.svg)

Explaining the difference between Carbon Removal and Carbon Avoidance

Most corporate buyers we talk to in 2026 arrive with the same starting assumption: removal credits are the credible ones, and avoidance credits are a legacy problem to back away from. That position is partly fair. The 2024 Nature study found that 87% of credits bought by the world's largest companies carried a high risk of delivering no real emissions reduction, and most of those were avoidance credits. The market took that finding and rotated hard into removal as the safe answer.

It's true that the highest-quality permanent removals (DAC, biochar, mineralisation) sit at the top end of the quality range, and that reputation is earned. But removal as a category is not uniformly high-quality, and avoidance is not uniformly low-quality. The Calyx Global 2026 ratings show the spread inside both categories. Avoidance occupies the very top ratings (the only credits earning A+ and A are avoidance credits), while removals are more heavily represented in the lower bands. There is a wide quality range in both. The quality story is methodology-specific and project-specific, not category-specific, and what looks like a category problem in the market is usually a screening problem inside a category.

The reason removal trades at a premium is supply, not quality. There simply isn't much of it: the methodologies are newer, more capital-intensive, and slower to issue. The 2026 State of Quality and Pricing in the VCM report shows this clearly: at every GHG rating tier, removal projects price meaningfully higher than avoidance projects with the same quality grade.

So the question for a corporate buyer in 2026 isn't really "do I pick removal or avoidance." It's: what are the two categories actually doing, what mix should sit in my portfolio given my net zero target year, and how do I screen out the projects within each category that will create a reputational problem two years from now?

The difference

A carbon avoidance credit represents emissions that did not happen. A carbon removal credit represents emissions that have been taken out of the atmosphere. Both are measured in tonnes of CO₂ equivalent, but the underlying climate work is fundamentally different.

Carbon avoidance covers projects that prevent emissions from happening in the first place. The most common types are forest protection (paying landowners and communities not to clear standing forest, sometimes called REDD+), methane capture from landfills or agriculture, and renewable energy projects that displace fossil generation. A retired avoidance credit represents a tonne of CO₂ that didn't enter the atmosphere because that project was financed.

Carbon removal covers projects that pull CO₂ that's already in the atmosphere back out and store it. The storage can be biological (afforestation, reforestation, soil carbon), it can be a hybrid (biochar, which locks plant carbon into a stable form in soil for 100 to 1,000 years), or it can be geological (Direct Air Capture with underground mineral storage, which holds carbon for tens of thousands of years).

Both categories matter, and the IPCC has been explicit about that since AR6: the world needs deep emissions reductions plus 6–10 gigatonnes of carbon dioxide removal per year by 2050. The voluntary market currently delivers a tiny fraction of that, well under 0.01% of the 2050 requirement.

Three questions to ask before you choose

1. Will this credit count toward our net zero claim?

Under SBTi's Corporate Net-Zero Standard v2, only removal credits can be used to neutralise residual emissions in a net zero claim. After 2035 this becomes the rule across most credible frameworks. Avoidance credits don't count toward neutralisation, but they remain valid for the near-term mitigation work that runs in parallel with your decarbonisation roadmap.

SBTi v2 also introduces the concept of Ongoing Emissions Responsibility (OER), which formalises something most corporate buyers were already starting to sense from supply conversations: you can't wait until your net zero year to start buying removal. Removal supply will be tighter and more expensive in 2045 than it is today, and the procurement curve needs to start now.

