12 Carbon Credit Providers Compared in 2026: a selection guide for companies

The short answer

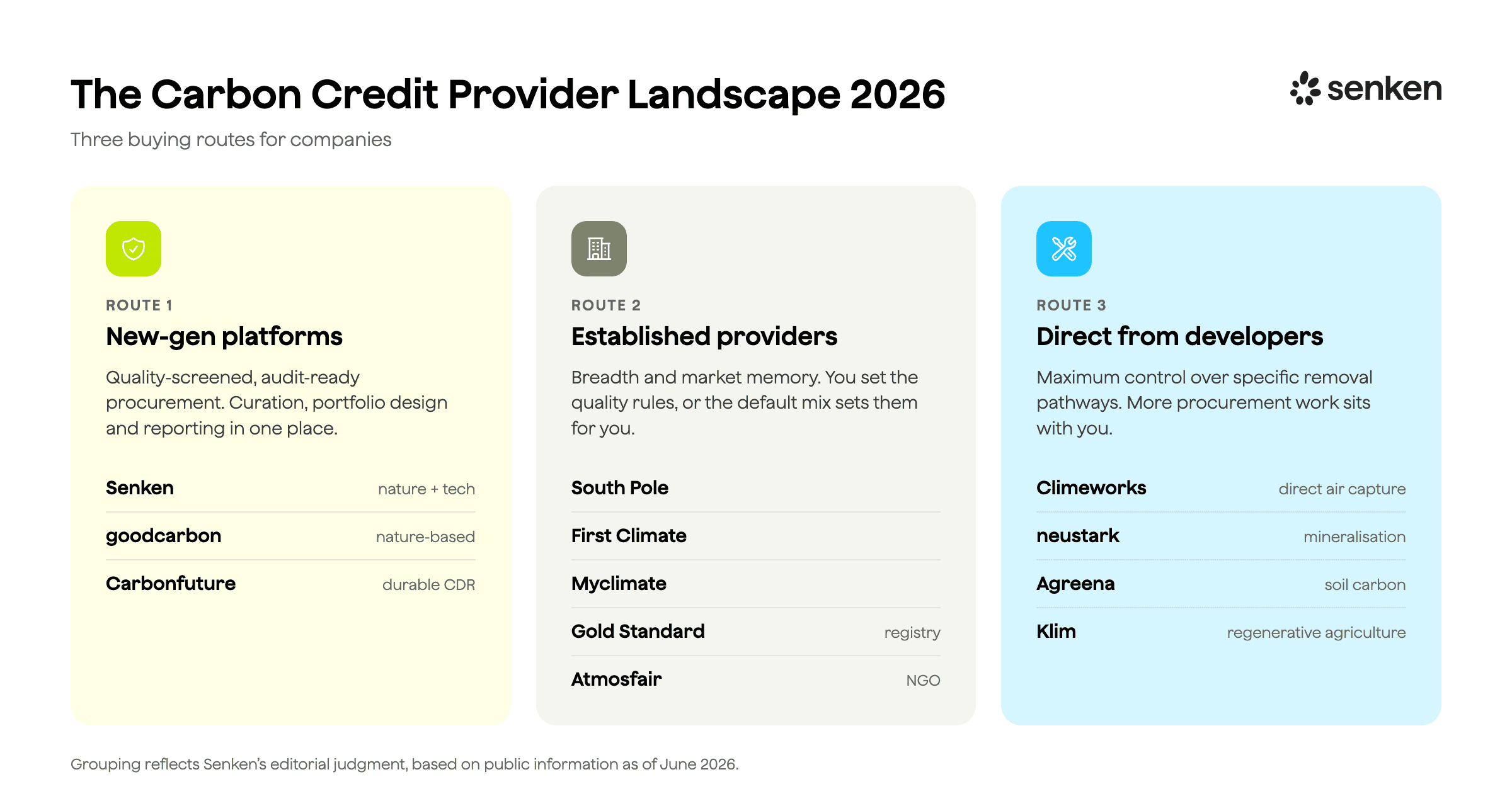

Companies buy carbon credits through three routes in 2026: new-generation procurement platforms (Senken, goodcarbon, Carbonfuture), established offset providers (South Pole, First Climate, Myclimate, Gold Standard, Atmosfair), and direct deals with project developers (Climeworks, neustark, Agreena, Klim). In our assessment, new-generation platforms fit most corporate buyers because they combine quality screening, portfolio design and audit documentation in one place. Established providers bring breadth and market memory, if you set the quality rules yourself. Direct developer deals give the most control over specific removal pathways, and the most procurement work. The comparison table below maps all twelve to the job they do best.

Why the route matters more than the project

Most carbon credit problems do not start in a forest or a kiln. They start on a route. The provider looked fine on a slide, terms were fuzzy, evidence sat in five folders, and a few months later you are defending choices you barely remember. The way you buy sets price stability, delivery risk, the cleanliness of your audit trail, and even the claims you can make in public. Pick a good route and the work gets quiet: predictable deliveries, tidy files, fewer surprises.

And yes, every provider promises the same three things: quality, good price, and easy reporting. Spoiler: they don’t deliver the same way. What actually separates them is less glamorous and more practical: how they curate projects, how transparent they are on price, whether their tech makes reporting trivial or painful, how deep their local knowledge runs, and how they manage risk when the world moves. We’ll use those differences to make clear choices based on the job you need done.

Jobs to be done (choose your lane)

Pick a primary job for this year. Maybe a secondary for resilience. Trying to do everything is how files get messy. I’ll also show which differentiation dimensions matter most for each job so you can see where providers actually diverge.

Contribution now and communication.

Sometimes you need a credible story this quarter. The right shape is simple: high-quality projects, on-time delivery, and evidence that your auditor can follow. Finance gets cost control; Comms gets clear language and, if needed, local angles. Teams slip when they buy cheap and don’t verify the data. Here, quality assessment, strategy design and project curation philosophy (what’s in/out and why) carry the most weight.

