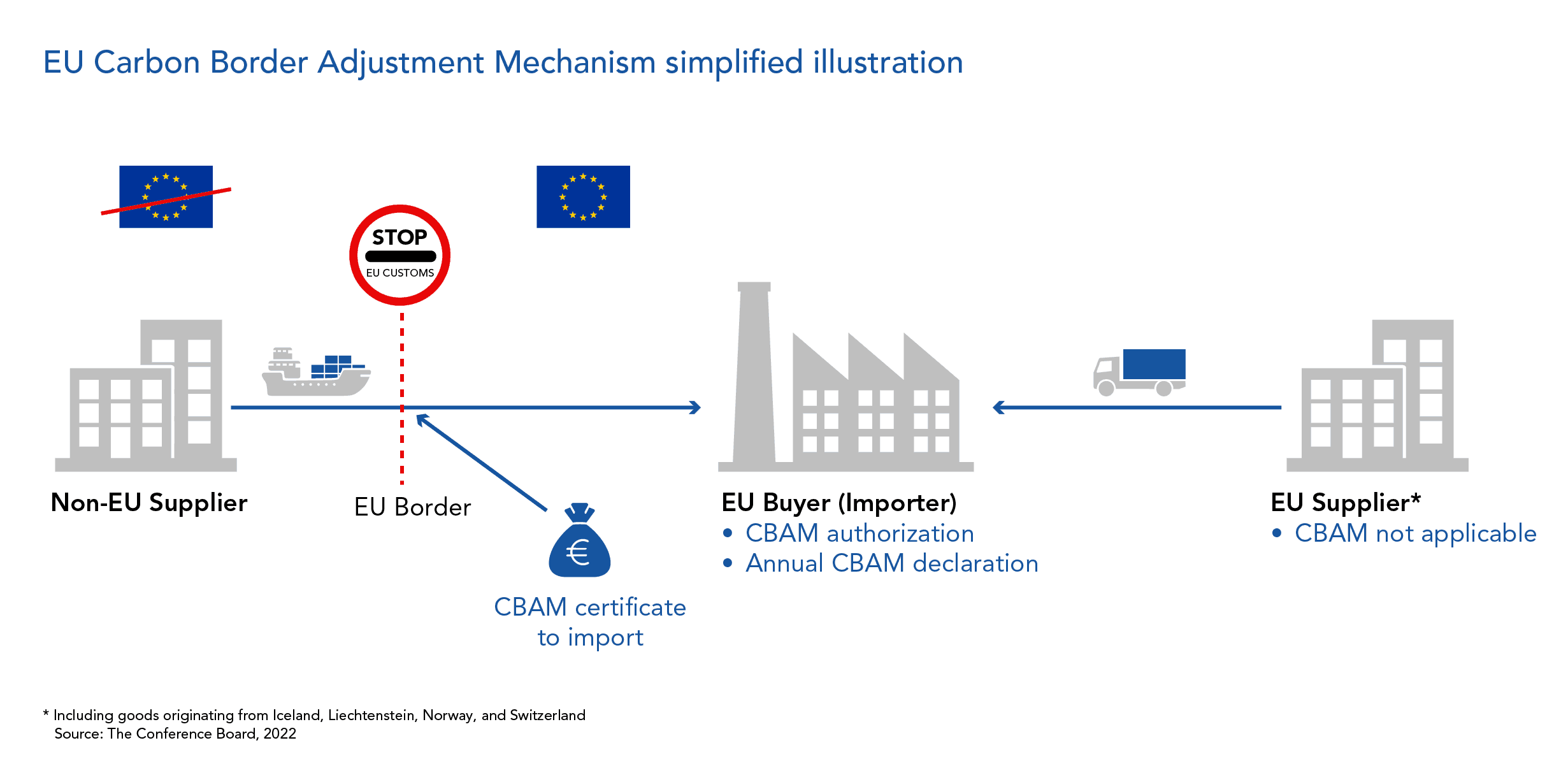

The EU Carbon Border Adjustment Mechanism (CBAM regulation) is the Union's way of putting a carbon price on certain imports. Under Regulation (EU) 2023/956, if you bring iron and steel, cement, aluminium, fertilisers, electricity or hydrogen into the EU from a non-EU country, you will soon need to account for the embedded greenhouse gas emissions in those goods and, from 2026 onwards, purchase and surrender CBAM certificates to cover them.

