How to build a corporate carbon credit strategy: a 14-step framework

By Adrian Wons, founder and CEO of Senken.

If I had to build a corporate carbon credit strategy from scratch today, I would do it completely differently from how most companies still do it.

I can say that because I have watched dozens of large European corporates get this wrong. I have seen companies spend seven figures on credits that turned out to be useless for their Science Based Targets initiative (SBTi) submission, because nobody checked the methodology against the rules first. I have watched a sustainability team get talked into a public "carbon neutral" claim by marketing, then watched legal quietly strip that same claim eighteen months later once the EU's green-claims rules came into view.

The pattern is almost always the same. Companies start shopping for credits before they have done the foundational work. They pick a project that looks good, retire some tonnes, write a press release, and a year or two later it unravels.

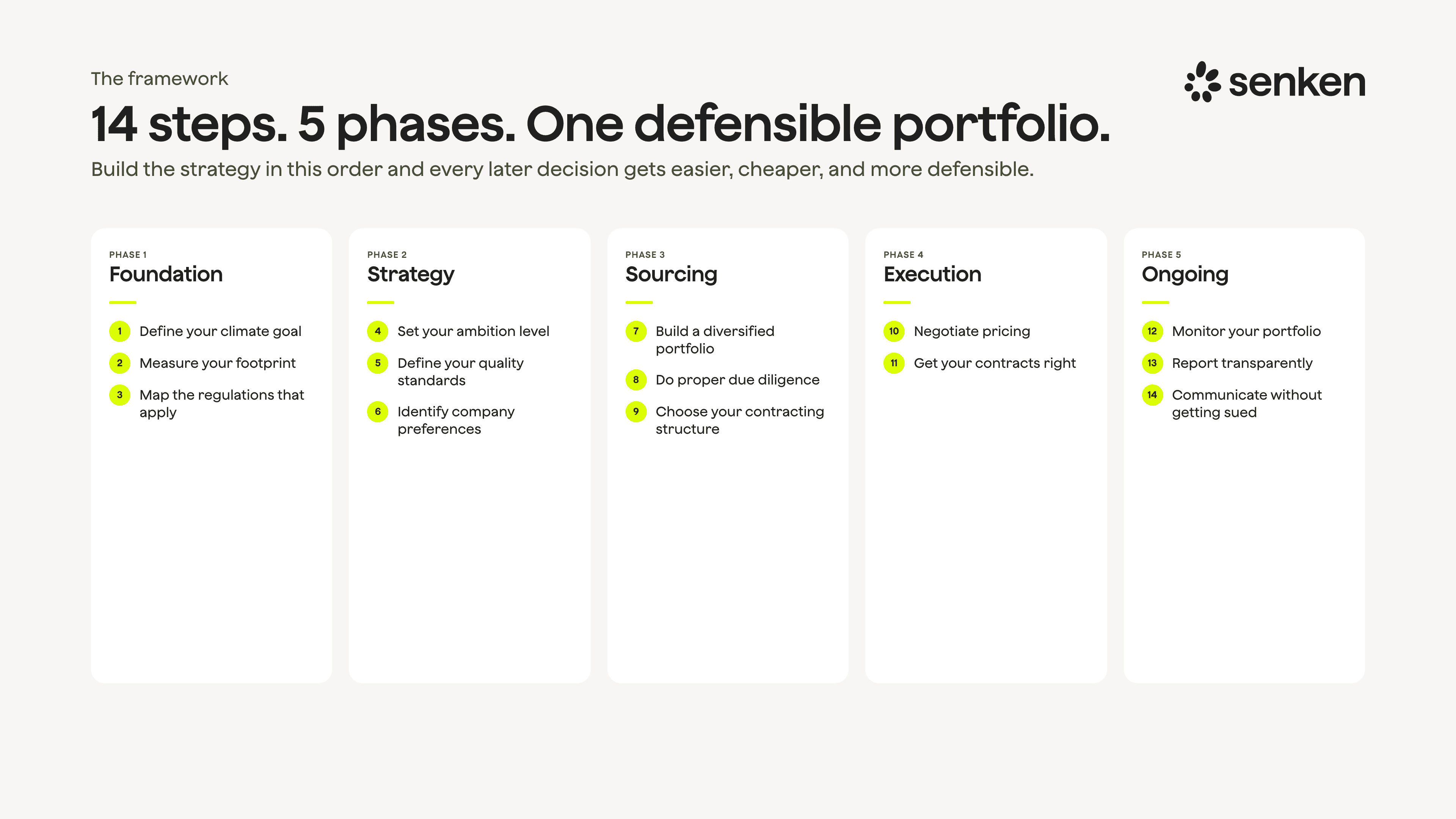

So here is the framework I actually use, the one we take clients through. Fourteen steps, five phases, and the order is what most people get wrong. Get the early steps right and the expensive, hard-to-reverse decisions later on become a lot simpler. Start at step seven instead, because a supplier turned up with a project that looks perfect, and you will be unwinding it a year or two from now.

The framework: 14 steps across five phases. Source: Senken.

Phase 1: Foundation

Step 1: Define your climate goal

Before you buy anything, you need a goal. Without one, procurement, finance, and your board have nothing to approve a budget against.

There are only a handful of commitment types worth understanding, and each one changes what kind of credit you can buy and what job it does. The most common is an SBTi target. If you have one, your credit choices are constrained, and they are about to be constrained further: the SBTi Corporate Net-Zero Standard v2, currently in consultation, introduces explicit carbon-removal targets and a concept called Ongoing Emissions Responsibility (OER), the framework that replaces what used to be called Beyond Value Chain Mitigation. An SBTi target also leads, eventually, to a net zero target, and that matters: once you reach net zero you will have residual emissions you cannot eliminate, and you can only neutralise those with carbon removal, not avoidance.

Then there are the other types we see: carbon neutrality for your own operations (scope 1 and 2), longer-term climate-neutral targets, or a simpler climate-contribution commitment, for example financing a set volume of climate projects each year based on an internal carbon price.

Whatever you pick, lock down three things before you move on: the timeline, the scope boundaries (scope 1, 2, and whether scope 3 is included), and the exact public claim language, signed off by legal, the CFO, and the CEO.

One more thing, and I have seen this catch companies out more than once. Before you set any new goal, audit what your company has already said in public. Sustainability reports, press releases, customer-facing landing pages, product packaging, investor decks. A surprising number of companies discover a "climate neutral" claim sitting in a 2021 press release that nobody remembers signing off. That kind of legacy claim is a liability now, and it is worth revisiting before it becomes someone else's lawsuit.

And do not make the public commitment before the footprint is measured. If you do, you will spend the next year reverse-engineering the whole strategy to fit a number someone picked for a headline.

Step 2: Measure your footprint

I am not going to walk through measurement here, because it is not what we do and it deserves its own guide, especially now that scope 3 is getting genuinely complicated. I am only flagging it because it sits in the middle of the foundation for a reason. Your footprint is the denominator for every later decision: how many tonnes you need, what share is residual, what you can credibly claim. Get it measured properly, ideally with third-party assurance, before you treat any number as fixed.

Step 3: Map the regulations that apply to you

Before you go anywhere near the market, build a one-page matrix of every framework you report under, plus the goal you set yourself in step 1, and what each one demands of your carbon credit programme. You will reference this matrix at every decision point afterwards.

The ones to check: SBTi, the Corporate Sustainability Reporting Directive (CSRD) and its disclosure standards, the EU's Empowering Consumers for the Green Transition Directive (more on that in step 14), any carbon-tax regime you fall under, the EU Emissions Trading System (EU ETS), CORSIA (the UN's offsetting scheme for international aviation) if you fly, and the disclosure schemes like CDP and EcoVadis. The reason this is worth a dedicated step: a credit can be perfectly acceptable for a CSRD disclosure and completely useless for anything inside SBTi. If you do not know which rules bind you, you cannot know which credits are eligible.

A question I get constantly here: "should we buy Article 6 credits with corresponding adjustments?" For almost every corporate, my answer is no. There is no demand source that requires them yet, the supply is thin, and you usually pay a premium for a feature you will not use. The same goes for the EU's forthcoming Carbon Removal Certification Framework (CRCF): worth tracking, but its first real demand case is likely the EU ETS around 2031, so do not reshape your 2026 portfolio around it.

