ESRS Standards

What are the European Sustainability Reporting Standards (ESRS)?

The European Sustainability Reporting Standards (ESRS) were developed as a crucial part of the Corporate Sustainability Reporting Directive (CSRD) to standardise and enhance transparency in sustainability reporting across the European Union. These standards aim to bring sustainability reporting to the same level as financial reporting by providing a framework that ensures consistency and reliability in the disclosure of environmental, social, and governance (ESG) information by companies.

Key Components of the ESRS

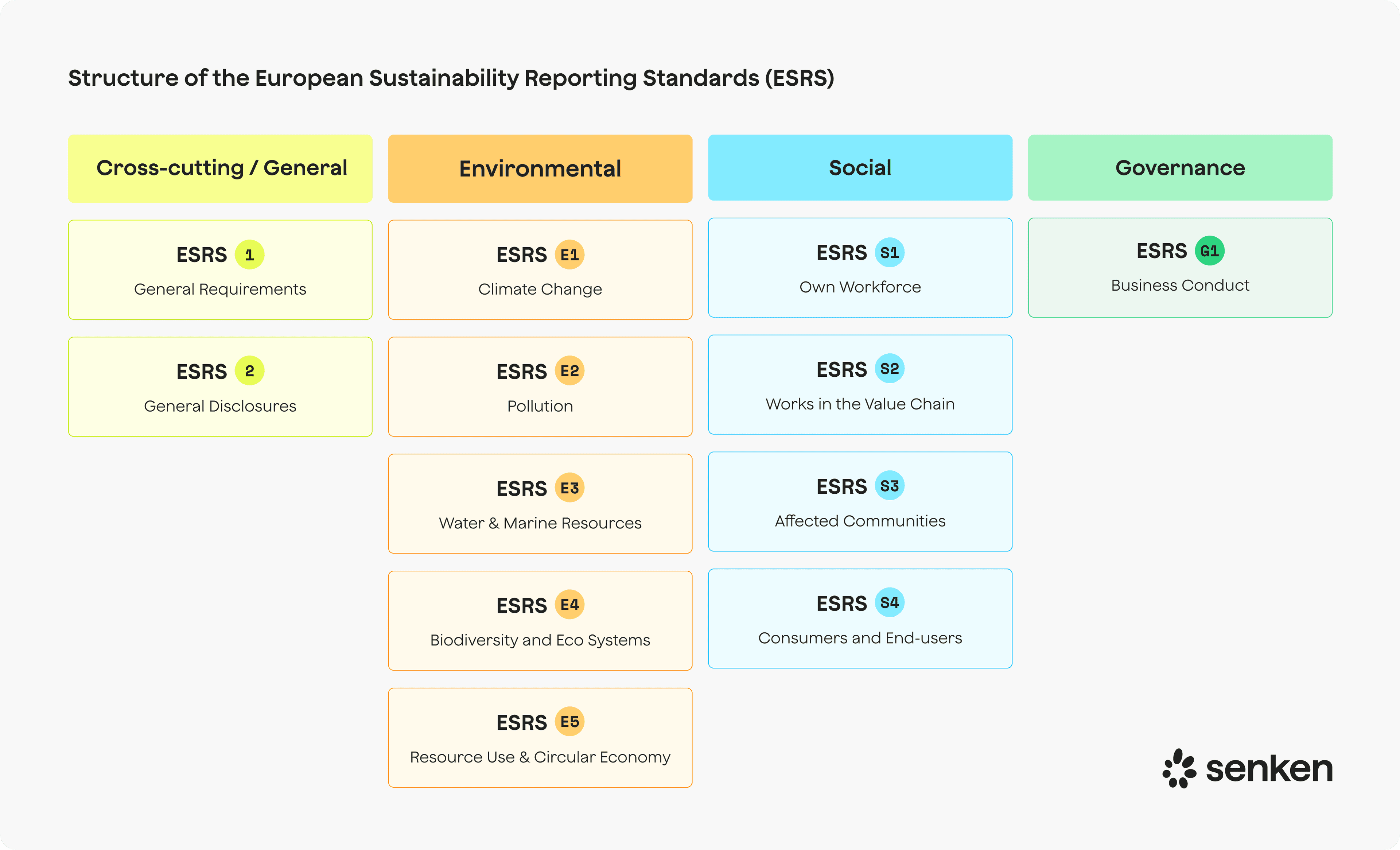

The ESRS framework includes a set of standards that cover a wide range of ESG topics. These are divided into cross-cutting standards which provide general principles and reporting requirements, as well as topical standards, which address specific sustainability issues like climate change, biodiversity, and social welfare. This structure helps organisations integrate ESG considerations into their business processes and strategic decision-making, enabling stakeholders to assess the sustainability performance of companies more effectively.

