Buying Blind? Introducing our Analysis of DAX40 Carbon Credit Disclosures under CSRD

Today, together with Sylvera, we are publishing Buying Blind?, the first independent analysis of how Germany's largest public companies disclosed their carbon credit purchases under the Corporate Sustainability Reporting Directive (CSRD). You can read the full report at senken.io/buying-blind.

The report is the result of three months of work. We extracted the carbon credit section of every FY2025 CSRD filing published by a DAX40 company by April 1st, 2026, traced as many of the reported credits as we could across seven public registries, cross-referenced California AB 1305 filings and corporate websites, and then asked Sylvera to independently rate the projects we managed to identify. The result is, as far as we know, the most comprehensive picture available of what European corporate carbon credit reporting actually contains under the new disclosure regime.

The headline is that it contains a great deal less than most readers would assume.

Key findings

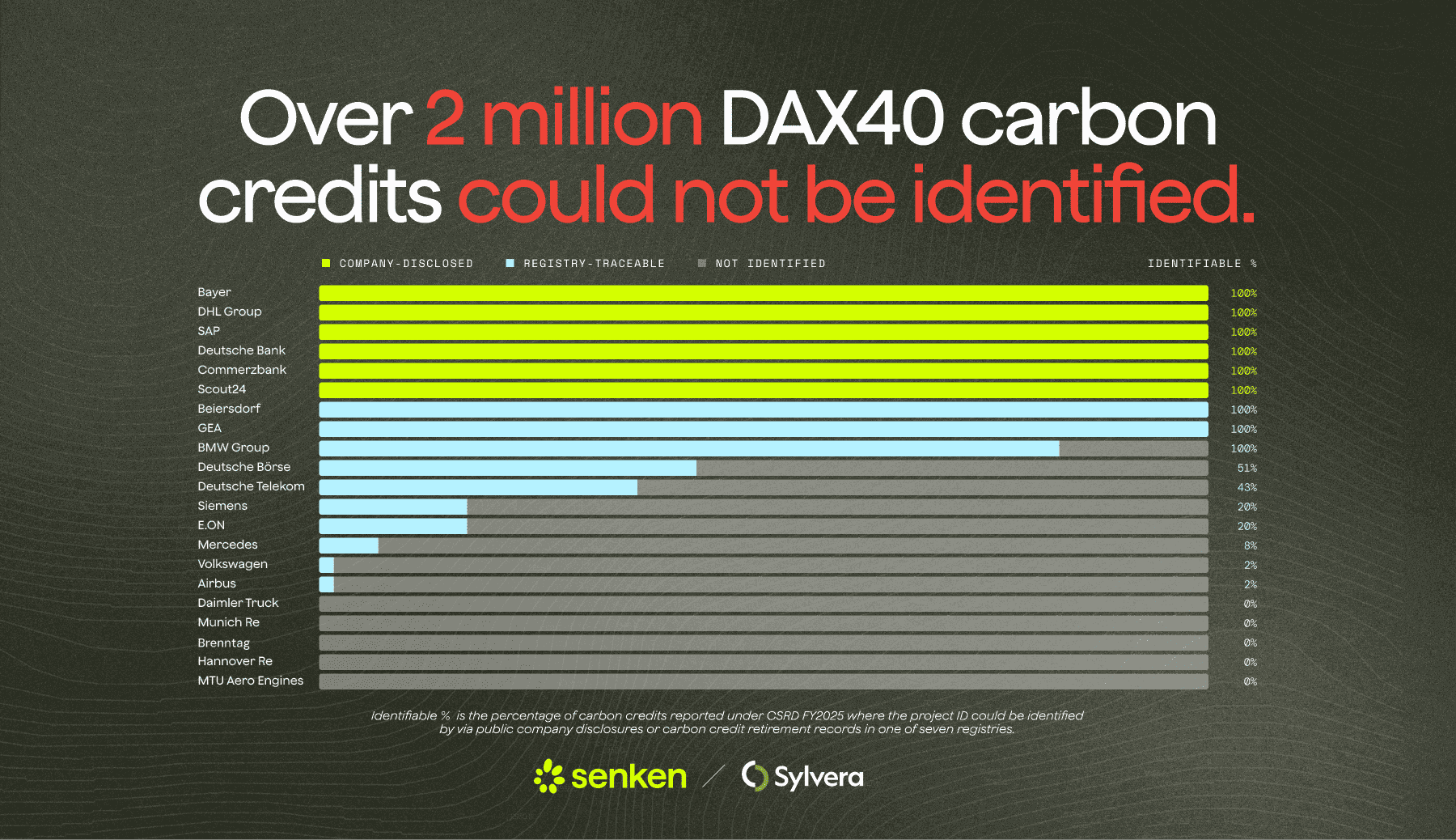

- Zero of 39 DAX40 companies disclosed a project identifier in their FY2025 CSRD filing. ESRS E1-7 does not require it, and almost no company has chosen to volunteer the information.

- 2.17 million credits, equivalent to 45% of all DAX40 reported volume, could not be traced to any specific project through seven public registries or any other public source we searched.