Phase 2: Strategy

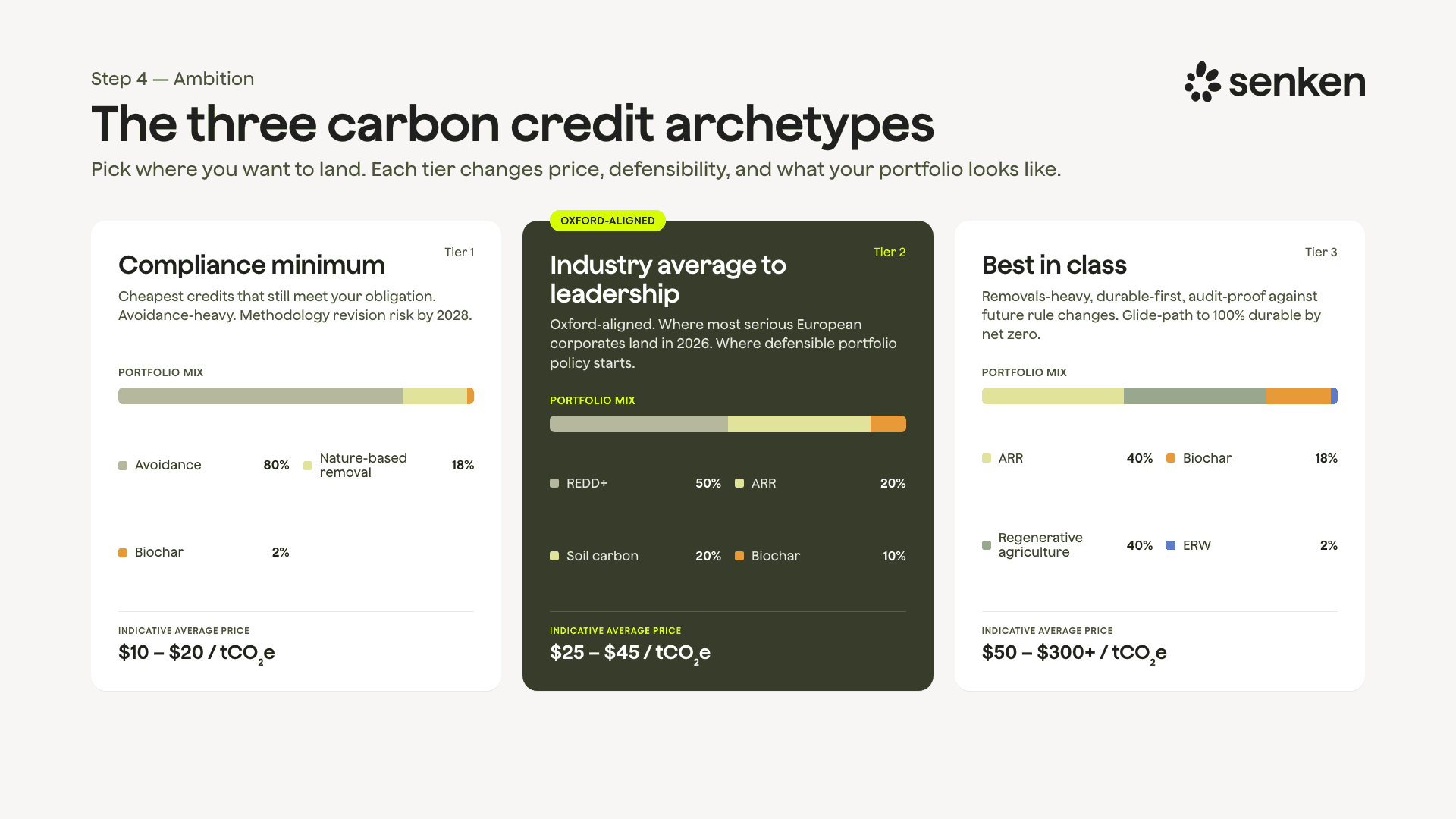

Step 4: Set your ambition level

Once the goal is set, the next question is how ambitious you actually want to be. This is not only about price, it is about how defensible your portfolio looks in a few years. I think in three archetypes.

The three ambition archetypes. Source: Senken.

At the bottom is the compliance minimum: the cheapest credit that still meets your obligation. In practice that means mostly avoidance credits, often older vintages, at roughly $10 to $20 per tonne. It is cheaper on paper, but it carries a high probability that the methodology gets revised before your reporting cycle even closes. If your portfolio looks like this in 2026, you are buying yourself a write-down in 2028.

The middle archetype is industry average to leadership: a typical Oxford-aligned portfolio (I will explain what that means in step 5), priced somewhere around $25 to $45 per tonne. This is where most serious European corporates landed in 2026, and where a genuinely defensible portfolio policy starts.

At the top is best in class: removal-heavy, durable, built to hold up against future rule changes, already usable toward a net zero claim. These portfolios include forward commitments to engineered removals, sometimes supply-chain projects in the company's own value chain, and a written path to 100% durable storage by net zero.

To pick the right level, benchmark against five peers in your sector. Pull their public sustainability reports, CDP responses, and disclosures, and look at their target, the volumes they buy and retire, the project types, sometimes even a price, and their public claims. It takes a couple of days and gives you a real market anchor. If the sector average is 10% removals and you commit to 40%, you can credibly call that leadership.

One warning before you move on. The biggest mistake here is overcommitting in public and having to walk it back. I would rather undercommit and beat the target than put a number in a press release that legal makes me retract two years later.

Step 5: Define your quality standards

This step used to be hard. It has become much easier over the last few years, because there are now two standards you can anchor to: the Oxford Offsetting Principles and the ICVCM Core Carbon Principles. Both are worth understanding deeply, because they are the lens that auditors, NGOs, and journalists will use to judge your portfolio in five years.

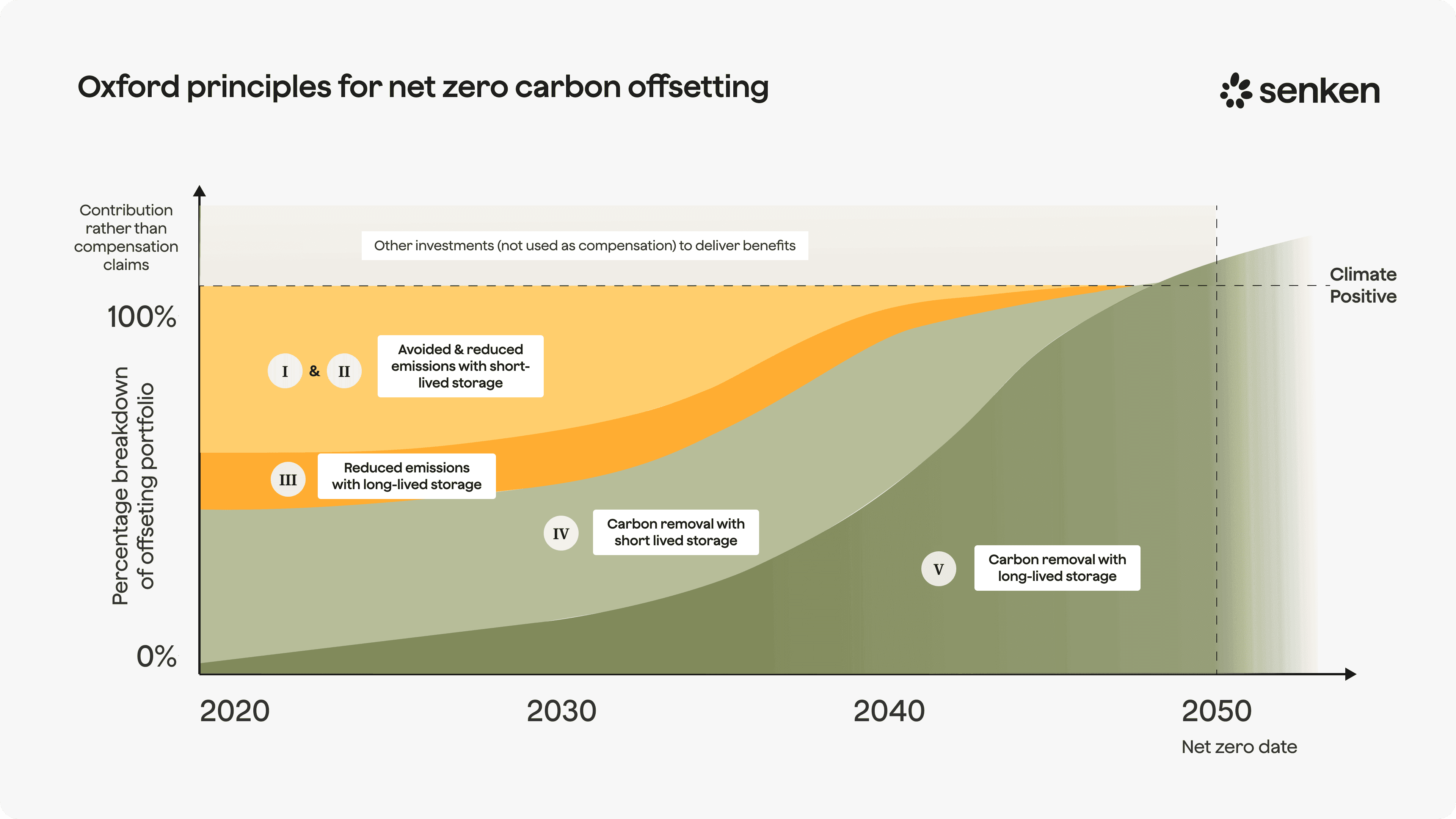

Start with the Oxford Principles for Net-Zero Aligned Carbon Offsetting, the most influential integrity framework in the voluntary market. They were first published in 2020 by researchers at the University of Oxford and had a major revision in 2024. Almost every credible portfolio policy in Europe now references them. The 2024 version rests on four principles, and two of them shape portfolio design more than anything else.

