CRCF

Key Takeaways

- The EU Carbon Removals Certification Framework (CRCF) is a voluntary regulation that sets a common quality baseline for permanent carbon removals, carbon farming, and carbon storage in products—and it will quietly become the reference point for what "high-quality" means across European carbon markets from 2026 onwards.

- For DACH corporates, CRCF isn't just a policy topic—it's an operating system change that affects how you buy credits, classify them in CSRD/ESRS reporting, plan for SBTi compliance, and defend voluntary claims against rising greenwashing enforcement in Germany, Austria, and Switzerland.

- You can start preparing now by mapping your current carbon portfolio to future CRCF categories (permanent removals, carbon farming, product storage) and flagging segments unlikely to meet CRCF or ICVCM-quality thresholds before your next audit cycle.

- CRCF will interact tightly with CSRD (ESRS E1), SBTi's Net-Zero Standard V2, and VCMI's Claims Code—but none of these frameworks allow you to "net off" emissions with credits in the way many legacy strategies assumed, so your claims language and target accounting need updating.

Introduction: What the EU Carbon Removals Certification Framework Means for Your 2025–2030 Strategy

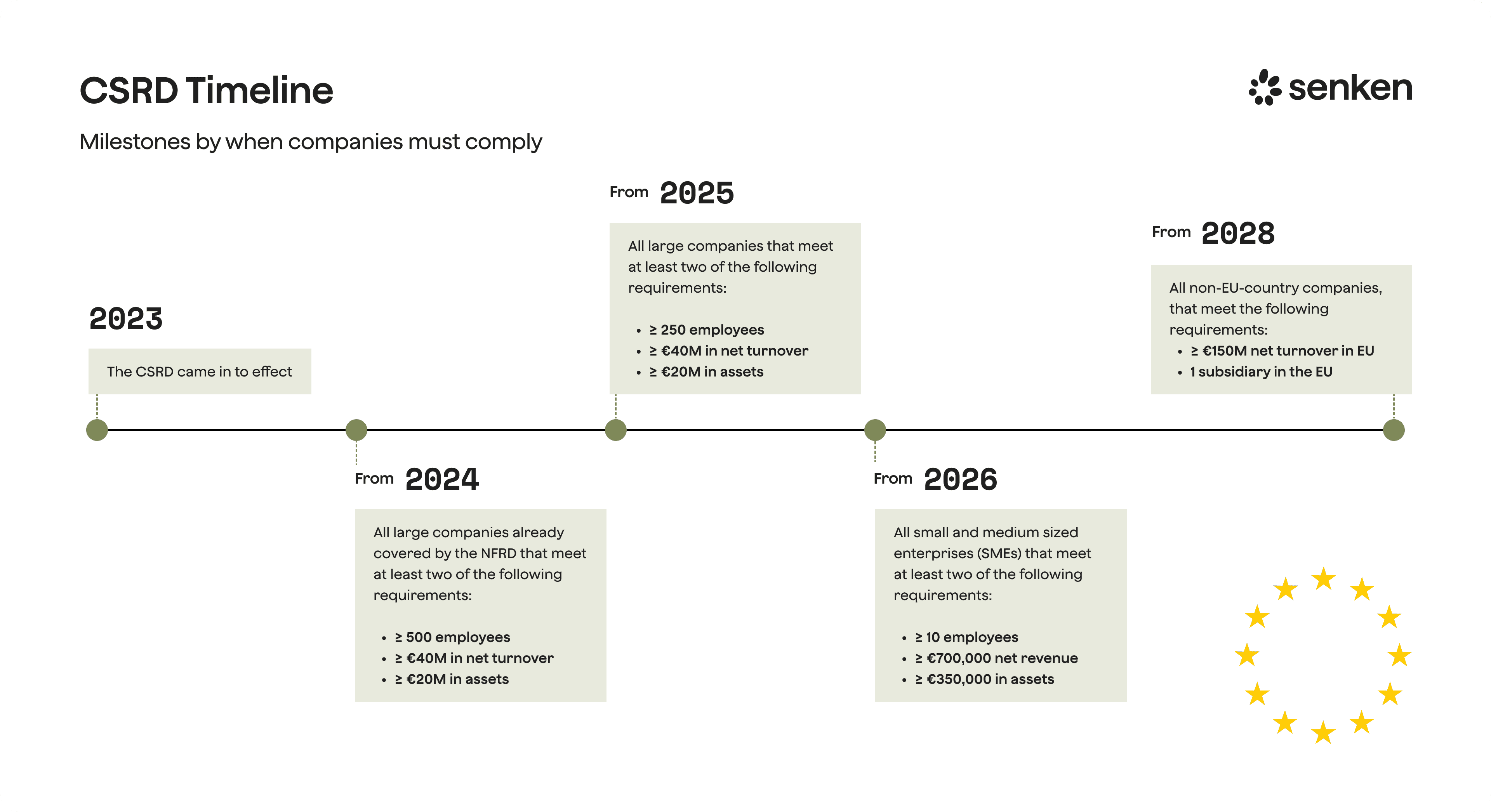

The EU Carbon Removals Certification Framework—or CRCF for short—is a voluntary EU-wide regulation (formally Regulation (EU) 2024/3012) that establishes quality standards and certification rules for three types of climate activities: permanent carbon removals (like direct air capture and biochar), carbon farming (soil carbon, agroforestry, peatland restoration), and carbon storage in long-lasting products. It came into force in December 2024, with the first certification methodologies landing in 2026 and a common EU registry launching by late 2028.

If you're a Head of Sustainability at a large DACH company, CRCF matters because it's about to become the baseline for what counts as "credible" in Europe—and that baseline will shape your CSRD audits, your SBTi commitments, your board conversations, and your exposure to greenwashing risk. This article translates dense EU law into a concrete 12–24 month playbook: how to audit your current portfolio against CRCF principles, update your procurement rules, align with CSRD and SBTi, and build a defensible strategy for durable removals without ending up in the next Handelsblatt headline.