Durable removal ramp.

You’re paying more per ton for permanence, so treat it like a capital program. Stage commitments against milestones, spread delivery risk across a small basket, and make MRV and buffer rules explicit for each method. Teams run into trouble jumping straight from zero to long-term offtakes without the internal plumbing, or treating all removals as equal. They aren’t. The heavy hitters here are project curation philosophy (how they judge permanence/additionality), risk management (offtake structure, replacements), and geographic expertise (permits, regulatory nuance, public language in DACH).

Audit-ready CSRD reporting.

Assurance is getting real. PDFs in a folder won’t cut it. Our own DAX40 analysis found 45% of disclosed credits untraceable to a specific project. You need traceability from contract to retirement, evidence mapped to ESRS topics, and exports your reporting stack can use. Problems start when you mix vendors whose data doesn’t align, or when you rely on glossy certificates with no underlying structure. This job is mostly about quality assessment, technology/UX (data model, registry sync) and curation philosophy (so Legal trusts the claims).

Portfolio experimentation and learning.

Early stage is fine. Just be clear that the goal is insight, not headlines. You want fast access to supply, clean enough reporting to pass scrutiny, and a written learning agenda: what you tested, what you learned, what you’ll change. Here, strategy design (learning), technology/UX (comparability), curation (quality without junk), and price transparency (so you can compare true cost) win.

“Get the cheapest price per ton.”

Let’s be blunt. Optimising for €10/t as the main job is usually buying a headline risk and a paper claim. 2023’s average voluntary-market price was around $6.53/t (Ecosystem Marketplace, State of the Voluntary Carbon Market 2024), but that average hides wide variation: buyers have been concentrating demand in pricier, higher-integrity segments while the very cheapest categories have faced the harshest scrutiny. Regulators and watchdogs are also tightening the screws on “carbon-neutral” claims built on cheap offsets: the UK’s ad regulator now expects clear, proximate disclosures on the basis of such claims (how much is reduction vs. offset, and on what grounds), and Germany’s Federal Court of Justice has ruled that vague “klimaneutral” advertising misleads unless the mechanism is explained in the ad itself. In practice, “cheapest” tends to mean “hardest to defend.” Plan for comms and legal load if you take this path. The net effect is simple: cheap credits often carry reputational overhang. If you still want the lowest price, treat it as a conscious trade-off and build extra risk controls into your route.

Now that we’ve defined the jobs, let’s explore the providers for each.

The 12 providers at a glance

| Provider | Route | Project focus | Pricing signal | Best for |

|---|---|---|---|---|

| Senken | New-gen platform | Nature- and tech-based, Europe + verified Global South | Custom quote, line-item fee breakdown | One partner covering several jobs, audit-ready CSRD reporting |

| goodcarbon | New-gen platform | Nature-based, mostly Global South | Custom quote | Nature-first portfolios with visible co-benefits |

| Carbonfuture | New-gen platform | Durable removals: biochar, BECCS, DACCS, mineralisation | Custom quote | Durable removal ramp with batch-level tracking |

| South Pole | Established provider | Broad global portfolio, reductions and removals | Spans the price spectrum; ask for fees and spreads | Contribution at scale, with bright lines set up front |

| First Climate | Established provider | Conventional portfolios, reduction and removal types | Service-led; clarify fees and re-pricing | Mid-market DACH teams wanting a nearby counterparty |

| Myclimate | Established provider | Broad catalogue, renewables and cookstoves alongside better-screened projects | Ask for fee/spread disclosure | Conservative contribution with a Swiss non-profit |

| Gold Standard | Standard & registry | Certification and registry; small marketplace | Marketplace retail prices public | Registry traceability when you bring your own due diligence |

| Atmosfair | Established provider (NGO) | Cookstoves, renewables, energy efficiency | Public rates | German documentation and co-benefit storytelling |

| Climeworks | Project developer | Direct air capture, permanent mineral storage | Above €500/t | A durable backbone with maximum permanence |

| neustark | Project developer | Mineralisation in recycled concrete, European sites | Above €200/t | Tangible, local, permanent storage |

| Agreena | Project developer | Soil carbon across European cropland (Verra VM0042) | Forward pre-orders or spot from issued vintages | European soil carbon at scale |

| Klim | Project developer | Regenerative agriculture, Germany-first | Published €50/t | German regional credits with farm-level stories |

New-generation procurement platforms

These are built around portfolio design, quality frameworks, and audit-friendly data. First, they verify quality (due diligence, MRV, third-party ratings). Then they turn that logic into science-based portfolio design you can defend: Oxford-aligned mixes, a visible ramp into durable removals, and guardrails that prevent failure. Usually, they do all of the procurement and risk-management heavy-lifting, and in case they don’t, your suspicions should rise. For DACH teams, German documentation and EU project options are normal, and the tech/UX is built for CSRD rather than slide decks.

Senken

New-generation platform, multi-jobs

At a glance. Best for: one partner covering several jobs at once, from contribution to audit-ready CSRD reporting. Focus: nature- and technology-based credits, Europe plus verified Global South projects. Pricing: custom quote, with a line-item fee breakdown on request. Trade-off: guided procurement rather than an instant self-serve checkout.