The mechanism exists to prevent carbon leakage. As EU producers face rising costs under the EU Emissions Trading System (ETS), CBAM levels the playing field by ensuring that imports carry a comparable carbon cost. It also supports the EU's Fit for 55 package and the phase-out of free ETS allowances in covered sectors.

Two phases matter for your planning. The transitional phase runs from 1 October 2023 to 31 December 2025. During this window, you report quarterly via the CBAM Transitional Registry but do not yet pay. The definitive phase starts on 1 January 2026. From that point, you must file an annual CBAM declaration by 31 May each year, purchase CBAM certificates at prices linked to the weekly average EU ETS auction price, and surrender certificates corresponding to your verified embedded emissions (adjusted for any carbon price already paid abroad and for the remaining share of EU free allocation).

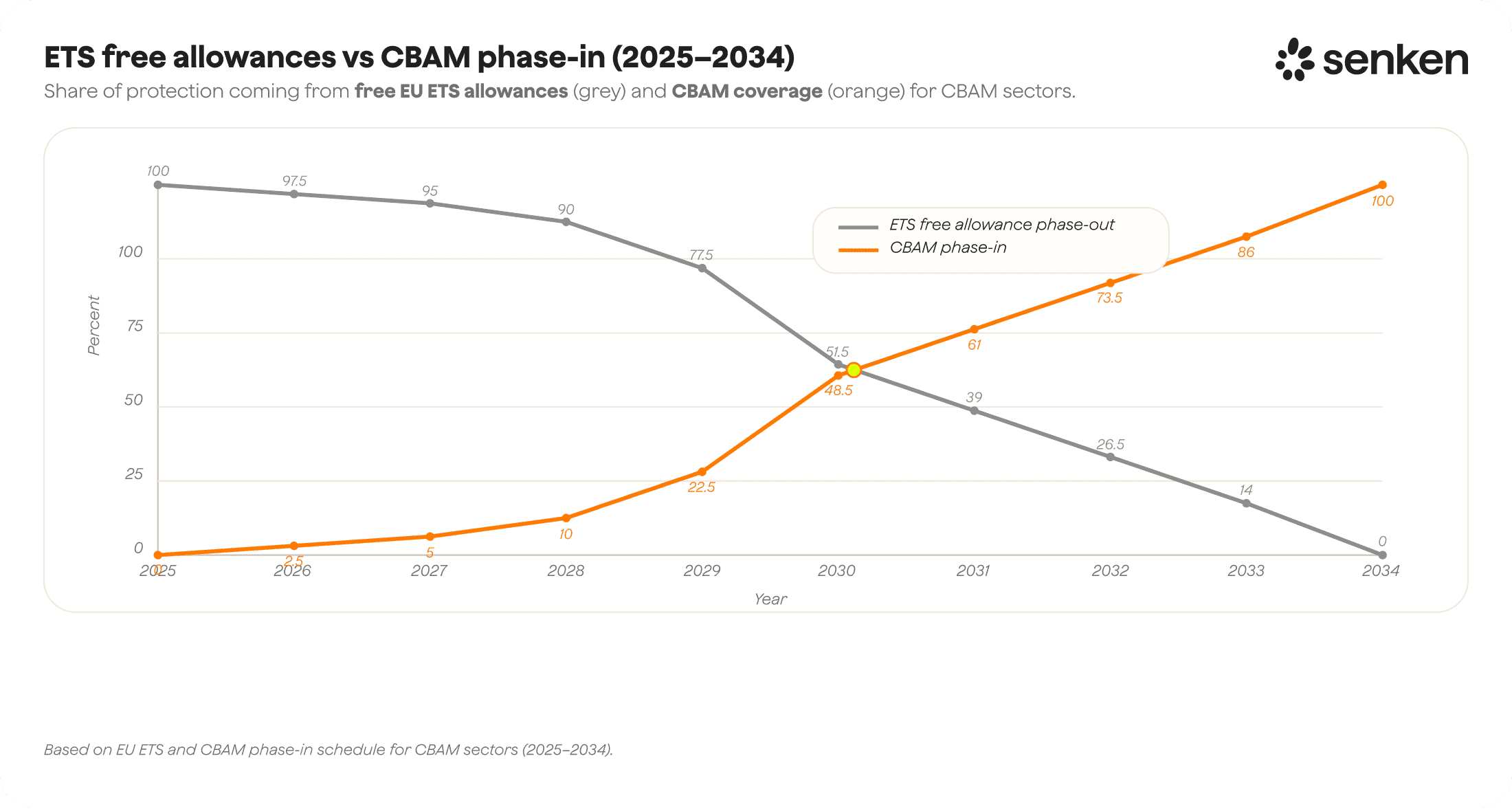

The free-allocation factor drops steadily: 97.5% in 2026, 95% in 2027, and then accelerating through 2030 (51.5%) until it reaches zero in 2034. What starts as a modest cost line in 2026 will become a material procurement and P&L item by the end of the decade.

For DACH manufacturers and importers, this is not abstract policy. If you run automotive plants importing steel and aluminium from Turkey or India, machinery operations sourcing primary aluminium from the Gulf, or chemicals businesses relying on ammonia or fertilisers from outside the EU, CBAM is now a structural feature of your cost base and a board-level topic. The simplification package adopted in October 2025 (Regulation (EU) 2025/2083) introduces a 50-tonne-per-year de minimis threshold to exempt the smallest importers, but it leaves large-scale manufacturing and trading businesses squarely in scope.

From law to ownership: who runs CBAM inside a large DACH company?

CBAM regulation sits at the intersection of sustainability, trade compliance, finance and IT. In most large DACH companies, no single function has all the skills or mandates to deliver it alone. Clear cross-functional ownership is the foundation of any workable CBAM program.

Sustainability or ESG teams should own the methodology and data quality standards. You are already familiar with GHG accounting, verification principles and the link to CSRD. CBAM's "EU method" for calculating embedded emissions and the verification requirements in Annex VI of the regulation are close cousins of what you handle for Scope 3. Your role is to define what "good" looks like for CBAM data, align it with your broader carbon footprinting and ensure the approach will stand up to external assurance.