1. CRCF in two minutes: what it is and what it changes for DACH corporates

The EU Carbon Removals Certification Framework (CRCF), formally known as Regulation (EU) 2024/3012, is a voluntary EU-wide certification system for carbon removals, carbon farming, and carbon storage in products. Entering into force in December 2024, CRCF sets a common quality baseline across the bloc for activities that pull CO₂ from the atmosphere or reduce soil emissions. By 2026, the Commission will publish the first certification methodologies for permanent removal technologies (DACCS, biochar, BECCS) and carbon farming practices (agroforestry, peatland restoration, afforestation). By December 2028, a unified EU registry will track every certified unit, ensuring full traceability and preventing double counting.

For a DACH Head of Sustainability, CRCF is less a policy curiosity and more an operating system upgrade. It will quietly shape what "high-quality" means in Europe, influence CSRD assurance expectations, and interact tightly with SBTi's evolving net-zero rules and VCMI's Claims Code. Here's what this means for your next 12 to 24 months:

- Review your current portfolio. Map existing credits to CRCF categories (permanent removals, carbon farming, product storage). Identify segments that may not qualify under future CRCF methodologies or ICVCM standards.

- Plan for CRCF-aligned removals. Start securing early offtakes for durable removal types that will carry CRCF certification, such as biochar or pilot DACCS/BECCS projects, to manage scarcity and price risk.

- Update your claims strategy. Align public statements with DACH enforcement reality. Germany's Federal Court of Justice ruled in June 2024 that "klimaneutral" claims are ambiguous without in-ad clarification. CRCF certification alone does not make strong claims safe.

- Prepare CSRD-ready evidence. CRCF's four-unit typology and quality criteria will help structure ESRS E1-7 disclosures on financed removals and reductions, but you must still separate gross emissions from purchased credits.

CRCF does not replace your internal due diligence. It is a floor, not a ceiling. Companies serious about avoiding the next greenwashing headline in Germany or Switzerland will layer CRCF with deeper quality filters, like Senken's Sustainability Integrity Index, and conservative claim language.