2. What's the right mix of removal and avoidance for our portfolio?

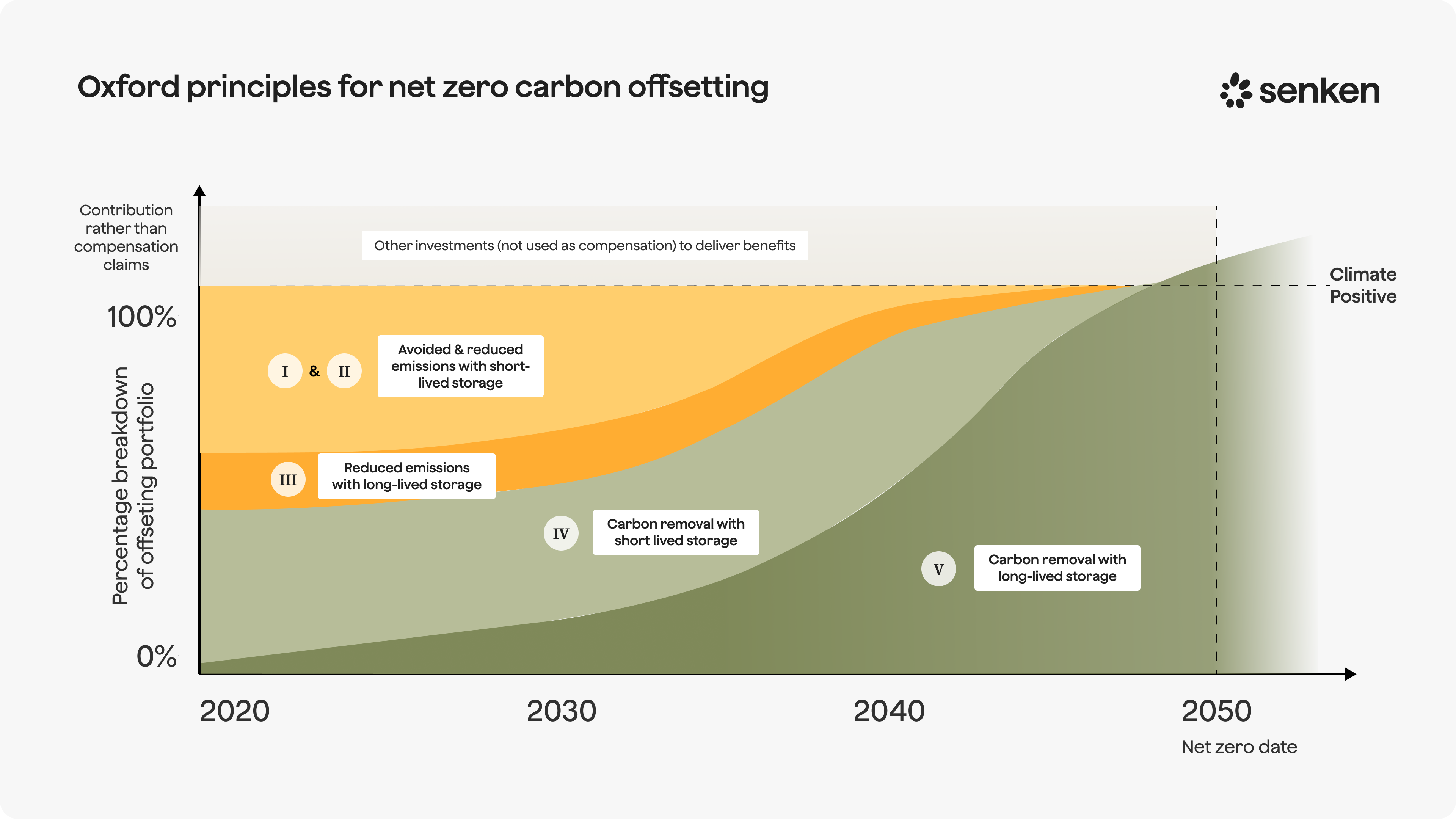

The Oxford Principles for Net-Zero Aligned Carbon Offsetting set out the canonical trajectory. Principle 2 says corporates should progressively shift their portfolio away from avoidance and toward removal, reaching 100% removal by their net zero year. Principle 3 asks for a parallel shift inside the removal allocation itself: from short-lived storage like forests (which can be lost to fire, pest, or harvest) toward long-lived storage in biochar, geology, or mineralisation, with permanence measured in centuries or millennia. SBTi v2 follows the same logic through OER.