Procurement owns supplier engagement. Your procurement colleagues manage the supplier relationships and contracts that will need to change. They must request installation-level emissions data, negotiate data-sharing clauses, and decide when to switch suppliers if the data or the carbon intensity is unacceptable. Procurement also has to balance CBAM compliance with cost, quality and delivery, so they need your support to understand why primary emissions data matters and how it can become a supplier selection criterion.

Customs and trade compliance manage the interface with authorities. They know HS codes, countries of origin, and the import declaration process. Under CBAM, someone in your group needs to become an "authorised CBAM declarant" and file declarations through the CBAM registry. Customs teams will also map which CN codes in your import flows fall under CBAM and track regulatory updates from the European Commission.

Finance, tax and treasury handle the money. CBAM certificates are a new line item to budget, purchase and account for. Finance will model exposure, set provisions and integrate CBAM costs into transfer pricing and margin analysis. Treasury may handle the actual purchase of certificates from the national registry, and tax/finance will work with external auditors to document and book the liability correctly.

IT and ERP teams make the system changes. You need to capture CBAM-relevant fields in your procurement and customs master data: CN codes, supplier installation IDs, embedded emissions per tonne, electricity mix, evidence of any foreign carbon price paid. IT must link these fields to your customs declarations and to the outputs you submit to the CBAM registry, often using the XSD schemas and templates the Commission publishes.

In a typical DACH setup, the CFO and General Counsel co-sponsor the program, Sustainability and Procurement co-lead the working group, Customs/Trade handles registry mechanics, Finance/Tax models the cost, and IT delivers the data backbone. Internal Audit and, in Germany, the Betriebsrat (works council) should be consulted early, because CBAM creates new controls and may require new supplier audit rights.

If you are reading this as the Head of Sustainability, your job is to convene the table, translate the regulation into plain language for each function, and make sure CBAM does not become an island. The best CBAM programs double as infrastructure for CSRD reporting, SBTi supplier engagement and internal carbon pricing, so design with that in mind from day one.

Your 12–24 month CBAM readiness roadmap for manufacturers and importers

A lean, pragmatic CBAM roadmap has five workstreams. You do not need a two-year consulting engagement; you need disciplined project management and clear owners for each step.