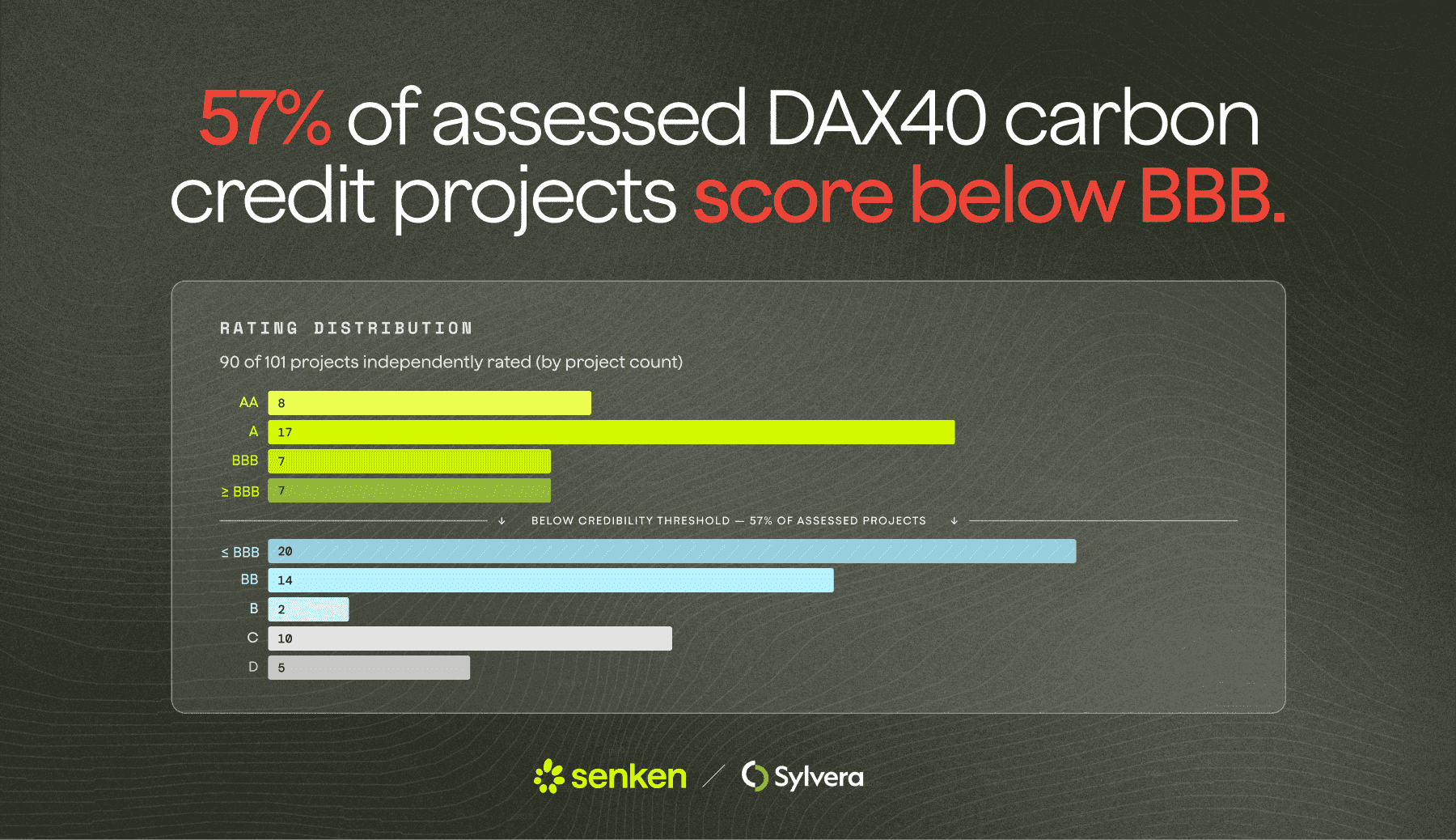

- 57% of independently rated projects scored below BBB, the minimum threshold Sylvera considers credible for climate impact. Most below-threshold volume sits in methodology categories the ICVCM has already declined to approve under its Core Carbon Principles.

- Only 6 of 21 active buyers disclose project-level detail through any public source. Four do so voluntarily (Bayer, DHL Group, Commerzbank, Scout24). Two are required to under California's AB 1305 (SAP, Deutsche Bank).

- Less than 1% of DAX40 carbon credit volume comes from EU-based projects, despite the EU's push to build out a domestic carbon removal market under the CRCF framework.

The full data, scorecard, methodology and project-level analysis are in the report, available at senken.io/buying-blind.

Why this matters

When ESRS E1-7 came into force for FY2025 reports, it represented a meaningful step forward for transparency in European corporate carbon credit reporting. For the first time, every large EU company was required to disclose how many credits it had purchased, which standards those credits sat under, and the split between removal and reduction. That is more than most companies were disclosing before, and a real improvement on a status quo in which carbon claims often had to be pieced together from press releases and broker hints.