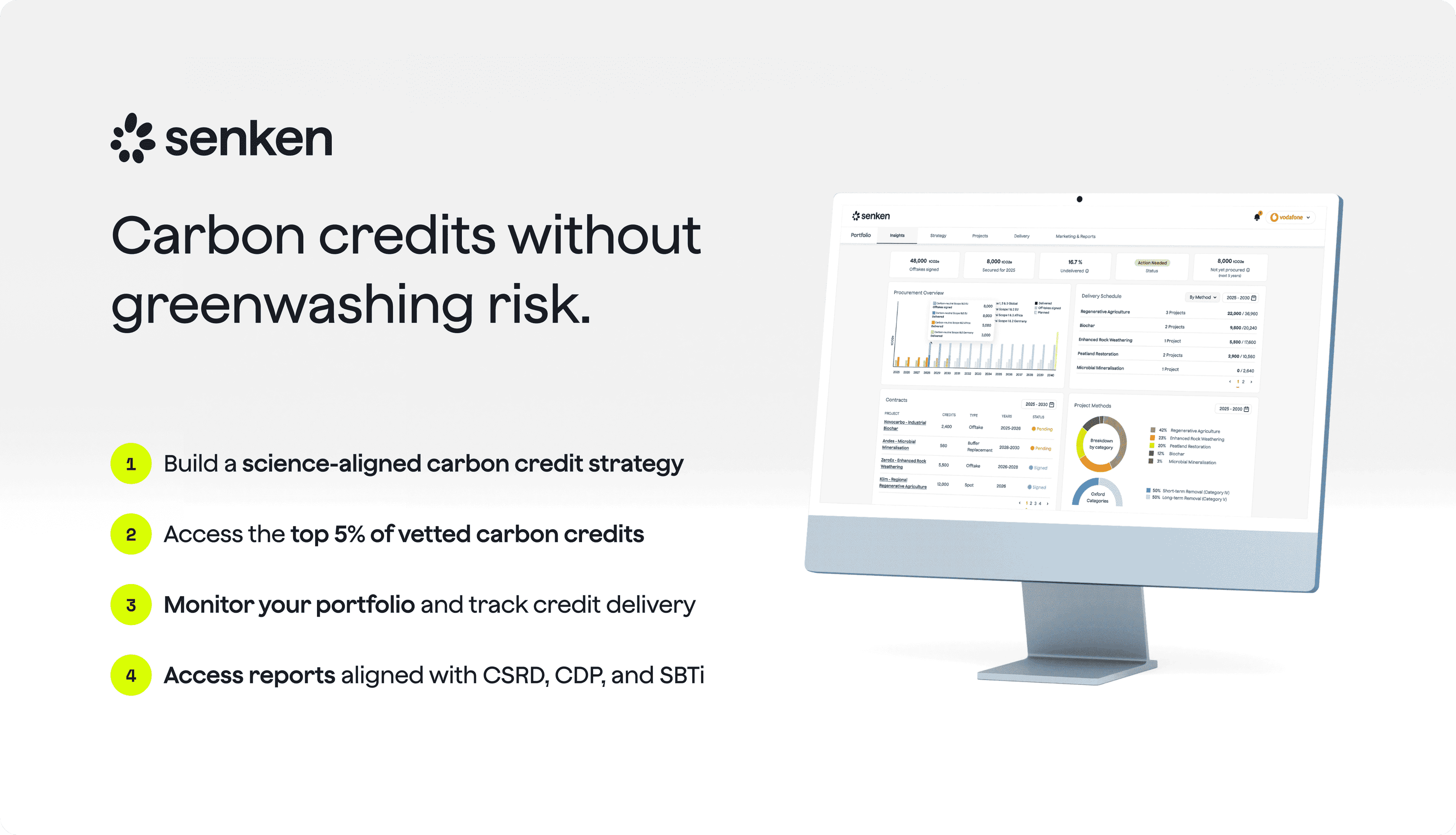

Senken is a Germany-based platform built around a simple promise: credits you can defend. Under the hood, the product revolves around a 600-data-point Sustainability Integrity Index (SII) that screens projects before they ever hit a customer’s portfolio, and a Portfolio Manager that tracks delivery, flags risk, and keeps the paper trail tidy. It is a strategy, procurement and operations layer in one place. That combination means Senken can credibly cover several jobs at once, such as contribution now, multi-year planning, removals ramp, and audit-ready reporting, without pushing you into a patchwork of tools and negotiations.

Procurement here looks like a guided search rather than a self-serve marketplace. It is shaped by Senken’s curation philosophy: exclude weak projects upfront, then advise the client on what works best for their climate goals and brand. Geographic focus usually includes Europe and selected, verified projects from the Global South. Senken covers a wide range of project methodologies, being experts in both nature- and technology-based carbon credits, making the portfolios both affordable and audit-ready.

Several large enterprises went with Senken: Vodafone Germany, Deutsche Telekom and Lufthansa Group work with Senken on their climate targets, which reflects a Quality Framework and expertise that holds up to corporate procurement standards. Yet multiple mid-sized companies also chose that route, like EV charging provider Mer and insurance company DR Walter, which shows fast lead times despite complexities under the hood.

On reporting and audits, the product is built to export cleanly from day one. All credits are traceable and cover a wide range of reporting documents (CSRD, CDP) and leading standards (VCMI, IPCC, SBTi).

Where it fits best. If you want “one partner that does it all”, contribution without drama, multi-year planning, or audit-ready data that your assurance team won’t fight, this route is strong. It’s also one of the few that can credibly span multiple jobs without breaking your operations.

Goodcarbon

New-generation platform, only nature-based projects which has its pros and cons

At a glance. Best for: nature-first portfolios with visible co-benefits and storytelling power. Focus: nature-based projects, mostly Global South. Pricing: custom quote. Trade-off: no engineered removals, and limited self-service tooling (based on public materials as of June 2026).

goodcarbon is a Berlin-based platform focused on nature-based portfolios. Think curation of forestry and land-use projects. Their positioning is clear: nature projects for the long term, high-quality credits, and support that goes beyond the logo soup of standards. The company is also a project developer itself, with deep expertise in what it takes to reduce carbon from the atmosphere.

The curation philosophy is explicitly nature-based; geographic focus mostly includes the Global South, and the narrative leans into restoration and biodiversity alongside carbon. That’s a strength if you want a nature-first portfolio with storytelling power and a structured risk view; it’s a limitation if your job is a more diversified, Oxford Principles-aligned, portfolio or a durable removals ramp into engineered pathways. In this case, you’ll likely pair goodcarbon with another platform or a project developer.