2. The CRCF regulation in plain language: scope, categories and quality bar

2.1 Three activity categories and four CRCF unit types

CRCF organizes carbon activities into three families, each with distinct crediting rules:

Permanent carbon removals capture atmospheric or biogenic CO₂ and store it for "several centuries." Think DACCS (direct air capture with storage), BECCS/BioCCS (bioenergy or bio-based CO₂ capture with geological storage), biochar, enhanced rock weathering, and certain ocean-based methods. These generate Permanent Carbon Removal Units, one per tonne of CO₂e, with no expiry.

Carbon farming covers land-based practices over activity periods of at least five years that either sequester carbon in soil and biomass or reduce soil GHG emissions. Examples include peatland rewetting, agroforestry, cover cropping, conservation tillage, and afforestation. These generate two temporary unit types: Carbon Farming Sequestration Units (for carbon stored in biogenic pools) and Soil Emission Reduction Units (for net emission cuts from soils). Both units expire at the end of the monitoring period unless the methodology allows prolongation.

Carbon storage in products locks up atmospheric or biogenic CO₂ in long-lived goods, typically wood-based construction materials, for at least 35 years with on-site monitoring. These generate Carbon Storage in Product Units, which also expire at the end of the monitoring period.

This typology forces clarity. Your finance and legal colleagues can now ask: "Is this a permanent unit or a temporary one?" and "What is the monitoring period and reversal liability?" That transparency is the point.

2.2 CRCF quality criteria and why they matter more in DACH

CRCF embeds four quality tests into every methodology:

- Quantification and MRV. Net benefit must be positive, calculated from a robust baseline, total removals or reductions, and lifecycle GHG emissions (including indirect land-use change), with conservative treatment of uncertainty.

- Additionality. The activity must go beyond existing EU or national law at the operator level and require the incentive of certification to be financially viable. Standardised baselines can satisfy additionality automatically; otherwise, methodologies specify the test.

- Storage, monitoring, and liability. Operators face ongoing monitoring obligations, must mitigate reversal risks, and carry appropriate liability (buffers, insurance) for any reversals during the monitoring period.

- Sustainability safeguards. Activities must "do no significant harm" and may deliver co-benefits in climate, water, biodiversity, and socio-economic dimensions. Carbon farming must deliver at least one biodiversity or ecosystem co-benefit by design.

Why does this rigour matter more in Germany, Austria, and Switzerland? Because enforcement and media scrutiny are intense. The German BGH ruling in June 2024 made clear that "klimaneutral" is ambiguous: companies must clarify in the ad itself whether neutrality comes from reduction or compensation, and a QR code is not enough. Switzerland's Fairness Commission has deemed "climate-neutral" claims generally unfair without robust, accepted methods. CRCF's MRV backbone, registry traceability, and liability rules reduce some structural risks, but they do not eliminate the need for conservative claims and layered due diligence.

3. What actually qualifies: CRCF-eligible removals and carbon farming you can buy

3.1 Permanent carbon removals (DACCS, BECCS/BioCCS, biochar, enhanced weathering)

The Commission prioritises DACCS, BECCS/BioCCS, and biochar for the first wave of 2026 methodologies. These are the technologies that deliver "several centuries" of storage:

- DACCS (direct air capture with geological storage) is the gold standard for permanence but remains expensive and supply-constrained. Expect prices in the hundreds of euros per tonne through 2030.

- BECCS and BioCCS (capturing biogenic CO₂ from bioenergy or bio-industrial processes) offer near-permanent storage at lower cost than DACCS, and Microsoft's 2025 mega-offtake showed large volumes are contractable.

- Biochar (pyrolyzed biomass) stores carbon for hundreds to over a thousand years and is the most mature durable CDR pathway today. CDR.fyi reports biochar led deliveries in 2025, with around 0.68 Mt delivered and 0.33 Mt retired by mid-year. It is the practical entry point for many DACH buyers.

- Enhanced rock weathering accelerates natural mineral reactions to sequester CO₂. Methodologies are under development; expect these to follow biochar and BECCS in the CRCF pipeline.