Principle one is cut emissions first. Offsetting is not a substitute for reduction, and credits should only ever address the residual emissions you cannot eliminate. The practical test: can you point to year-on-year absolute reductions in scope 1 and 2, plus a credible scope 3 plan, before you claim any retirement? If your strategy is "buy credits and keep operating," you have failed principle one and the whole portfolio is exposed.

Principle two is the one most people mean when they say "Oxford-aligned." It says you should shift toward high-durability removals over time. Roughly: maybe 20% removals in 2025, around 50% by 2030, approaching 100% by your net zero year. And durability matters enormously. A tonne stored in a forest for 50 years is not equivalent to a tonne mineralised underground for 10,000 years.

The Oxford glide path: the shift from avoidance toward durable removal over time. Source: Oxford Offsetting Principles (2024), via Senken.

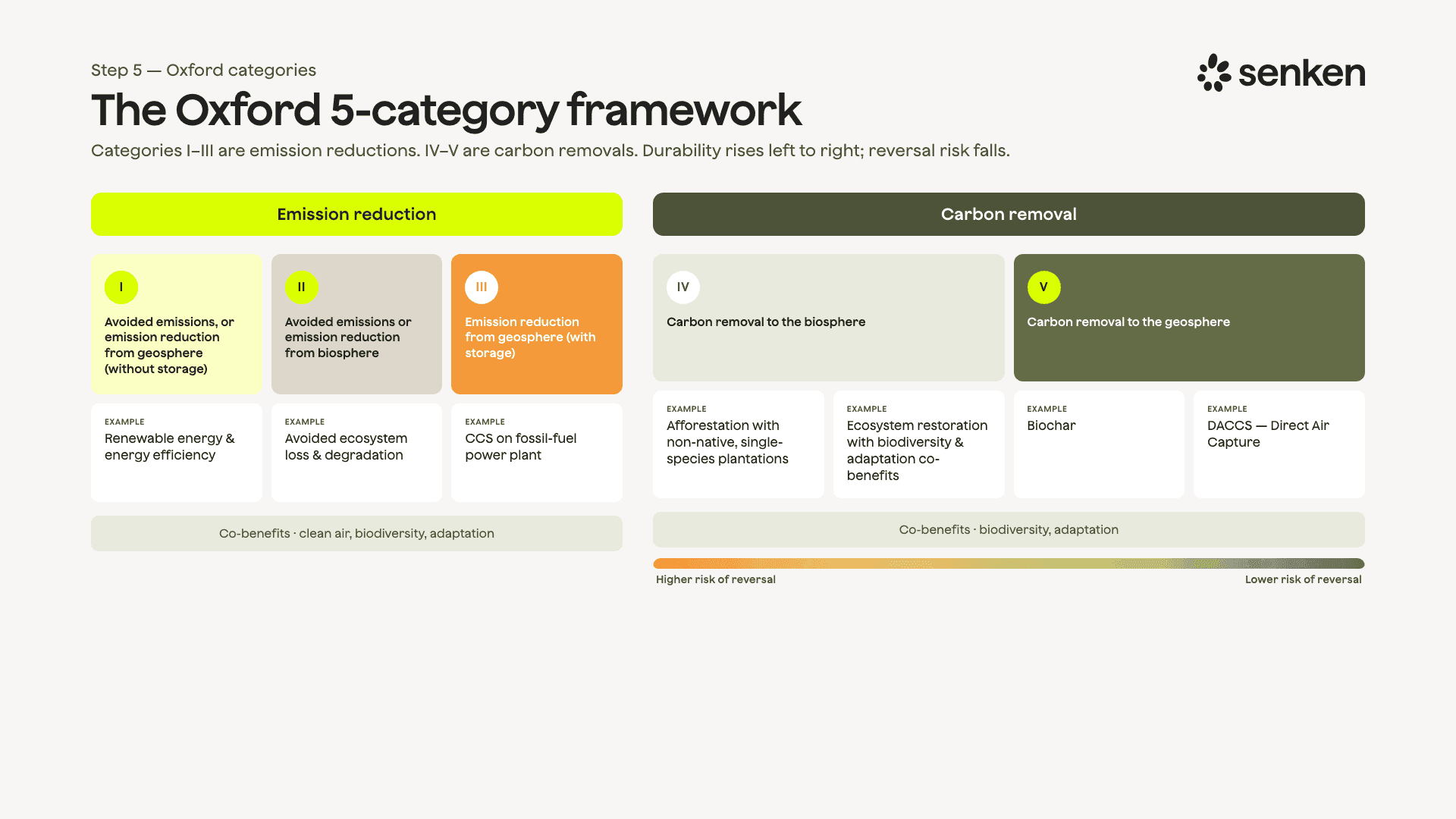

To make that concrete, Oxford sorts projects into five categories. Categories one to three are emission reductions, four and five are carbon removals, and reversal risk falls as you move right.

The Oxford five-category framework. Source: Oxford Offsetting Principles (2024), via Senken.

A practically Oxford-aligned portfolio in 2026 has four things on paper: a written reduction-first commitment, a published glide path with year-by-year removal targets, hard quality filters on every credit, and at least one forward or offtake agreement with a durable removal project. If your portfolio is missing any of those, you are not fully aligned, whatever your sustainability report says.