Step 1: Scope your CBAM exposure and de minimis status

Start by mapping which of your imports fall under CBAM. Work with Customs to pull import data by CN code, country of origin and annual tonnage. Cross-check against Annex I of Regulation (EU) 2023/956 to confirm scope. If your total annual imports of CBAM goods per legal entity stay below 50 tonnes, you are exempt under the 2025 simplification. For everyone else, quantify your exposure: how many tonnes of steel, aluminium, cement, fertilisers, electricity or hydrogen do you import each year, and from which countries?

This scoping exercise tells you whether you need authorised declarant status, how many suppliers you need to engage, and roughly what your cost exposure will be. Plan this for Q1 2025 if you have not done it yet.

Step 2: Design the data model and choose methodologies

Next, define what data you will collect and how. The "EU method" set out in Annex IV is your reference. For simple goods (e.g., primary steel, aluminium ingots), you need direct emissions from production plus any relevant precursor emissions. For complex goods (e.g., bolts, cables), you also need to trace inputs.

During 2024 and early 2025, you can still use default values published by the Commission for part of your reporting, but from 2026 onwards in the definitive phase, the regulation expects installation-level actual data, verified by accredited third parties. Build your data model now around primary data fields: supplier installation name and location, production route, emissions per tonne of product, electricity consumed and its carbon intensity, and documentary evidence of any explicit carbon price paid in the origin country.

Work with IT to define where these fields will live: in your ERP supplier master, in a dedicated CBAM module, or in a procurement data platform. Map how they flow into your quarterly (2025) or annual (2026+) declarations.

Step 3: Launch supplier engagement and contractual changes

Suppliers outside the EU may not yet understand CBAM or have the systems to provide installation-level data. Start engagement in 2025. Use the Commission's CBAM Communication Template as a starting point, adapt it for your supply base, and set clear deadlines.

Procurement should update standard terms to require CBAM data provision and allow for audits or data verification. Where suppliers cannot or will not provide primary data, you face a choice: accept higher costs (because you must use conservative default values), find alternative suppliers with better data, or work with the supplier to build their measurement capability.

Prioritise your largest and highest-emission suppliers first. A small number of steel, aluminium or fertiliser suppliers will account for the bulk of your CBAM exposure, so focus resources there.

Step 4: Integrate CBAM into ERP, customs and reporting workflows

CBAM data must flow from supplier invoices and attestations, through your procurement and customs systems, into your CBAM declaration. This is an IT and process design challenge.

Define a workflow: Procurement receives emissions data with each shipment or quarterly; this data is validated (does it match the product, the tonnage, the supplier installation?); it is stored with traceability (you will need it for audits); and it is aggregated and exported in the format the CBAM registry requires.

Test the workflow during the transitional phase (2025) while the penalty for errors is lower. By the time you file your first definitive declaration in May 2027 for 2026 imports, the process should be routine.

Step 5: Put in place controls, documentation and assurance

CBAM regulation requires you to keep records for at least four years. External verifiers will check your embedded emissions data before you file your declaration. Treat this like a financial audit: document your data sources, calculation methods, assumptions and any use of default values.

Align your CBAM controls with your CSRD assurance scope. If you are building systems for ESRS E1 (climate-related metrics and targets), your CBAM data can feed those disclosures and vice versa. Use the same rigour you would apply to financial reporting: clear roles, documented procedures, and an audit trail from raw supplier data to final certificate surrender.

Getting the data right: embedded emissions, systems and audit readiness

Embedded emissions are the total greenhouse gas emissions released during the production of a CBAM good, expressed in tonnes of CO2 equivalent per tonne (or MWh) of product. The regulation defines this precisely in Annex IV. For simple goods, it is the direct emissions at the installation plus the emissions from electricity consumed. For complex goods, you also include emissions from any input materials (precursors) that are themselves CBAM goods.

The EU method is your rulebook. It sets system boundaries, attribution rules and which gases to count (CO2, and in some cases N2O and perfluorocarbons). Suppliers must calculate their emissions following this method, not their national GHG inventory rules or the GHG Protocol.

During the transitional phase through end-2025, the Commission allows limited use of default values and "equivalent methods" (for example, if a supplier uses an established product carbon footprint standard). From 2026, the bar rises: you need actual, installation-specific data, and it must be verified by an accredited body under principles similar to those in the EU ETS.