On reporting and audits, goodcarbon emphasises “advanced analytics” and “confidence beyond accredited standards,” which is the right ambition for CSRD-era scrutiny. Their public materials, as of June 2026, do not walk through the due diligence process end to end, so the practical question for your team is format and depth: do you get a full due diligence report, versioned documentation per project, and exports compatible with your reporting stack, or mostly polished PDFs and summaries? That’s not a criticism; it’s the RFP you should run. Ask for a sample evidence and a mock audit trail from contract to retirement, then check how fees, risks, and re-pricing are disclosed over multi-year horizons.

If you’re searching for a software-enabled platform that can guide you through the purchasing process: based on their public materials as of June 2026, goodcarbon’s emphasis is deep expertise in nature-based solutions and relationship-driven project curation rather than extensive self-service tooling. If those answers are crisp, the job coverage expands from contribution and learning into price coverage with nature-heavy portfolios. If they’re not, keep the engagement focused on curated sourcing plus your own data plumbing.

Where it fits best. If your stakeholders value nature projects with visible co-benefits, goodcarbon is a strong specialist. Pair it with an internal stance on claims (especially permanence language), ad-hoc due diligence and, if you need engineered removals or long-duration credits, add a second route alongside.

Carbonfuture

New-generation platform, durable removals only

At a glance. Best for: building a durable removal ramp with delivery tracked at batch level. Focus: durable removals only: biochar, BECCS, DACCS and mineralisation. Pricing: custom quote. Trade-off: no nature-based supply, so you’ll pair it with another route for volume and co-benefits.

Carbonfuture is a Freiburg-based platform built entirely around durable carbon removal: biochar, bioenergy with carbon capture and storage (BECCS), direct air capture (DACCS) and mineralisation. Where most providers treat tracking as paperwork, Carbonfuture made it the product. Its MRV+ system (monitoring, reporting and verification) follows each batch of carbon removal from production to final application, feeding third-party verification under methodologies like Puro.earth’s biochar standard.

The buyer list signals where this route has landed: Microsoft, Swiss Re and members of the World Economic Forum’s First Movers Coalition procure through Carbonfuture. Procurement runs from spot purchases to multi-year offtakes, with suppliers on five continents.

Quality reality check. Durable-only is a feature and a constraint. The screening question here is less “is this category credible?” and more “is this specific facility delivering on schedule, and what happens if it doesn’t?” Ask how delivery risk is buffered across suppliers, what replacement rules apply, and how MRV+ data flows into your own reporting stack rather than staying inside theirs.

Where it fits best. If your job is the durable removal ramp and you want batch-level evidence behind every tonne, this is a strong specialist route. For a portfolio that also needs affordable volume, nature-based co-benefits, or strategy support across the whole mix, pair it with a multi-job platform or run it as the engineered flank of a broader portfolio.

Old-generation providers

Old-gen providers also sell portfolios and will package the whole comms kit. Their edge is market memory and breadth. The risk is quality: part of the market’s legacy inventory sits in categories that newer integrity screens treat with caution. The ICVCM’s CCP assessments have excluded several legacy renewable-energy methodologies, and peer-reviewed work has challenged baselines in cookstove and some forestry categories. Unless you set the standard, you’ll often get a mix of decent projects plus cheap, high-scrutiny categories.

You can get strong evidence if you negotiate for it. Make due diligence data a requirement, not a favour. As a preparation, outline your own due diligence framework to not put your reputation at risk. Lead times run from weeks to a couple of months. They can do multi-year deals; it’s just not the default, so you must steer the brief toward offtakes rather than clearing last year’s stock.

Pricing in this cohort is often bundled: platform costs, risk-management fees and markup can sit inside one service charge. Ask directly for the fees and margins they take and how much actually arrives at the project. Demand a breakdown showing project cost, margin, and what portion of your payment reaches project developers. The differences between providers are significant, and the willingness to disclose is itself a quality signal.

South Pole

Global incumbent, scale and experience… plus scars you must manage

At a glance. Best for: contribution at scale and diversified books, with bright lines set up front. Focus: broad global portfolio across reductions and removals. Pricing: catalogue spans the price spectrum; make fees and spreads explicit. Trade-off: breadth includes high-scrutiny segments unless you exclude them, and the Kariba history needs comms readiness.

South Pole brings breadth: a giant portfolio, long developer relationships, and advisory heft. For many enterprises, that scale is the point. But you can’t ignore 2023–24. The Kariba REDD+ controversy triggered a leadership change and a long reputational shadow. South Pole disputes over-crediting claims, yet the episode taught a hard lesson: a black-box curation philosophy plus generous baselines can blow back on buyers. If you go with SP, you need bright lines and auditable documentation up front, or ad hoc due diligence in-house.

Quality reality check. Like other large brokers, South Pole’s catalogue spans the price spectrum. In a market where cheap credit has dominated corporate purchases, “breadth” can quietly include very low-cost, high-risk segments unless you say otherwise. Use market evidence to set floors and filters: the 2024–25 data shows buyers have been shifting toward higher-integrity (and pricier) segments, even as average prices hover around the mid-single digits; watchdog and media scrutiny of low-cost forest credits hasn’t gone away. Your fix is relatively simple: specify allowed methods, vintages, and minimum quality/rating thresholds in the MSA/SOW.

How to use them well. For Contribution at scale or Price-lock, South Pole can assemble diversified books and navigate supply. Make price transparency explicit (fees/spreads, pass-throughs, FX), and hard-code risk management (shortfall replacements, substitution approvals, incident reporting). For a Durable removals ramp, consider SP as a wrapper around a few direct offtakes you control. For Audit-readiness, don’t assume: request sample exports (issuance/retirement proofs, due diligence reports), versioning practices, and data schemas you can plug into CSRD workflows. Done right, you buy their scale without inheriting their risk.