3. How do we make sure a credit doesn't blow up on us?

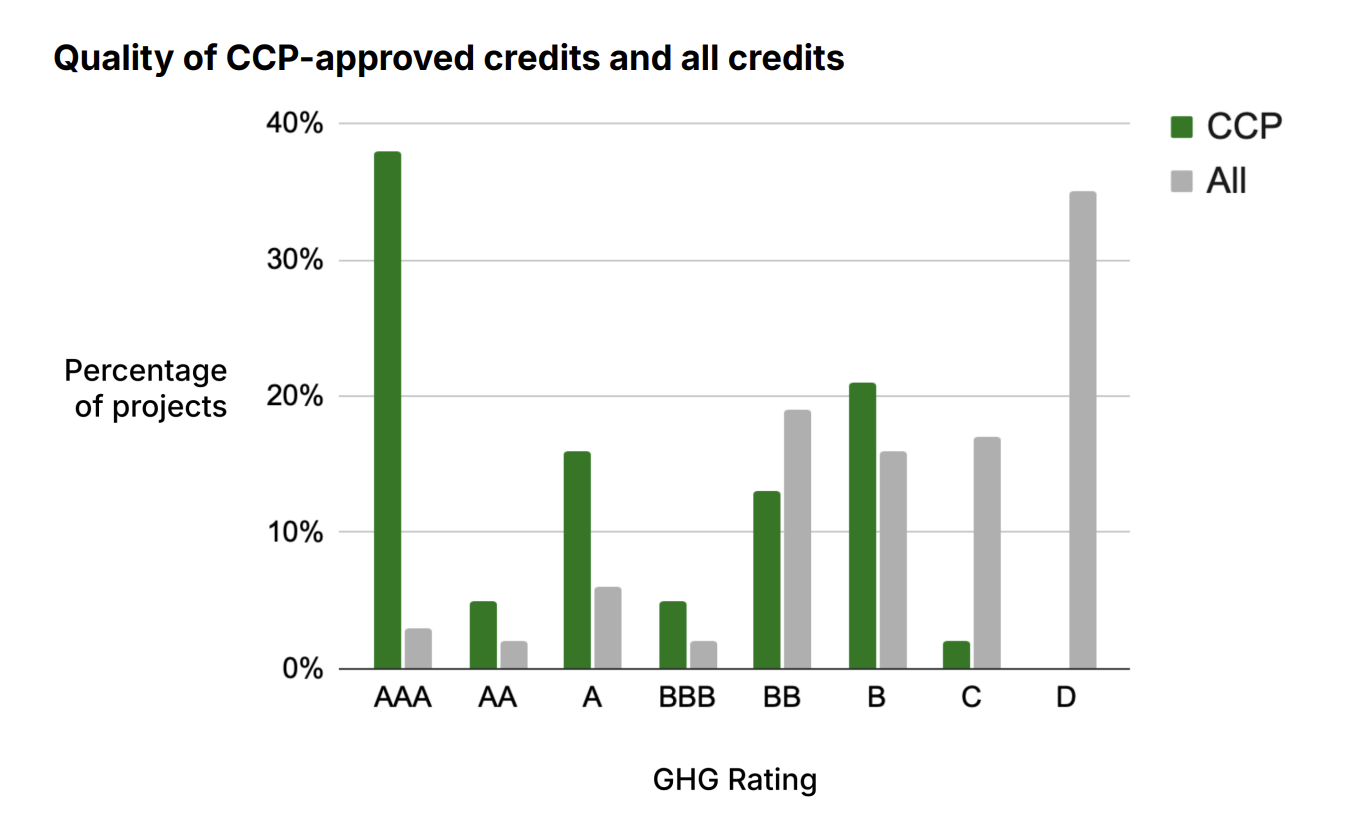

Quality is much less about which category a credit sits in than about how the specific project is screened. The single most useful filter on the market is whether a credit is approved under the Core Carbon Principles (CCP). The Integrity Council for the Voluntary Carbon Market (ICVCM) launched the CCP framework in 2023 to set one quality threshold across the patchwork of older standards (Verra, Gold Standard, ACR, CAR). The data shows it works: CCP-approved credits cluster in the higher quality bands, while the broader uncategorised universe is concentrated at the bottom.