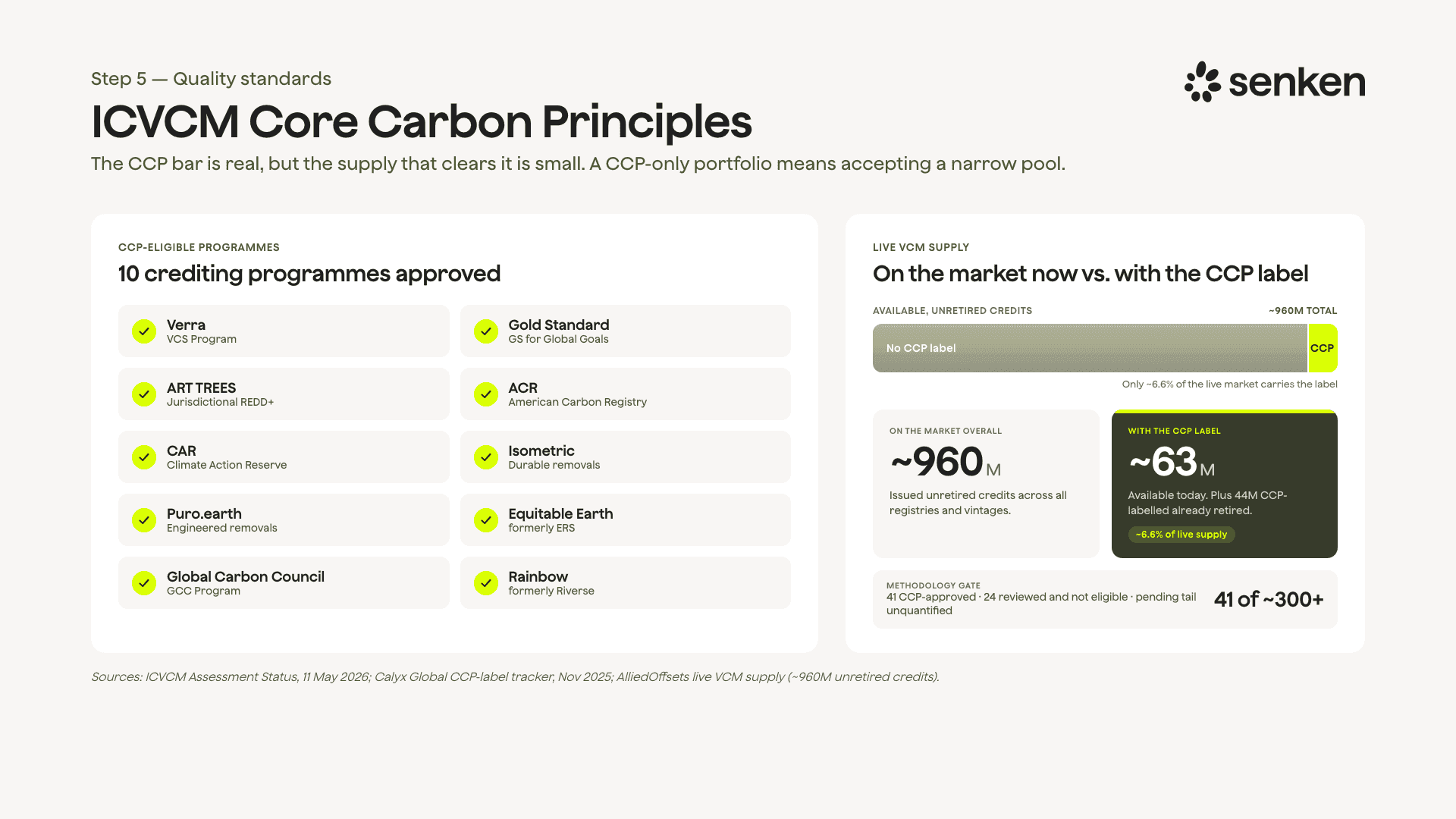

The second standard is the ICVCM Core Carbon Principles (CCP). The Integrity Council for the Voluntary Carbon Market, an independent governance body launched in 2021, published these principles in 2023, and they are the closest thing the market has to a global integrity standard. There is one important architectural point: the CCP label applies at the programme and methodology level, not the individual project level. When a specific methodology under a registry is assessed and approved as CCP-compliant, all credits issued under it carry the label. That makes the CCP a useful procurement filter, because you can apply it at the contract stage rather than credit by credit.

The Core Carbon Principles, and how little of the live market currently carries the label. Source: ICVCM, Calyx Global, via Senken.

There are ten Core Carbon Principles, grouped under governance, emissions impact, and sustainable development. A CCP-approved programme has cleared a meaningful integrity bar across all of them. CCP-approved is not the same as perfect, but it is a strong positive filter that buyers and auditors increasingly recognise. My standard rule for a procurement policy: CCP-approved is the default, and any non-CCP credit needs a documented exception. The caveat in 2026 is that not every methodology has been assessed yet, so for now I want the registry and programme to be CCP-approved and the methodology to at least not have been rejected. Over the next two or three years that transition will close.

If you remember one thing from this step: Oxford tells you what shape your portfolio should be, and the ICVCM tells you what each credit inside it should look like. You need both.

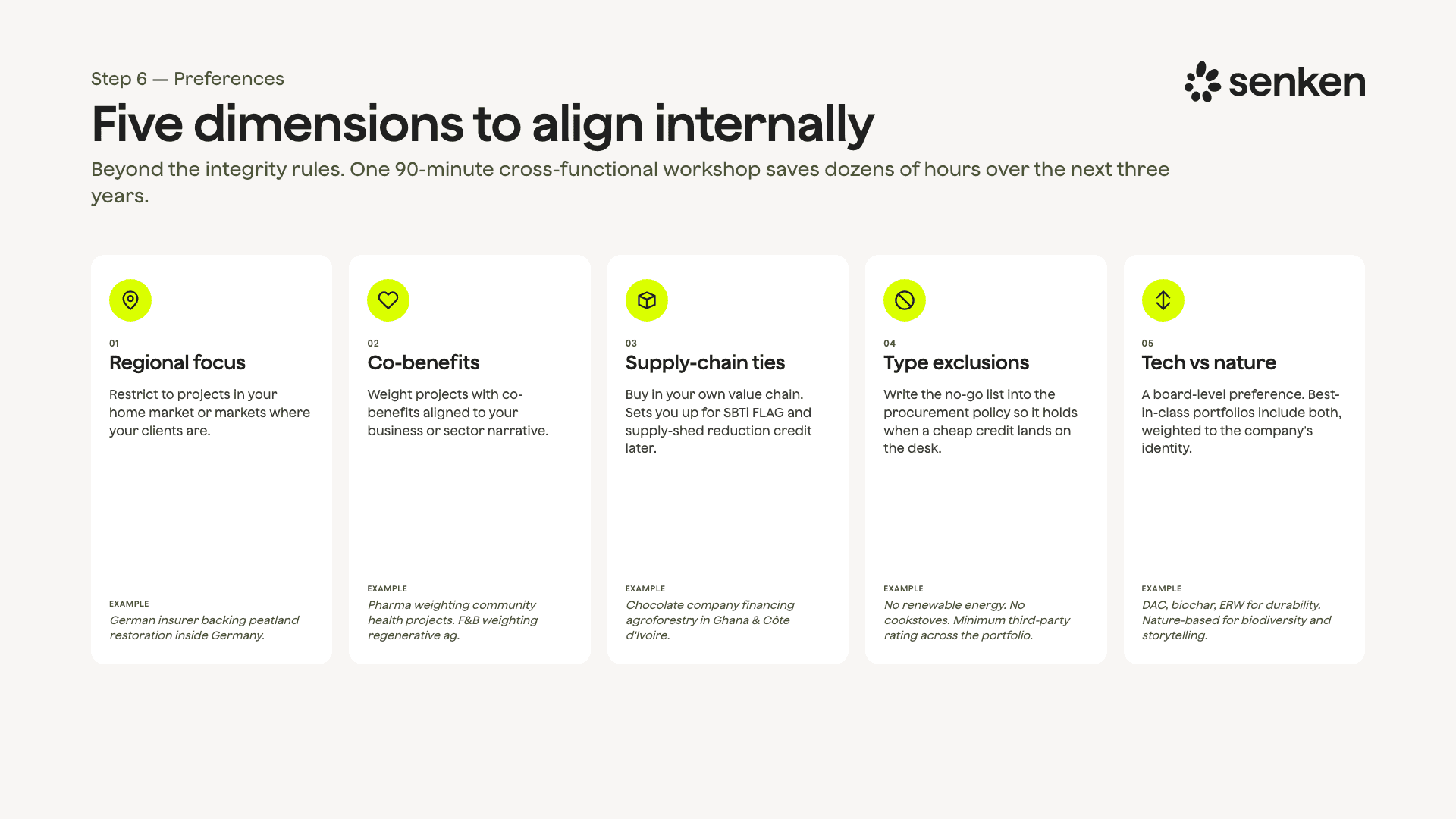

Step 6: Identify your company preferences

Integrity rules and company preferences are two different things, and you should run an internal alignment exercise on the second before you start talking to suppliers. Preferences reshape which suppliers you approach and what story your portfolio tells.

The five dimensions to align internally. Source: Senken.

The dimensions we see most: regional focus (an insurer with only German clients often wants German projects); co-benefits tied to your business (a food company leaning toward regenerative agriculture, a pharma company toward community health); supply-chain proximity (projects close to your value chain, which may later qualify under SBTi FLAG, the initiative's forest, land and agriculture guidance, and can make the supply chain itself more resilient); explicit exclusions (some companies rule out cookstoves or grid renewables on integrity grounds, others rule out a category on price); and the big one, technology versus nature. Some companies will only fund engineered removal, others only nature. A best-in-class portfolio usually includes both, weighted to the company's identity.

What we usually recommend is one cross-functional workshop, 90 minutes, with sustainability, marketing, procurement, and whichever business units are affected. Skip it and the disagreement does not go away, it just turns up again at every contracting cycle for the next three years, by which point it is a lot more expensive to settle.