First Climate

DACH-centric, pragmatic packaging, keep your guardrails on

At a glance. Best for: mid-market DACH teams wanting a nearby counterparty and German documentation. Focus: conventional portfolios across reduction and removal types. Pricing: service-led; clarify fees, spreads and re-pricing rules. Trade-off: the default mix needs your quality rules.

First Climate is a steady operator with deep DACH roots. In 2025, they introduced a “Supporting Climate Action” label, positioned as a future-proof alternative to vague neutrality claims. The offer is service-led: German documentation, familiar procurement workflows, and conventional portfolios across reduction and removal types. It’s a comfortable choice for mid-market teams that want a nearby counterparty and tidy comms.

Quality reality check. Comfort doesn’t equal quality by default. As with others in this cohort, catalogues often include lower-priced, higher-risk categories next to better options. The broader literature is unambiguous: corporate offset purchasing has historically concentrated in cheap segments with an elevated risk of non-additionality. If you don’t set the rules, the default mix will set them for you. Write exclusions (e.g., no large-scale grid RE after year X; no forestry baselines that fail test Y), vintage limits, and a minimum share of higher-integrity types (or ratings) into the framework.

How to use them well (jobs + the five real differentiators). For Contribution & comms with German-language assets, First Climate is straightforward. If you need Price-lock, clarify price transparency (fees/spread, re-pricing rules) and risk management (replacement SLAs, who approves substitutions). For Audit-readiness, ask for registry-linked, structured data; don’t settle for certificates alone. If your priority is a Durable removals ramp, you’ll likely pair First Climate with direct developer offtakes or a specialist removals platform.

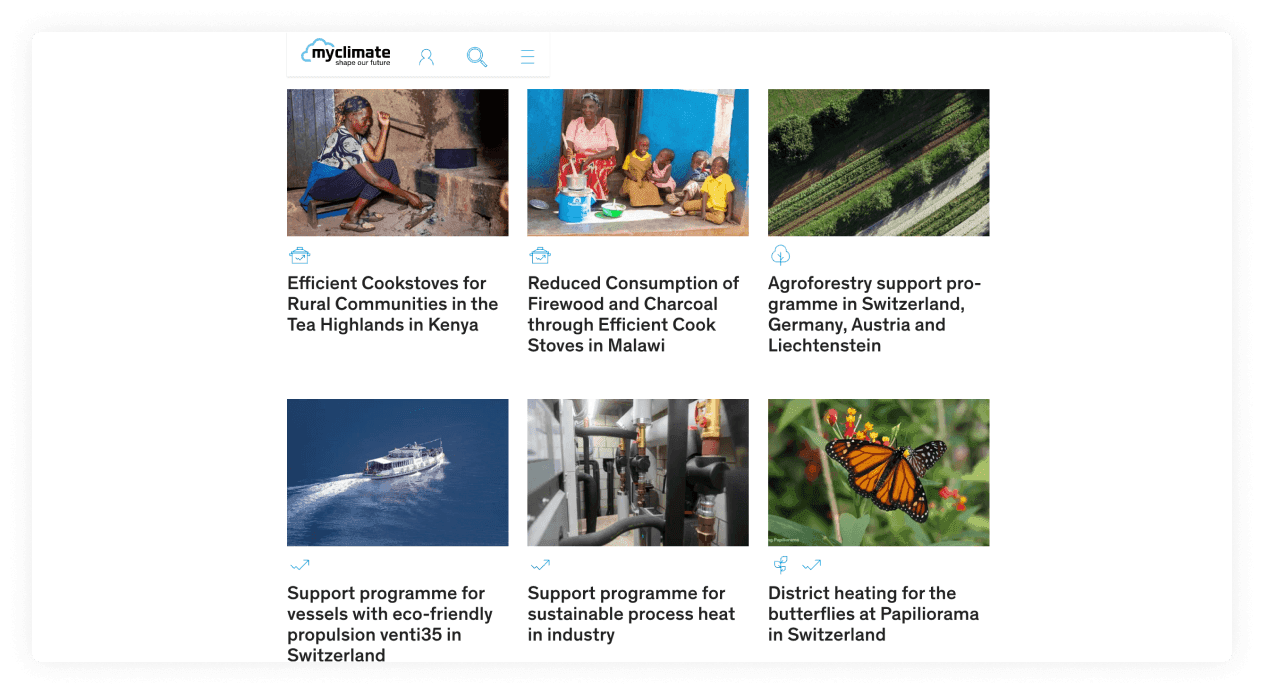

Myclimate

Swiss non-profit, service-led, quality is what you specify

At a glance. Best for: conservative contribution and comms with a Swiss mission-driven counterparty. Focus: broad catalogue, renewables and cookstoves alongside better-screened projects. Pricing: ask for fee and spread disclosure. Trade-off: quality is what you specify, not what arrives by default.

If you want a Swiss, mission-driven counterparty with familiar workflows, Myclimate is the comfortable pick. The company moved early to retire the old “carbon neutral” framing and now offers the myclimate impact label: “Engaged for Impact”. The label’s point is disclosure over slogans: you quantify, reduce, then finance climate projects; Myclimate publishes guidelines for how that contribution is shown and audited. That change wasn’t cosmetic, it tracked the legal climate in Germany and the EU, where courts now demand that any “klimaneutral”-style claim explains inside the claim what it actually means.

Quality reality check. Myclimate’s default catalogue spans price and integrity. If you don’t set rules, you’ll often end up with lower-priced categories (older renewables, cookstoves) next to better-screened projects. That matters because some of those cheap segments are exactly where scrutiny is hottest: a 2024 Nature Sustainability study found pervasive over-crediting across major cookstove methodologies; other peer-reviewed work flagged systemic quality problems across several project types; and ICVCM’s new CCP screens have already excluded swathes of legacy renewable methods. None of that says “never buy”, it says write your exclusions and minimums up front.