But the standard, in its current form, stops well short of what would let any outside reader independently verify those claims. It does not ask for the project identifiers that allow a credit to be looked up in a registry, the vintages that determine when the climate benefit was claimed, the methodologies that govern how the project was measured, the countries the projects sit in, or the quality ratings an independent assessor would attach to them. As a result, two companies reporting the same headline numbers, one with a portfolio of high-integrity removals and one with a portfolio of cookstove programmes rated below the credibility threshold, look indistinguishable in their CSRD filings.

That gap is what the report sets out to document.

This is not a story about bad actors

It would be easy, and lazy, to read the report as an indictment of the DAX40 companies in it. We do not think that reading holds. The companies in the analysis are, by and large, complying with the regulation they are subject to. Their procurement teams are buying the credits that meet the standards on offer. Their sustainability teams are filing what the disclosure regime requires. Their auditors will sign off on those filings without difficulty. That is the system working as designed.

The issue is that the system, as designed, asks too little of the public disclosure to make it independently meaningful. Aggregate volume and a registry name are not enough to assess quality. A registry name is not a quality signal on its own: within Verra and Gold Standard, the same label sits behind projects rated AAA and projects rated D. Without project-level information in the public filing, a reader has no way of knowing which one a given company actually bought.

This matters because scrutiny on corporate carbon credit claims is rising, not falling. Boards are starting to ask about quality, not just volume. Auditors are sharpening their questions. Investors are pricing climate risk more carefully. Journalists are reading these filings closely. The companies that can confidently answer the questions "which projects?" and "what quality?" will be in a meaningfully stronger position than those that cannot.

Europe's largest companies reported 4.84 million carbon credits under CSRD, but none disclosed the project identifiers needed to verify them. The current ESRS E1-7 creates the illusion of transparency without enabling it.

— Adrian Wons, CEO and Co-Founder, Senken

The amendment we would like to see

The report ends with one specific policy recommendation. ESRS E1-7 should be amended to require project-level disclosure alongside the aggregate volumes it already mandates. The fields are not exotic: project identifier, country, vintage, methodology and supplier. Every company that has retired a credit already has all of this information in its procurement records. The amendment imposes no additional data collection burden.

The closest working example sits across the Atlantic. California's AB 1305 already asks for a more detailed disclosure than CSRD, and the companies subject to it have no difficulty producing it. The information was always there; California's regulation simply asked for it. A similar requirement could be added to ESRS E1-7 in time for the FY2026 reporting cycle, and we believe there is every reason to do so. If the amendment lands, next year's reports arrive with verifiable carbon claims and the questions journalists, auditors and investors are increasingly going to ask can be answered from the filing itself. If it does not, the same analysis will produce the same findings a year from now.

The data in this report reflects something we see consistently: certification and credibility are not the same thing. As carbon markets mature and demand tightens on higher-quality supply, the ability to verify quality at the project level becomes essential.

— Allister Furey, CEO and Co-Founder, Sylvera

What companies preparing FY2026 filings can do now

Waiting for the regulation to catch up is the slowest option, and not necessarily the best one. The DAX40 companies already publishing project-level detail voluntarily are not doing so because they have been forced to. They are doing so because they have concluded that being able to defend the portfolio is more valuable than the small competitive risk of disclosing it. As the market matures, that judgement looks increasingly correct.

Sylvera's most recent market data points in the same direction. Investment-grade credits (BBB+) are now trading at an average of $20.10 per tonne, up from $18.10 a year ago, while B-rated credits have fallen from $8.50 to $7.80 over the same period. The premium for high-quality, verifiable supply is widening, and the discount for lower-rated volume is hardening. In transparency-mature markets the same pattern is visible at the buyer level: UK retirements moved from 37% high-rated in 2022 to 85% high-rated by the first quarter of 2026. US and Canadian buyers improved from 21% to 68% over the same period. The buyers who got ahead of disclosure pressure early are now in a structurally stronger position.

For European companies preparing their FY2026 CSRD filings, three things are worth thinking about. The first is to publish project-level detail voluntarily, even where ESRS E1-7 does not yet require it. The data is already in procurement, the editorial cost is small, and the benefit is a portfolio that holds up to any future scrutiny. The second is to treat an independent project rating as part of procurement rather than a post-hoc check, particularly for credits intended to support a Net Zero or SBTi-aligned claim. The third is to move carbon credit quality out of procurement and into the same governance structure as other material sustainability disclosures, where it can be tested, documented and defended on the same terms as the rest of the report.

Read the report

Buying Blind? is the most detailed picture we have been able to assemble of what corporate carbon credit reporting actually contains under CSRD. It covers all 39 FY2025 filings included in the analysis, the full project-level dataset across 43 countries, the DAX40 scorecard mapping every active buyer across five dimensions of transparency and quality, the SAP CSRD versus AB 1305 comparison in full, the complete methodology, and the limitations of the analysis.

It is the first independent analysis of its kind in Europe. We hope it will be the first of many. Read the full report at senken.io/buying-blind.

If your own company appears in the dataset and you would like a private trace of your portfolio against the same methodology, get in touch.