Phase 3: Sourcing

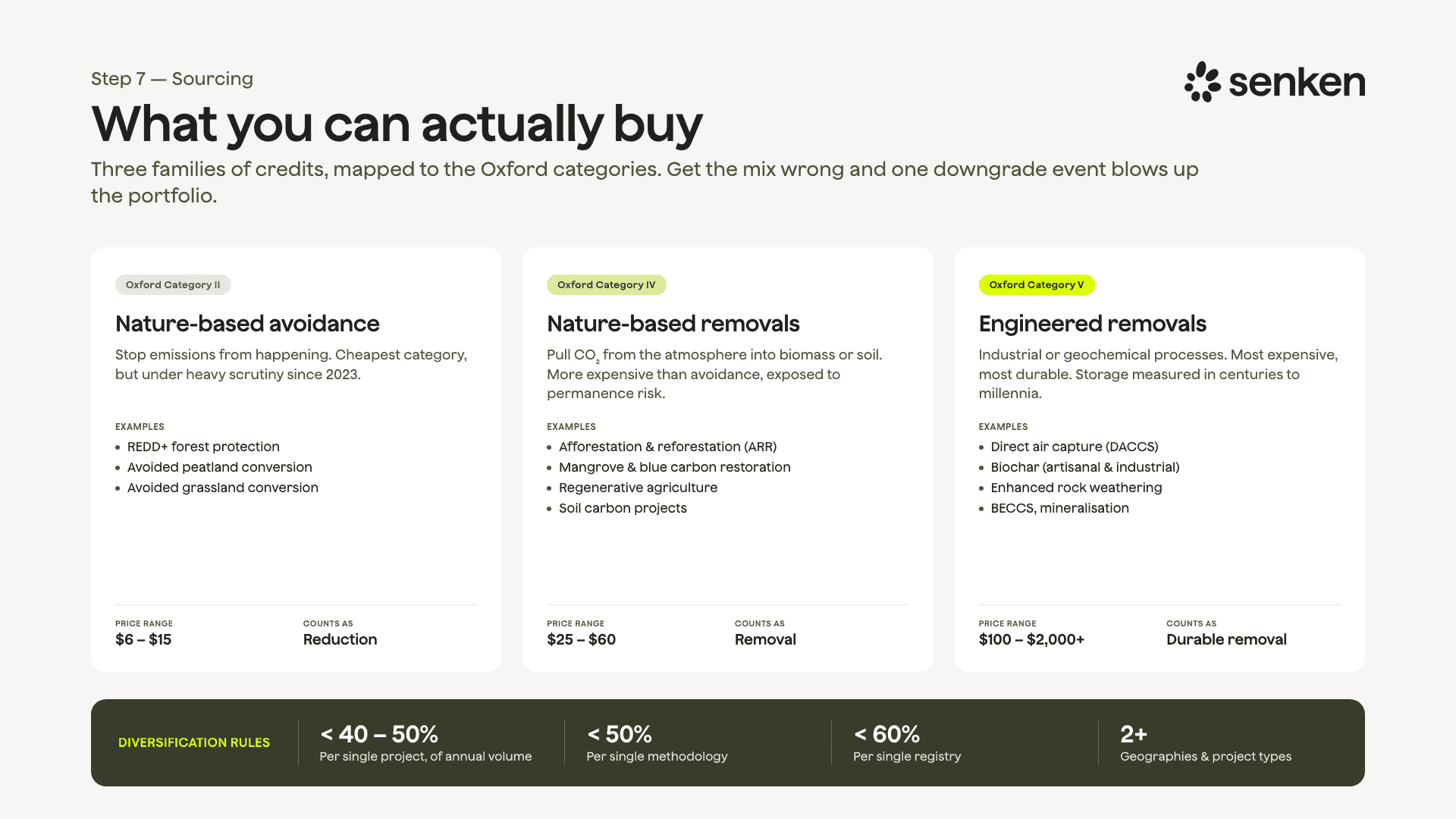

Step 7: Build a diversified portfolio

Now to what you can actually buy. There are a few families of credit, mapped to the Oxford categories.

The credit families and the diversification rules we apply. Source: Senken.

Nature-based avoidance (Oxford category two) stops emissions from happening: forest protection (REDD+, short for Reducing Emissions from Deforestation and forest Degradation), avoided peatland conversion, improved forest management. These are cheaper and under more scrutiny, but still essential for not blowing past climate tipping points in the near term. Nature-based removals (category four) actively pull CO₂ out of the atmosphere into biomass and soil: afforestation, reforestation and revegetation (ARR), mangroves, regenerative agriculture. More expensive, and necessary to reach net zero. Engineered removals are the durable end: direct air capture (DAC), biochar, enhanced rock weathering, mineralisation. Expensive, durable, and still mostly in the scaling phase, but the only way to mirror the geological carbon we burn with geological storage. There is also a fast-growing category of super-pollutant projects such as methane capture, cheaper than removals, with an outsized atmospheric impact, and showing up more and more in near-term portfolios. To make the removal end concrete: our European forest partnership with Ocell and our 81,600-tonne biochar offtake with Exomad Green are two examples of the project quality that anchors a credible 2026 portfolio.

Whatever the mix, put diversification rules on paper. As a starting point: no single project above 40 to 50% of your volume, no single methodology above 50%, no single registry above 60%, more than one geography, more than one project type. Those few caps take a lot of risk out of the portfolio for almost no cost.

Step 8: Do proper due diligence

This is the largest time driver in the whole process, the largest driver of how well your portfolio holds up over time, and the place buyers under-invest the most. There are roughly seven questions to answer for every project:

- Additionality. Would the project have happened without carbon finance? Does it pass the regulatory, barrier, and common-practice tests? If the argument rests on one narrow claim with no supporting evidence, walk away.

- Baseline, especially for avoidance. Is the counterfactual credibly constructed, or inflated to mint more credits? Inflated baselines are the most common form of over-crediting.

- Permanence. How long is the carbon stored, and what happens under fire, flood, political change, or a market shift? Is there a buffer pool, and is it sized correctly? For nature-based projects, 10 to 30% is typical.

- Leakage. Is the carbon just being pushed elsewhere, for example a protected forest while the trees next door come down? Find out what deduction has been applied.

- MRV (monitoring, reporting and verification). How is the carbon actually measured, by remote sensing, ground truth, or both, how often, and by whom?

- Social safeguards. Free, prior and informed consent, community benefit-sharing, and so on.

- Controversy history. A quick search on the project and developer, every time.