How to use Myclimate well. If your job is Contribution now & comms or Audit-readiness with a conservative tone, they fit, provided you contract for evidence: due diligence report, CCP-approved methods, third-party ratings, and export formats you can actually use under CSRD. Be explicit on price transparency (fees/spreads) and on risk management (like-for-like substitutions, shortfall SLAs, who approves changes). If you’re building a Durable removals ramp, you’re better off considering new-gen platforms or direct developer offtakes.

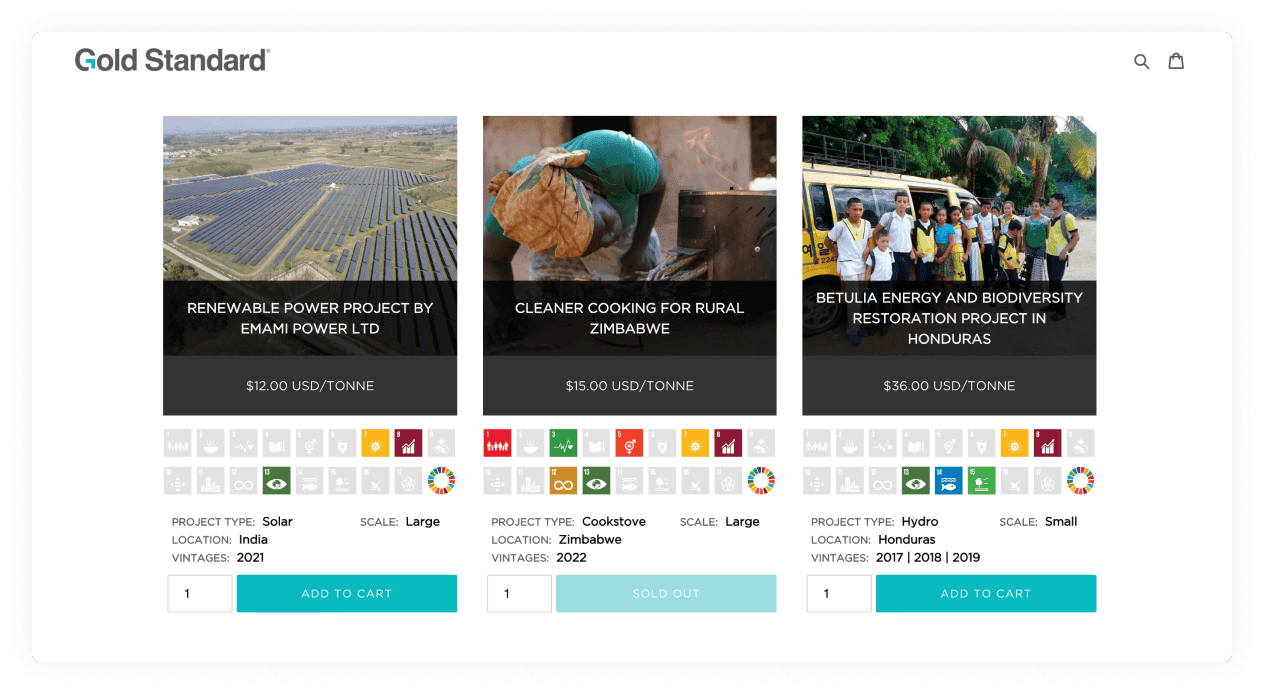

Gold Standard

Standard and registry first, small marketplace; certification is not a substitute for buyer-side due diligence

At a glance. Best for: registry-level traceability when you bring your own due diligence. Focus: standard and registry; small marketplace. Pricing: marketplace retail prices are public. Trade-off: certification tells you a project passed the standard’s requirements, not that it fits your quality bar.

Gold Standard is, first and foremost, a standard and registry. They certify methodologies and run the registry where issuances and retirements live, and publish corporate claims guidance.

Quality reality check. Issuance ≠ quality. A Gold Standard certification tells you a project passed the standard’s requirements; it is not a substitute for your own buyer-side due diligence. Some GS-certified categories have also been in the crosshairs, notably cookstoves, where academic work has documented large over-crediting under certain methodologies (disputed, and now being reworked across the market). Meanwhile, the ICVCM’s CCP process has begun filtering legacy methods across standards (e.g., large tranches of older renewables). If you buy “from the registry,” you still need your own curation philosophy: due diligence, allowed methods, vintages, geographies, and minimum integrity thresholds.

How to use GS well. If your job is Audit-ready CSRD and Contribution now without marketing fireworks, a GS route has registry-level traceability. But build the rest of the system yourself: due diligence on each project, portfolio rules, diversification, and risk controls. Also, align claims language with GS’s guidance and Germany’s advertising standard: the basis of any claim must be clear in the claim itself.

Atmosfair

German non-profit; strict on standard, heavy cookstove exposure, so write the rules

At a glance. Best for: contribution and comms with German documentation and strong co-benefit storytelling. Focus: cookstoves, renewables and energy efficiency, with a Gold Standard CDM emphasis. Pricing: public rates. Trade-off: portfolio leans into the most-scrutinised categories, so integrity rules go in the contract.

Atmosfair is a German NGO with a long track record, especially in aviation. Their projects skew to renewables and energy efficiency, with a stated emphasis on Gold Standard CDM; they also publish the Airline Index, which many comms teams know. If you need a DACH-native counterparty with visible social co-benefits, they’re easy to explain to stakeholders.

Quality reality, plainly. “High standard” doesn’t mean “no risk.” Atmosfair’s portfolio (by design) leans into cookstoves and renewables, exactly the zones under the brightest greenwashing spotlight. The 2024 Nature Sustainability study documented large over-crediting under several cookstove methodologies (again: contested, and being updated across the market); and ICVCM/CCP determinations and other analyses have cast doubt on older renewables and some avoided-deforestation baselines. None of this negates the social benefits of clean cooking; it just means your carbon claims need a tighter bar. If you buy here, specify due diligence requirements, method/version, vintage limits, usage monitoring requirements, and like-for-like replacement rules in the contract.