Market reality: removals credits traded at an average 381% premium over reduction credits in 2024, and durable CDR remains scarce. The State of Carbon Dioxide Removal 2024 estimates only around 1.3 Mt/yr of novel CDR today versus 7 to 9 Gt/yr required by mid-century. Early action secures supply and locks in today's pricing before scarcity tightens further.

3.2 Carbon farming and carbon storage in products: what to expect first

The 2026 methodology roadmap includes agriculture and agroforestry, peatland rewetting, and afforestation, all generating temporary units with monitoring periods typically 5 to 30 years. These credits will carry expiry dates synchronized to project timelines and explicit reversal liability for forest fires, land-use change, or abandonment.

Carbon farming offers nearer-term volumes, lower prices, and strong co-benefits (biodiversity, soil health, water retention), making it suitable for contribution and BVCM-style claims. However, temporary units do not meet SBTi's permanence bar for neutralization at net-zero. Plan to use them for ongoing emissions responsibility or philanthropy, not as replacements for aggressive reduction.

Carbon storage in products, focused on wood-based building materials, is still emerging. The Commission has signaled methodologies for construction and timber products will follow the first wave. Expect these to mature post-2026.

Practical takeaway: by 2030, you can assemble a CRCF-aligned portfolio blending biochar and select engineered removals for long-term neutralization needs, plus high-quality carbon farming for short-term contribution claims and co-benefits, all under a unified EU quality and registry framework.

4. Bringing CRCF into your company: portfolio audit, procurement rules and governance

4.1 Audit your existing carbon portfolio against CRCF and ICVCM principles

Start with a simple three-step process:

- Map existing credits and offtakes to CRCF categories. For each project in your portfolio, ask: Is this a permanent removal, carbon farming, product storage, or an avoidance/reduction credit outside CRCF scope? Assign an indicative CRCF unit type.

This audit is not about perfection. It is about visibility and risk management. Even if parts of your current portfolio fall short, mapping them now prevents nasty surprises in a 2026 CSRD audit or a media investigation.

4.2 Design CRCF-aligned procurement rules and embed them in approvals

Translate CRCF into internal policy language. For example:

- Minimum durability. For neutralisation use cases (SBTi net-zero residuals), procure only permanent removals (CRCF permanent units or equivalent) with >200 years storage, in line with Oxford Principles.

- Acceptable methodologies. Specify CRCF-eligible or CRCF-certified project types. Exclude methodologies flagged by ICVCM (e.g., renewable energy) or with poor external ratings (BeZero, Sylvera below BBB).

- Required documentation. Mandate project design documents, verification reports, and evidence of registry issuance. For CRCF-certified units, require proof of certification body accreditation and methodology compliance.

- Approval gates. Route purchases above a threshold (e.g., €50k or 10,000 tCO₂e) through a cross-functional review (sustainability, procurement, legal, communications) to check CRCF alignment, reputational risk, and claim compatibility.

Senken's Sustainability Integrity Index fits into this process as an extra risk filter on top of CRCF certification. With fewer than 5% of assessed projects passing Senken's screens, layering this discipline reduces your greenwashing exposure and strengthens audit readiness.

5. How CRCF fits with CSRD/ESRS E1, SBTi and VCMI in a DACH context

5.1 CRCF units in CSRD and ESRS E1 reporting (what counts where)

Under CSRD, your gross Scope 1, 2, and 3 emissions must remain un-netted. ESRS E1-7 requires separate disclosure of removals in your own operations or value chain and the amount of reductions or removals financed outside your value chain via carbon credits. You must break down purchased credits by type (reduction vs removal, permanent vs temporary), geography, standard/registry, and methodology.

CRCF makes this easier. The four unit types map cleanly to ESRS categories: permanent removal units, two types of temporary carbon farming units, and product storage units. The EU registry's transparency and traceability will provide auditors with the granular evidence they expect.

Critically, CRCF units do not reduce your reported gross emissions or count toward E1-4 target achievement. They support your E1-7 disclosure on climate finance beyond the value chain and may strengthen your transition-plan narrative, but they are not offsets in the accounting sense. This separation is intentional and strictly enforced under ESRS.