Implementing the ESRS

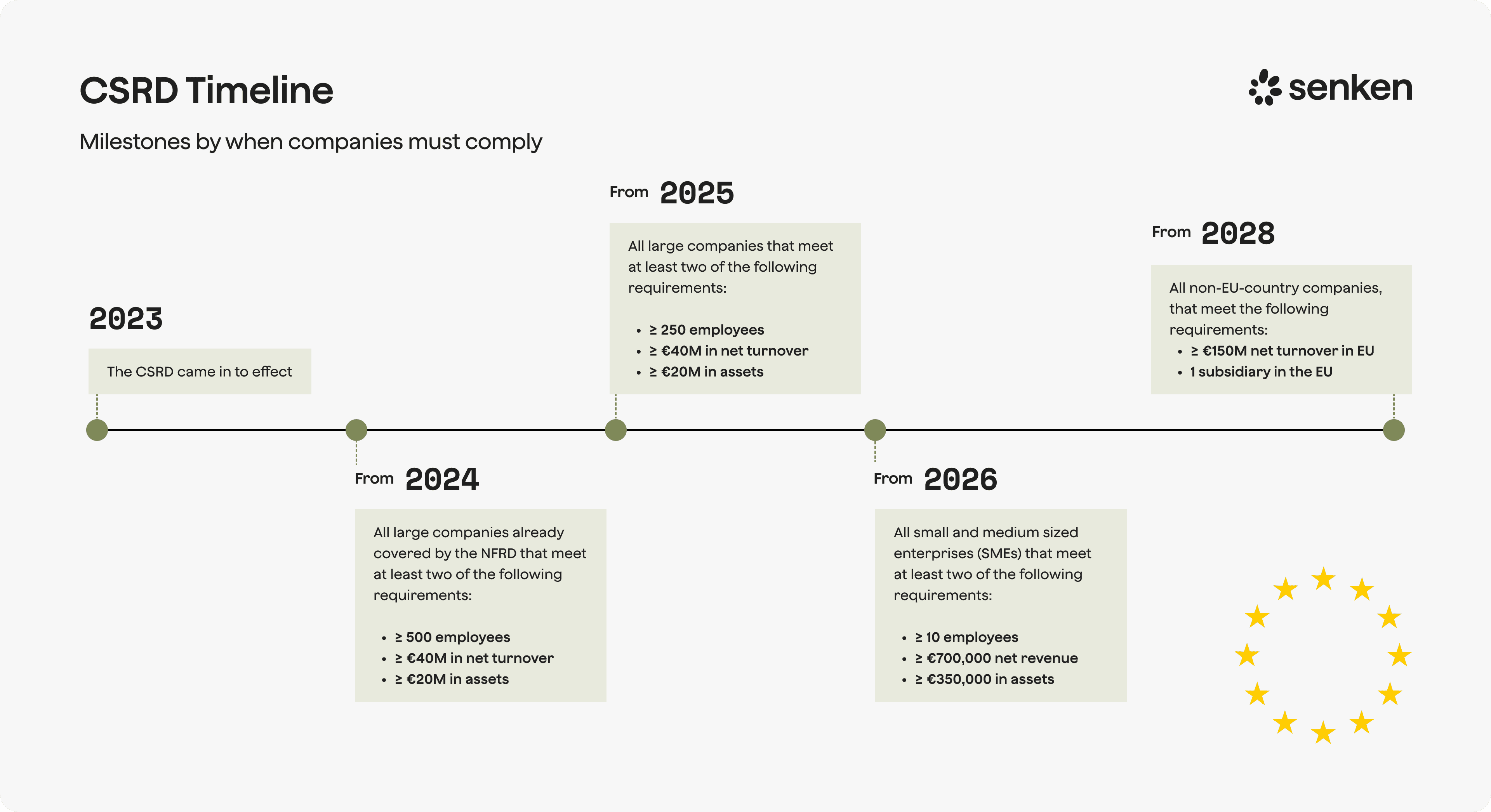

Implementation of the ESRS requires companies to prepare and publish a sustainability report alongside their annual financial report. This statement must include detailed disclosures on governance, strategy, and impact management, reflecting the company's performance and impact on sustainability matters. The ESRS adoption is phased, starting with large companies and gradually including SMEs and non-EU companies with significant operations within the EU.

Challenges and Opportunities in Adoption

Adopting the ESRS presents both challenges and opportunities for companies. They must ensure they have robust systems for data collection and reporting, particularly on complex topics such as biodiversity and the circular economy. The requirement to report based on the "double materiality" concept—considering both the impact of the company on sustainability matters and the impact of sustainability matters on the company—adds a layer of complexity but also a significant opportunity to enhance sustainability practices and transparency.

Regulatory Landscape and Strategic Frameworks

The ESRS are designed to align with other international reporting standards to ensure global interoperability, such as those developed by the Global Reporting Initiative (GRI) and the International Sustainability Standards Board (ISSB). This alignment helps companies that operate globally to streamline their reporting processes and avoid duplication of effort. As the standards evolve, they are expected to play a pivotal role in shaping the sustainability reporting landscape in Europe and beyond, influencing how companies worldwide approach ESG reporting.