How to use Atmosfair well. For Contribution now & comms with German documentation and strong co-benefit storytelling, Atmosfair works, if you pre-define integrity rules and demand structured exports for CSRD (not just certificates). If you’re building a Durable removals ramp, you’ll add engineered removals elsewhere and treat Atmosfair as your social-impact flank within a safeguarded portfolio.

Direct from project developers

Here you contract with developers, often for engineered removals or specific nature-based methods you want to back. You gain control and long-term visibility; you also accept more complexity. Expect spending months on project selection, off-takes with milestones and staged payments, and a lot of legal work to get the agreements right, as well as communications with multiple project developers. You will most likely purchase from at least two or three due to the limited supply. When it works, you get a good story. When it doesn’t, delivery risk sits closer to you. This route is strongest on curation philosophy (you pick the exact pathway) and price transparency (you can see the economics), but demands more from operations and risk management.

Climeworks

DAC + permanent underground storage, the flagship for engineered removals

At a glance. Best for: a durable backbone with line of sight from pilot to scale. Focus: direct air capture with permanent mineral storage. Pricing: above €500 per tonne. Trade-off: price and limited volumes, with fewer co-benefits than nature-based projects.

Climeworks removes carbon directly from the air and mineralises it underground. This isn’t avoided emissions; it’s engineered removal with permanent storage. In May 2024, they switched on Mammoth, at the time the world’s largest operating DACS plant. That’s significant for any board that wants a line of sight from pilot to scale with a real asset you can point to.

Procurement here usually means multi-year offtakes that stage volumes and price. Many corporates treat the first deal like building a “muscle” for durable removals, a small but growing tranche each year, with option clauses if costs fall. Climeworks’ buyer set includes high-signal names (e.g., Microsoft, Morgan Stanley), which helps with internal credibility, but you should still negotiate the boring bits: delivery windows, shortfall remedies, verification cadence, and how MRV outputs flow into your reporting stack. The technology is maturing fast; your contract should mature with it.

On evidence and audits, the advantages are clear: a single counterparty, a defined site, and storage that can be independently verified. You’ll want due diligence documentation, registry or equivalent attestation (where registry pathways are still forming for engineered removals), versioned MRV, and exports your CSRD system can ingest without manual stitching.

The two practical frictions are price (>500€ per ton) and supply volume and timing. One additional consideration for your strategy is that engineered removals have significantly fewer co-benefits than nature-based projects, which may impact your DMA. Solve these with a surrounding portfolio: keep Climeworks as your durable backbone, then add high-quality nature- or tech-based credits for the volume, price, and co-benefits.

neustark

Mineralisation in recycled concrete, industrial, permanent, European

At a glance. Best for: tangible, European, permanent storage in recycled concrete. Focus: mineralisation at biogenic point sources, site-specific. Pricing: above €200 per tonne. Trade-off: scale is tied to recycling infrastructure and individual sites.

Neustark is a Swiss developer that locks carbon into demolition concrete aggregate by mineralisation. Think of it as turning waste streams into permanent carbon stores. The feedstock CO₂ is captured at nearby biogenic point sources (e.g., biogas plants), liquefied, and injected into recycled concrete granulate; carbonates form and the CO₂ is durably stored within the material. It’s an elegant industrial route with European siting, which many DACH boards like because it’s tangible and local.

Neustark is built for multi-year offtakes. Microsoft signed 27,600 t over six years, and in August 2025, SWISS became its first airline partner under a contract running to 2030. Expect prices above €200 per tonne and limited volumes. Most buyers balance this with lower-cost, high-quality credits such as regenerative agriculture or more affordable biochar. You can negotiate several deals yourself, or use a new-gen platform to handle sourcing, contracting, and delivery risk.

Audits are straightforward because storage sits in physical assets at named sites. You get a clear MRV story. Ask for year-by-year delivery targets and independent verification. The trade-offs are scale and geography. Growth depends on recycling infrastructure, and projects are site-specific. Solve that with a small basket: two or three mineralisation sites plus one or two other projects, so your ramp is not tied to a single permit or plant.