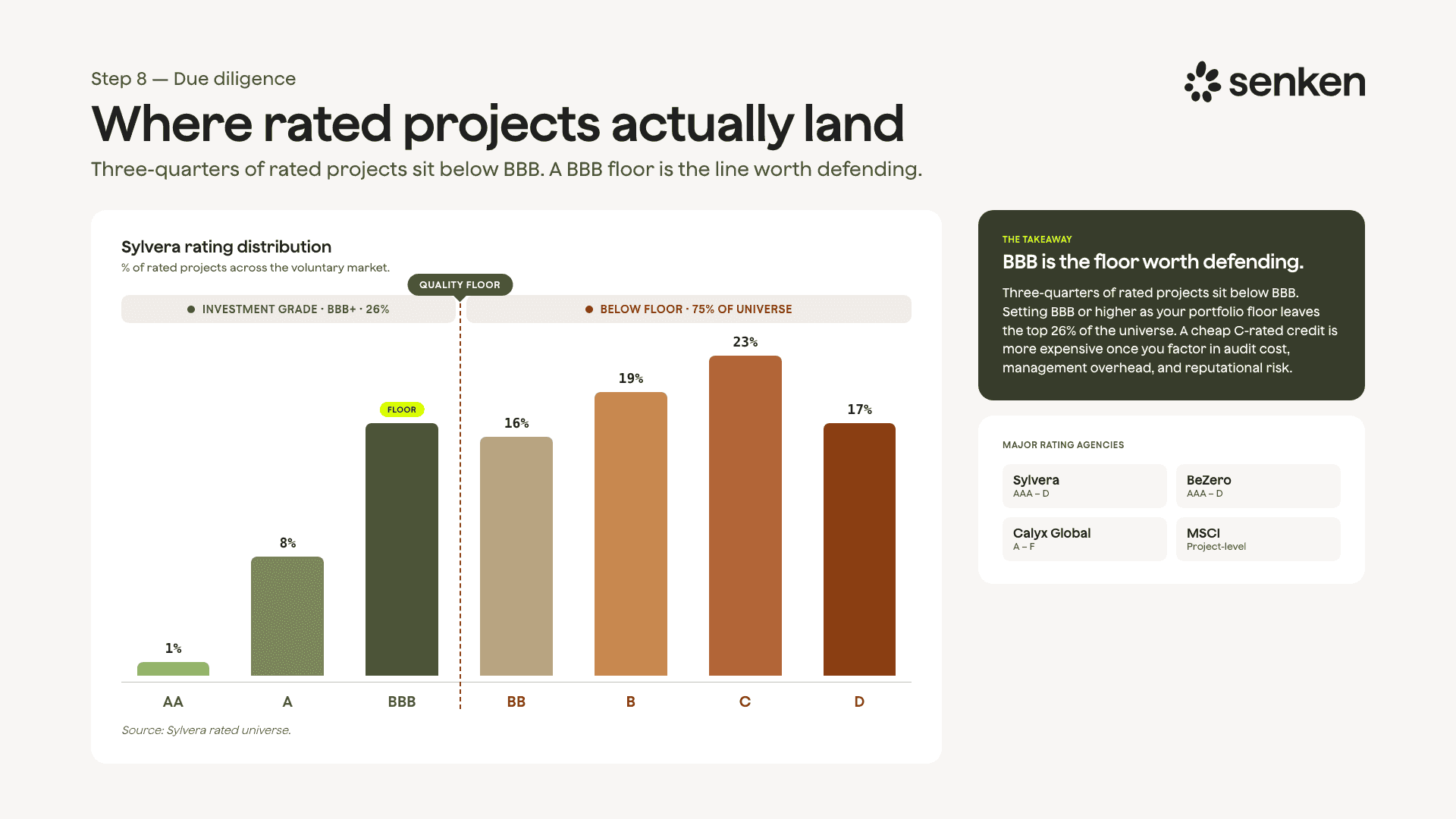

You will not do all of this from scratch on every project. This is where rating agencies earn their place: Sylvera, BeZero, MSCI Carbon Markets, and Calyx Global rate projects on a scale much like credit ratings, and you can access the ratings. Never rely on a single rating (the spread between agencies can be wide), but always check what your project scores.

Where rated projects actually land. Source: Sylvera rated universe, via Senken.

The data is sobering. Around three-quarters of rated projects sit below an investment-grade floor. Setting that floor, say BBB or higher, is one of the simplest filters you can write into a policy and defend later. This kind of screen is why we end up rejecting roughly 95% of the projects that come across our desk. And a related buyer question I hear often, "what does good enough look like in avoidance?", has the same answer: a recent vintage, a CCP-approved methodology, a credible rating, and a baseline you can defend in a room full of skeptics.

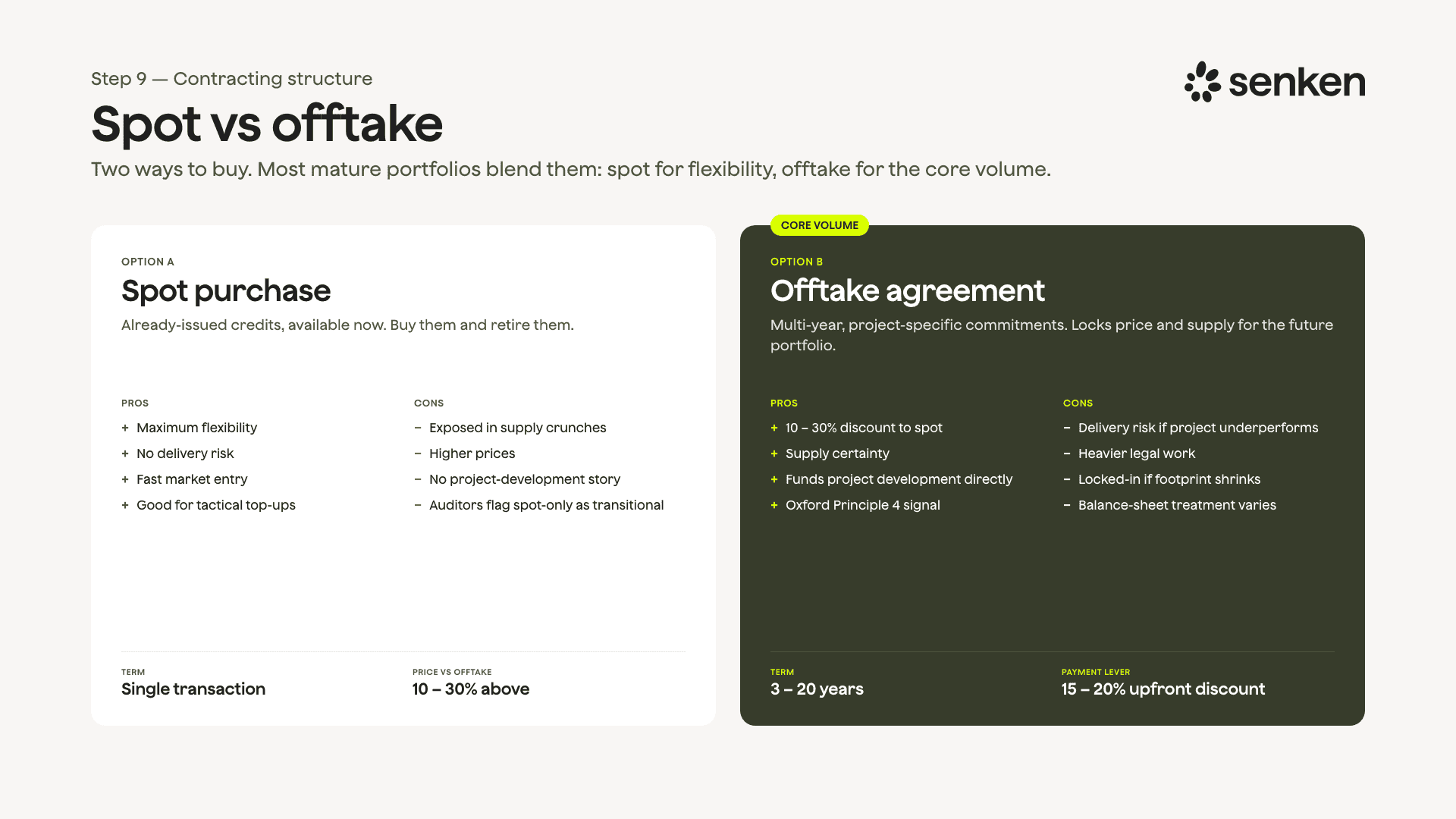

Step 9: Choose your contracting structure

You know which projects you want and that they are good. The next question is how to buy them. Two structures matter.

Spot versus offtake. Most mature portfolios use both. Source: Senken.

A spot purchase is already-issued credits, available now. Maximum flexibility, no delivery risk, but you are exposed to supply crunches and higher prices. It is a good way to enter the market and to top up tactically, but it should not be your long-term strategy. An offtake agreement is a multi-year, project- or portfolio-specific commitment, anywhere from three to twenty years. You typically get a 10 to 30% discount to spot, especially for high-quality removals, plus supply certainty and a much stronger story because you are funding project development directly. The trade-offs: delivery risk if the project underperforms, more legal work, and some lock-in if your footprint shrinks faster than expected. Those can be managed in the contract, but it is more work.

A question I get from the more sophisticated buyers is exactly this: "how do we move from buying spot credits once a year to a real long-term procurement strategy?" The honest answer is that the future commitments should be built on offtake. That is also where the economics work in your favour. Our Lufthansa removal offtake is structured this way, across multiple methodologies and several years, and one European bank we work with is moving from roughly a fifth of its portfolio in removals today toward half by 2030 on a multi-year contract. You cannot do that on the spot market.