Data quality has three tiers. At the top: primary, verified, installation-level data calculated per the EU method. In the middle: supplier-provided data using a recognised standard (ISO 14067, GHG Protocol Product Standard) that you can map to CBAM requirements. At the bottom: default values from the Commission's tables. Default values are conservative (often high), which means higher costs for you. Quality data is not just a compliance checkbox; it is a cost-management lever.

What to store and for how long. Keep the full calculation file for each supplier and product: the emissions factors used, production volumes, electricity inputs and carbon intensity, and any adjustments for carbon pricing in the origin country. Keep supplier attestations, third-party verification reports, and your own internal validation notes. CBAM requires four years of retention; CSRD assurance may require the same data, so design one document repository that serves both.

If you already have a product carbon footprint (PCF) program or Scope 3 Category 1 measurement in place, you have a head start. CBAM data will be more granular (installation-level, not company-level) and will follow the EU method rather than pure GHG Protocol, but the disciplines of data collection, supplier engagement and verification overlap heavily.

Quantifying CBAM costs and using them to steer procurement and decarbonisation

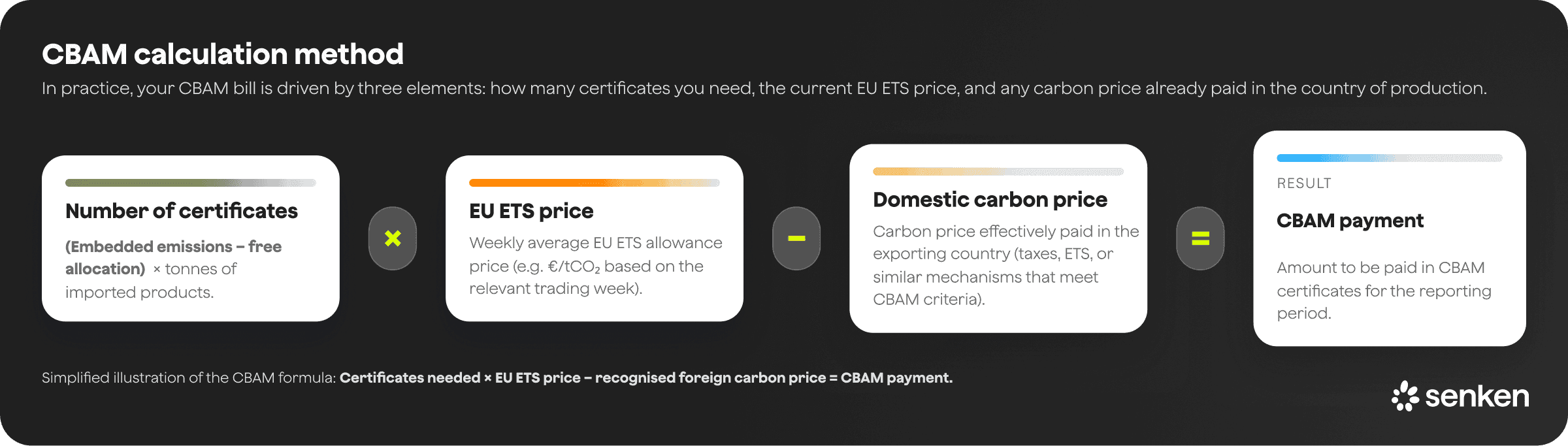

CBAM certificates are priced at the average EU ETS auction price in the preceding week. In mid-2025, EUA auctions cleared around €70 per tonne of CO2. Analysts expect prices to stay in the €70 to €90 range near term, with potential for higher levels depending on policy tightening and ETS II launch.

How do we calculate CBAM costs for our steel and aluminium imports?

Gross cost = Imports (tonnes) × Embedded emissions (tCO2e/tonne) × EUA price (€/t) × CBAM factor

The CBAM factor reflects the phase-out of free allocation: 2.5% in 2026, 5% in 2027, 10% in 2028, and rising to 100% in 2034.

Example 1: Automotive OEM importing 50,000 tonnes of steel at 1.9 tCO2e/tonne (a typical blast-furnace intensity).