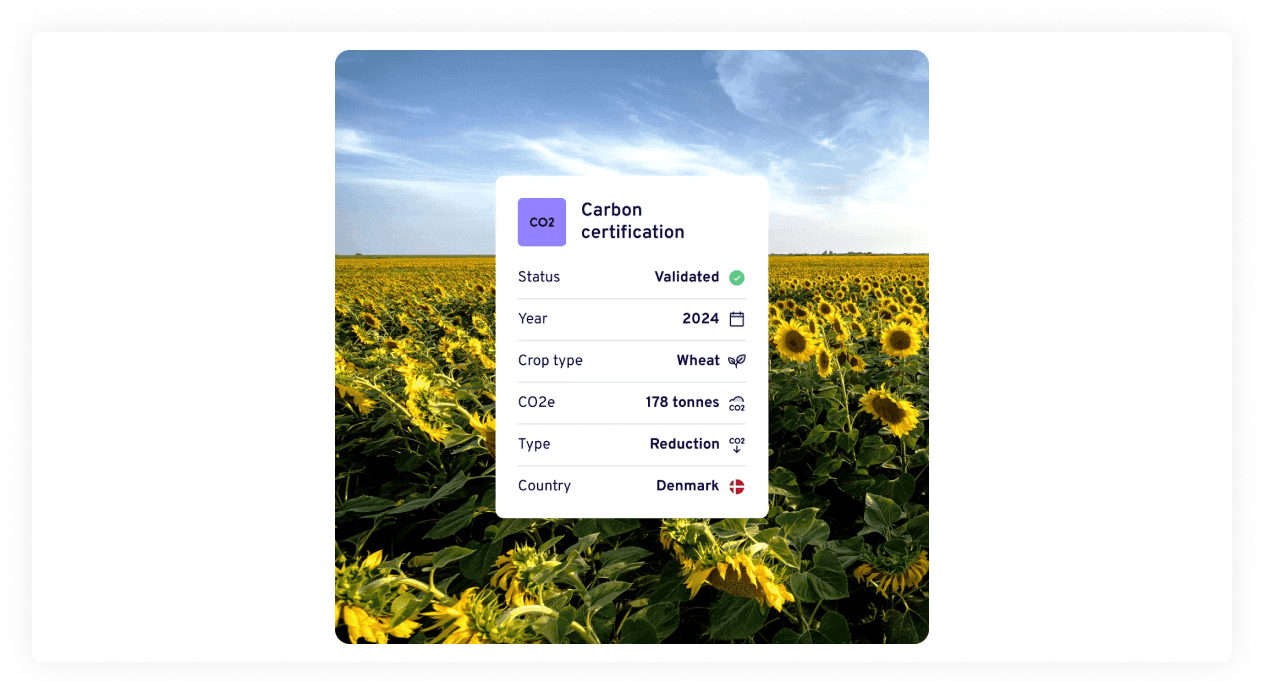

Agreena

Soil carbon across European cropland, large-scale, active debate, write the rules

At a glance. Best for: European soil carbon at scale, for contribution and portfolio learning. Focus: regenerative cropland under Verra VM0042. Pricing: forward pre-orders or spot from issued vintages. Trade-off: active methodology debate; contract explicitly for monitoring and reversals.

Agreena runs one of Europe’s largest soil-carbon programmes, paying farmers to adopt regenerative practices and issuing credits under Verra’s VCS. The project secured Verra registration in early 2025 and, crucially, has now achieved verification and issuance, with press reporting ~2.3 million VCUs under VM0042 v2.0. For DACH corporates, the draw is obvious: European geography, large scale and improvement on working farms.

Procurement feels like two tracks. One is forward: pre-orders and multi-year engagement to build volume and price visibility. The other is spot from issued vintages once verification lands. Either way, you need to interrogate the programme design: how additionality is established per field, how leakage and double counting are prevented, what permanence obligations farmers carry, and how reversals are handled (buffers, clawbacks, or replacement). Agreena has launched a “Carbon Credit Confidence” initiative and publishes Verra-related updates, good signs, but your contract still needs explicit rules on data access, monitoring frequency, and what happens when practices change.

Quality is the conversation here. Soil carbon has clear co-benefits and strong policy momentum in Europe, yet methodology debate is active: academics and practitioners continue to challenge model-heavy baselining and permanence claims; regulators are building stricter integrity screens (e.g., ICVCM/CCP, coming EU CRCF). Treat that as a design constraint rather than a red flag. For Contribution now or Portfolio learning, European soil credits can be useful if you diversify and set floors: field-level monitoring, conservative baselines, reversal provisions, and registry-linked evidence. For Price-lock or Durable ramp, keep soil as a portfolio component and anchor permanence with engineered routes. That balance lets you benefit from scale without inheriting the whole debate.

Klim

Regenerative agriculture; Germany-first, reductions and removals

At a glance. Best for: German regional credits with farm-level stories. Focus: regenerative agriculture, removal and reduction credits. Pricing: published €50 per tonne. Trade-off: pair with durable removals, and align claims with what is actually issued (as of June 2026, the Verra project is in development).

Klim sells German “regional” credits at a public price of €50 per tonne. It issues two types: removal credits from soil carbon build-up and reduction credits from lower farm emissions. This is local, farm-level procurement that suits DACH brands and auditors.

Procurement is simple. You can buy spot from issued vintages or contract forward against farmer cohorts. Data flows from Klim’s platform. Ex-post verification happens each spring, so delivery and reporting follow the farm year. Site visits and local storytelling are part of the offer.

ISO 14064-2 validation with TÜV Rheinland and annual TÜV verification indicate a structured quality posture. ISO validation is a process check: combine it with registry data, independent ratings and MRV data for a fuller quality picture. As of June 2026, Klim lists its Verra VM0042 project as “in development” rather than issuing VCUs. Do due diligence on contracting and align claims to what you are actually buying.

Use Klim as a component, not the whole plan. Diversify into durable removals to follow the Oxford Principles and to meet SBTi’s rule to neutralise residuals with permanent removals at net zero (Oxford 2024 update; SBTi Net-Zero Standard). Either add direct offtakes with other developers, or use a specialist platform that assembles removals and manages delivery risk for you. On price, platforms that publish fees and live pricing often land close to direct once you include contracting and monitoring overhead; make them prove it with a line-item fee breakdown, developer share, and project receipts.

Common pitfalls when buying carbon credits

Five mistakes come up again and again in procurement reviews:

- Buying on price alone. The 2023 average of $6.53/t (Ecosystem Marketplace) hides the fact that serious buyers concentrate in pricier, higher-integrity segments. A cheap tonne is usually cheap for a reason, and German courts now expect any claim built on it to explain itself inside the claim.

- Treating certification as quality. A registry stamp is the floor, not the ceiling. Peer-reviewed work has documented over-crediting in major cookstove methodologies, and the ICVCM’s CCP screens have excluded large tranches of legacy renewables. Add your own due diligence layer or buy from someone who shows you theirs.

- Letting the default mix decide. If you don’t write exclusions, vintage limits and minimum integrity thresholds into the MSA/SOW, the provider’s inventory writes them for you.

- Ignoring contract mechanics. Delivery windows, shortfall replacement, substitution approvals, incident reporting. Soft contracts are silent until something goes wrong.

- Mixing vendors whose data doesn’t align. Under CSRD assurance, a portfolio scattered across incompatible formats is a finding waiting to happen. Our DAX40 analysis found 45% of disclosed credits untraceable to a specific project.

How we chose: this guide is written by Senken and includes our own platform. Selection and grouping reflect our editorial judgment, based on public information as of June 2026. Factual claims are linked to sources; where we state opinions, they are ours.