Phase 4: Execution

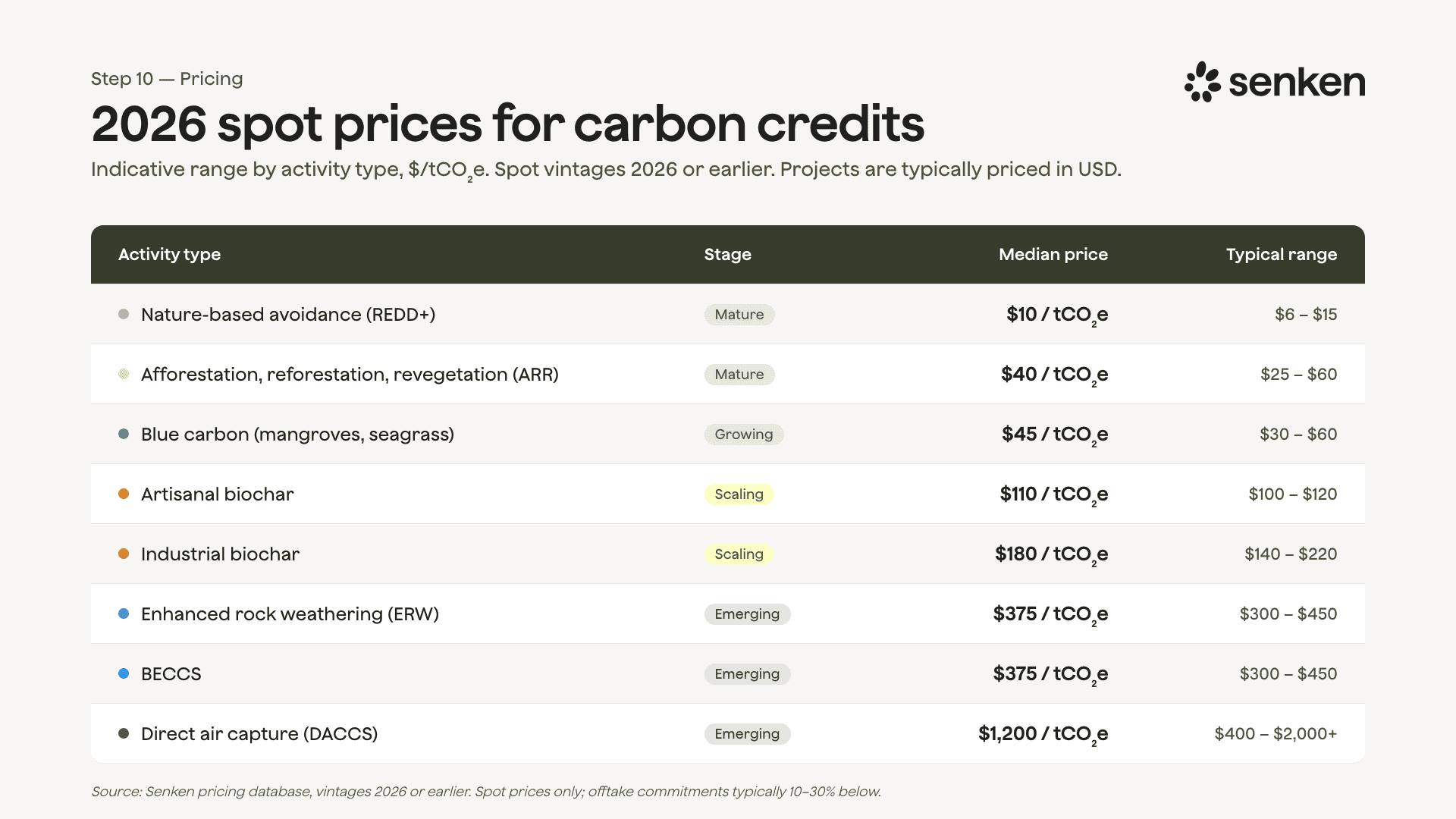

Step 10: Negotiate pricing

Now the obvious question: what should a credit actually cost? Here is the indicative range we are seeing in 2026. Note that projects are still priced in US dollars, so I would keep your modelling in dollars too.

Indicative 2026 spot prices by activity type. Source: Senken pricing database (2026 vintages or earlier).

Always get indicative quotes from at least two, ideally three, suppliers for the same volume and specification before you negotiate. The voluntary market is not liquid or transparent like a commodity exchange, so the spreads are wide, partly because quality varies so much. And the headline price is never the full cost. A $10 credit from a weak project ends up more expensive than a $50 credit from a robust one once you add in audit cost, management overhead, and the reputational hit if it goes wrong.

Payment terms are their own negotiation, and finance, controlling, and procurement need to be in the room, because multi-year upfront commitments land on your balance sheet and the accounting treatment varies by jurisdiction. The structure most of our clients choose right now is payment on delivery. You do not tie up cash until the tonnes are actually delivered and retired, which keeps that capital free for the thing that matters more, cutting your own emissions. If you can pay a deposit upfront, say 15 to 20%, you usually unlock a better per-tonne price, with a different risk profile. Get finance involved early, because the right structure here saves a meaningful amount of money and takes real risk off the table.

Step 11: Get your contracts right the first time

A spot contract can be simple. A forward structure is where the value is won or lost, and there is a lot you can lock in.

The clause I would never sign without is substitution. If you contract 100,000 tonnes and the project gets downgraded or invalidated, you need the right to be made whole with equivalent credits. Without a substitution clause you are left holding a useless asset, you still have a claim to uphold, and you still paid. Beyond that: delivery timelines with defined remedies for delays; a specification written down to the project ID, not "high-quality nature-based"; who retires the credit and in whose name; quality warranties; force-majeure definitions; reporting cooperation, audit rights, and marketing rights.

This is not simple, and if you build it from scratch your first carbon credit contract will take 12 to 24 weeks of legal review. Every contract after that should be much faster if you build a clause library and reuse it. One thing I will say plainly: do not let procurement run this off a standard commodity template. Carbon credits are not a commodity, and they fail in ways a commodity contract never anticipates. We have seen that one go wrong too many times.

Phase 5: Ongoing

Step 12: Monitor your portfolio

Your contracts are signed, and the work shifts from procurement to portfolio management. Most companies stop here. That is a mistake, because this is where a portfolio quietly goes bad. There are five things I would track:

- Delivery. Contracted versus delivered versus retired versus outstanding, by project and by year. Monthly or quarterly, depending on how many projects you hold.

- Project performance. MRV milestones, monitoring reports, verification cycles. Delays are the leading indicator that something is wrong. One delay can be fine, a pattern is not.

- Registry updates. Revisions, holds, downgrades, methodology version changes.

- Rating updates. Track the portfolio-weighted average rating across the agencies, flag any downgrade immediately, and assess whether your substitution clause needs to trigger.

- Rebalancing. At year-end, review against your Oxford glide path. Are you on track to your removal target for 2030? If not, what changes in the next sourcing cycle?

For each of these, have a contingency protocol. What gets triggered, and within how many days, on a downgrade or an invalidation? Keep a pre-approved substitute project list so you are not starting from zero in a crisis. The first time a journalist tells you your project got downgraded is the wrong moment to discover your monitoring has been failing.

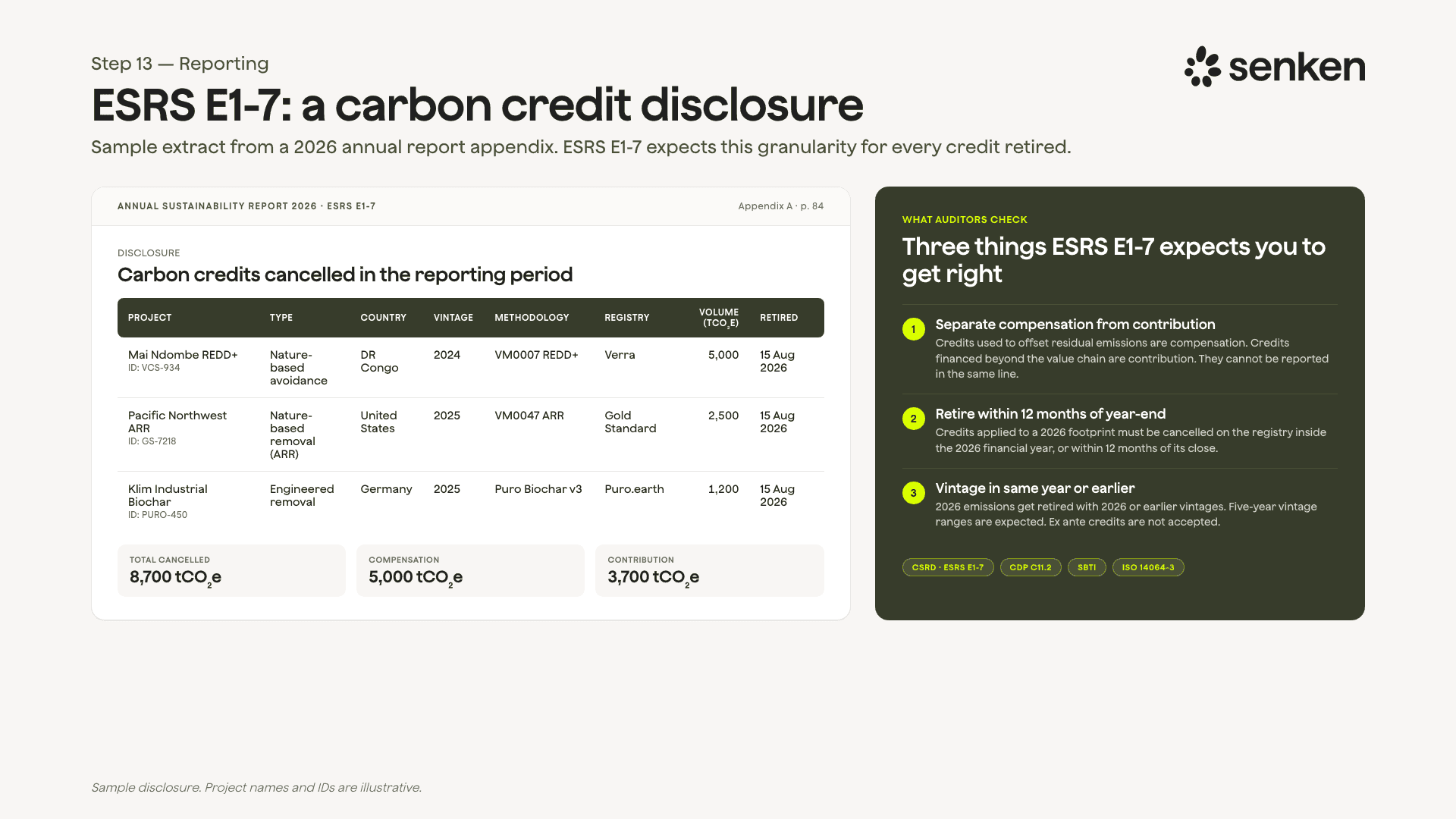

Step 13: Report transparently

Most companies will have to report on their credits somewhere, most often under CSRD. So check where your obligations sit, then disclose at the granularity the rules expect.