A question we get every week: is REDD+ dead? No, but the version of REDD+ that drove the 2024 controversy effectively is. Those were credits issued under VM0007 and similar pre-revision methodologies, where baselines were inflated and additionality was hard to verify. The newer CCP-aligned REDD+ methodologies produce credits that look very different, but the issued supply is small and most of what's available in the spot market is still old vintage. A 2026 portfolio that wants forest protection in it needs to be very selective about methodology and vintage, or it inherits the original problem.

The three filters that do most of the work in our screening process:

- CCP-approved methodology. If a credit isn't CCP-approved, there should be a defensible reason to buy it anyway.

- Recent vintage. Pre-2020 vintages carry the most reputational risk. The methodology that issued them has often since been retired, revised, or downgraded.

- Project-level defensibility. It combines external ratings, press and in later stages proprietary due diligence.

That screen is the reason we end up rejecting around 95% of the projects that come across our desk.

A look at the common methodologies

Closing

The corporate buyers who are getting this right in 2026 have stopped treating removal and avoidance as competing options to pick between. They build portfolios that contain both, weighted to fit their specific net zero timeline, and they screen every credit through CCP approval, vintage, and a project-by-project defensibility test before it goes in. That's not the most exciting answer, but it's the answer that survives a CSRD audit and a sceptical board.

Frequently Asked Questions

What is the difference between carbon removal and carbon avoidance?

A carbon avoidance credit represents emissions that did not happen, for example through forest protection (REDD+), methane capture from a landfill, or renewable energy that displaces fossil generation. A carbon removal credit represents emissions that have already been taken out of the atmosphere and stored, for example through afforestation, biochar, or Direct Air Capture with geological storage. Both are measured in tonnes of CO₂ equivalent, but the climate work is fundamentally different: avoidance prevents new emissions, removal addresses emissions that already exist.

Can carbon avoidance credits count toward a corporate net zero claim?

Under SBTi's Corporate Net-Zero Standard v2, only carbon removal credits can be used to neutralise residual emissions in a net zero claim. After 2035 this becomes the rule across most credible frameworks. Avoidance credits do not count toward neutralisation, but they remain valid for the near-term mitigation work that runs in parallel with a company's decarbonisation roadmap.

What is the right mix of carbon removal and avoidance in a corporate carbon credit portfolio?

The Oxford Principles for Net-Zero Aligned Carbon Offsetting set the canonical trajectory: corporates should progressively shift their portfolio away from avoidance and toward removal, reaching 100% removal by their net zero year. The closer a company's net zero target year, the more removal needs to be in its portfolio today. A 2030 target needs removal as a substantial share of current purchases, with multi-year offtakes signed for the durable portion (biochar, DACCS, mineralisation). A 2050 target has more runway, but a portfolio still close to 100% avoidance heading into 2035 will be caught by the SBTi v2 threshold.

Is REDD+ dead as a category for corporate carbon credit buyers?

No, but the version of REDD+ that drove the 2024 Nature study controversy effectively is. Those credits were issued under VM0007 and similar pre-revision methodologies, with inflated baselines and weak additionality. Newer CCP-aligned REDD+ methodologies produce credits that look very different, but issued supply is small and most of what is available in the spot market is still old vintage. A 2026 portfolio that wants forest protection in it needs to be very selective about methodology and vintage, or it inherits the original problem.

CARBON OUTLOOK

Subscribe to a biweekly newsletter from Adrian Wons, breaking down regulations, carbon markets, and corporate strategies.