- Embedded emissions: 50,000 × 1.9 = 95,000 tCO2e

- 2026 cost (2.5% factor, €70/t EUA): 95,000 × 0.025 × 70 = €166,250

- 2030 cost (48.5% factor, €70/t EUA): 95,000 × 0.485 × 70 = €3.2 million

If the supplier has paid an explicit carbon price of €20/t in their home country (verified and deductible under CBAM), you subtract that from the liability, reducing 2030 cost to roughly €2.3 million.

Example 2: Machinery business importing 10,000 tonnes of steel and 1,000 tonnes of primary aluminium (aluminium at ~15 tCO2e/t).

- Steel 2026: 10,000 × 1.9 × 0.025 × 70 = €33,250

- Aluminium 2026: 1,000 × 15 × 0.025 × 70 = €26,250

- Combined 2026: ~€60,000

- Combined 2030 (same EUA price, 48.5% factor): ~€1.2 million

These numbers assume no change in supply mix or carbon intensity. If you switch to low-carbon steel (e.g., electric-arc furnace at 0.5 tCO2e/t) or recycled aluminium (secondary aluminium at ~1 tCO2e/t), your costs drop proportionally.

How can we use CBAM numbers in internal carbon pricing and business cases?

Embed CBAM exposure into your procurement scorecards and supplier negotiations. If Supplier A offers steel at 1.9 tCO2e/t and Supplier B at 1.2 tCO2e/t, the CBAM cost difference in 2030 is material. Use the cost formula to translate emissions intensity into a euro impact and add it to your total cost of ownership.

Update your internal carbon price to reflect CBAM. If your shadow price today is €50/t but CBAM will cost you €70/t and rising, align your internal transfer price to the regulatory reality. This makes decarbonisation CapEx and supplier-switching business cases easier to justify.

Feed CBAM cost forecasts into your ESRS E1-9 disclosures on anticipated financial effects of climate risks and opportunities. CBAM is a quantifiable, near-term financial impact of carbon pricing regulation, and CSRD expects you to disclose it.

Beyond compliance: connecting CBAM with CSRD, SBTi and high-integrity carbon credits

CBAM does not exist in a vacuum. The data systems, supplier relationships and governance you build for CBAM can and should support your wider sustainability strategy.

CBAM and CSRD/ESRS. Under CSRD, you must disclose your climate strategy (ESRS E1-1), GHG emissions (E1-6), internal carbon pricing (E1-8), and anticipated financial effects from climate regulation (E1-9). CBAM feeds all of these. Your CBAM data is a subset of Scope 3 Category 1 (purchased goods), calculated at higher granularity. Your CBAM governance structure is evidence of climate-risk management for ESRS 2. Your CBAM cost forecasts quantify the financial effect of carbon pricing for E1-9. Design one data pipeline and one set of controls that satisfy both CBAM reporting and CSRD assurance, rather than running parallel processes.

CBAM and SBTi supplier engagement. Science Based Targets initiative (SBTi) guidance encourages companies to set supplier engagement targets as part of Scope 3 reduction. CBAM supplier programs are a natural vehicle: you are already asking suppliers for primary emissions data, so layer in a request for their decarbonisation roadmap, and offer support (financing, technical advice, volume commitments) to suppliers who commit to lower-carbon production routes. Track the tonnage and emissions covered by these programs and report it as supplier engagement under SBTi.

Can voluntary carbon credits reduce CBAM liabilities? No. Regulation (EU) 2023/956 is explicit: only an explicit carbon price effectively paid in the country of origin (for example, a national ETS or carbon tax) can be deducted from your CBAM obligation. Voluntary carbon credits or offsets purchased by the supplier or by you do not count.

That said, high-integrity voluntary carbon credits still have a role in your broader net-zero strategy. Use them to finance beyond-value-chain mitigation (for example, removals to address residual Scope 1, 2 or 3 emissions you cannot eliminate), but do not conflate them with CBAM compliance. The rigour you apply to CBAM data (traceability, verification, third-party assurance) is exactly the rigour you should demand from any carbon credits you buy. At Senken, we assess carbon projects through 600+ data points and reject over 95% of projects we review, because the same accountability standards that underpin CBAM and CSRD should guide voluntary climate investments. If you are building audit-ready systems for CBAM, extend that discipline to your carbon credit portfolio.