What an ESRS E1-7 disclosure looks like. Source: Senken (illustrative).

Under CSRD, the relevant datapoint in the European Sustainability Reporting Standards (ESRS) is E1-7, "GHG removals and GHG mitigation projects financed through carbon credits." It expects per-credit detail: volume, project type, project name and ID, country, vintage, methodology, registry, and retirement date. Two things to get right. First, separate compensation from contribution, and never net credits against your gross emissions: they are disclosed alongside the inventory, not subtracted from it. Second, retire credits within 12 months of your financial year-end, and keep the vintage in the same year or earlier. (Worth noting: the 2025 EU Omnibus package is narrowing and delaying who falls into CSRD scope, so confirm your own timing, but the disclosure logic for those in scope is unchanged.) For a sense of how badly this is currently done, our Buying Blind analysis of DAX40 disclosures found that 45% of retired credits were untraceable.

This is also where an insurer recently asked me a very practical question: "can I use all of these projects in my CSRD report?" The answer is not automatic. Ex-ante credits and EU ETS allowances, for example, do not belong in that disclosure. Eligibility is exactly the kind of thing your step-3 matrix should already have told you.

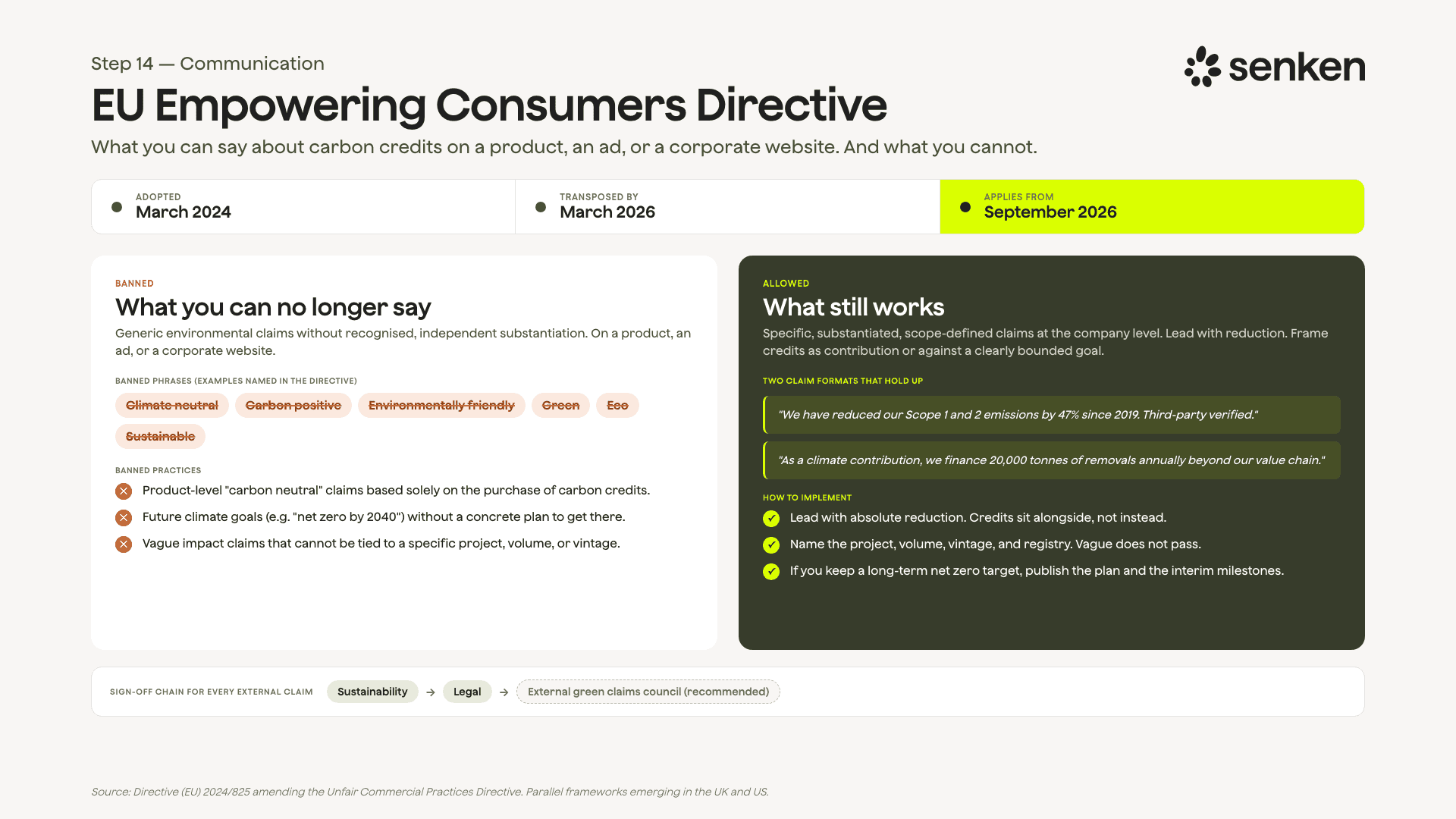

Step 14: Communicate without getting sued

The last step is the one that has changed the most. The single most consequential regulation for the marketing side of a carbon strategy in Europe is the Empowering Consumers for the Green Transition Directive. It was adopted by the EU in 2024 and amends the Unfair Commercial Practices Directive. Member states must transpose it into national law by 27 March 2026, and it applies from 27 September 2026. That is very soon.

What you can and cannot say under the EU Empowering Consumers Directive. Source: Senken.

It bans generic environmental claims that are not backed by recognised, demonstrated performance: "climate neutral," "carbon positive," "environmentally friendly," "green," "eco," "sustainable." Put any of those on a product or an ad without independent substantiation and you are exposed, and the lawsuits are already arriving. The biggest single change is on offsetting: the directive prohibits a product-level claim that a product is carbon neutral if it rests solely on the purchase of carbon credits. That is why the "climate neutral" sticker is disappearing from packaging, and why a lot of strategies have had to change. It also bites on future goals: if you advertise a net zero target for, say, 2040 without a credible plan to get there, that claim is not allowed either.

What you can still say are specific, substantiated, scope-defined claims at the company level. "We reduced our scope 1 and 2 emissions by 47% since 2019, third-party verified" is fine. "As a climate contribution, we finance 20,000 tonnes of removals a year beyond our value chain" is fine. So if you have a long-term net zero target, you do need a carbon credit strategy, there is no way around it, but the way to communicate it is to lead with reduction, frame the credits as a contribution or a specific scoped goal, and show the actual projects. Vague claims are what gets challenged. Sign off every external claim with sustainability and legal, ideally with an external green-claims reviewer too. And this is not only an EU story: the UK has its own framework, and the US is moving in the same direction. This trend is not going away.

Where this leaves you

That is the full framework: foundation, strategy, sourcing, execution, ongoing. Built in this order, the portfolio holds up when someone serious starts pulling on it. Built the other way round, starting from whatever happens to be for sale this quarter, it tends to come apart in exactly the places nobody checked.

It is a lot of work, which is why we built a platform that covers most of these steps in one place: our Sustainability Integrity Index for due diligence, curated portfolios of vetted projects, contract templates with substitution clauses built in, and reporting packages for CSRD, CDP, and SBTi. If you are building or refining your strategy, talk to us. It is far more manageable with a partner who has done this before, and it beats discovering the gaps in the middle of an audit.