5.2 CRCF and SBTi/VCMI: neutralisation, BVCM and voluntary claims

SBTi currently prohibits carbon credits for near-term or long-term reduction targets. At net-zero, residual emissions must be neutralised with permanent removals. SBTi's V2 revision (expected 2026-2027) will introduce "ongoing emissions responsibility" recognition and clarify interim removal factors, but the permanence requirement for neutralisation will remain.

CRCF permanent removal units align well with SBTi's neutralisation bar. Temporary CRCF units (carbon farming, product storage) likely qualify for BVCM or ongoing emissions responsibility recognition but not for neutralisation, pending final SBTi V2 rules.

VCMI's Claims Code allows companies to make Carbon Integrity Claims (Silver, Gold, Platinum) and a Scope 3 Claim if they retire high-quality credits in specified proportions of remaining emissions. CRCF-certified units can underpin these claims, provided they meet VCMI's quality screens and any corresponding-adjustment criteria.

Overlay DACH enforcement: Germany's BGH ruling means any "klimaneutral" statement must clarify the mix of reduction and compensation in the ad itself. CRCF certification gives you a credible quality signal, but it does not automatically make strong claims safe. Adopt conservative language ("contributing to climate neutrality," "supporting removals beyond our value chain") and reserve unqualified "net-zero" or "klimaneutral" claims for scenarios where SBTi, VCMI, and DACH legal standards all align.

6. Beyond the CRCF baseline: quality, reputational risk and a 24-month roadmap

6.1 Why CRCF is a floor, not a guarantee of integrity

CRCF sets a harmonized baseline, but it is not a silver bullet. NGO assessments from Carbon Market Watch and Oeko-Institut flag risks: delegation of technical choices to schemes may create inconsistencies, additionality tests and permanence/liability designs will vary by methodology, and leakage accounting may be insufficiently specified.

Buyers should ask:

- Does the methodology use conservative baselines and account for indirect land-use change?

- Are buffer pools or insurance adequate for reversal risk?

- Are co-benefits and potential harms (land rights, biodiversity trade-offs) transparently reported?

- Does the certification body have a track record of rigorous audits?

Senken's Sustainability Integrity Index adds over 600 data points on carbon impact (additionality, permanence, leakage), co-benefits (soil, water, biodiversity, livelihoods), MRV robustness, and reputation. This layered approach closes gaps CRCF leaves open, giving you defensible quality for CSRD assurance, investor scrutiny, and DACH media environments.

6.2 A pragmatic 2025-2030 CRCF-aligned roadmap for DACH corporates

Here is a 12 to 24-month checklist:

- Complete your CRCF and SII portfolio audit (Q1-Q2 2025). Map current credits to CRCF categories, flag high-risk segments, and quantify the share that will qualify under future CRCF methodologies.

- Set a 2030 target mix of permanent vs temporary removals. Align this with your SBTi net-zero plan (permanent removals for neutralisation) and VCMI or BVCM strategy (temporary units for contribution).

- Adopt a CRCF-plus quality policy. Define minimum standards (CRCF-eligible + ICVCM CCP + Senken SII or equivalent) and update procurement, approvals, and internal carbon pricing rules.

- Secure early offtakes for durable removals. Lock in biochar or pilot DACCS/BECCS contracts at today's pricing (around €50-€100/tonne for biochar) before scarcity drives costs to €150+/tonne by 2030.

- Integrate CRCF into CSRD reporting design. Build your E1-7 disclosure templates around CRCF unit types, permanence, and geography now, so 2025 and 2026 reports are audit-ready.

- Update claim language and risk registers. Reflect DACH case law, CRCF categories, and unit expiry in marketing and investor communications. Flag greenwashing risk in your enterprise risk register and assign ownership.

The carbon removal market is undersupplied and will remain so for years. Companies that wait for "cheaper removals" miscalculate. By acting now, you secure access, lock in costs, and build an operating model that passes audit and avoids greenwashing risk. CRCF is the common language Europe will speak; the question is whether you speak it fluently or scramble to learn it under pressure.