SBTi Ongoing Emissions Responsibility (OER): The Final Rules and How to Prepare

Updated June 11, 2026.Rewritten for the final Corporate Net-Zero Standard V2.0, published by SBTi today.

For years the message to companies was to cut emissions first and worry about credits much later, somewhere near the 2050 finish line. The final Science Based Targets initiative (SBTi) Corporate Net-Zero Standard V2.0, published on June 11, 2026 and effective from February 1, 2027, changes that. It gives carbon credits a defined, structured role from the moment a company sets a target, through a mechanism called Ongoing Emissions Responsibility (OER).

For sustainability and procurement teams at SBTi-committed companies, OER turns a vague future obligation into a near-term planning question. This guide explains what OER is, the three recognition levels and exactly what they require, the public declaration every company will make at validation, which credits qualify, what it is likely to cost, and how to prepare before the first validations in early 2027. Every rule here comes from the final Corporate Net-Zero Standard V2.0, with criterion numbers cited so your team can verify against the source.

If you want the wider picture of everything that changed in version 2.0, we covered that in our breakdown of the final V2.0 standard. This article goes deep on the OER part specifically.

What ongoing emissions responsibility actually is

Ongoing emissions are the greenhouse gases a company keeps releasing every year while it works toward net zero. SBTi draws a useful line here. Residual emissions are the smaller slice that remains in the net-zero year after a company has done all the abatement its science-based pathway allows. So all residual emissions are ongoing emissions, but most ongoing emissions are not yet residual. OER is about the bigger number: the emissions you are still producing on the way down, not just the ones left at the end.

OER replaces the framing that used to be called Beyond Value Chain Mitigation, or BVCM. We explained the old concept in our BVCM explainer. BVCM has not disappeared. It is now one way to take responsibility under a wider umbrella. SBTi widened the scope because the value-chain distinction was limiting: a removal project can sit inside or outside a company's value chain, and companies also wanted to fund things like adaptation that BVCM did not cleanly cover.

Under OER, a company can take responsibility through two routes:

- Verified mitigation outcomes. Funding activities that reduce emissions outside your value chain, protect or restore natural carbon sinks, or remove carbon from the atmosphere (criterion C41.1). Outcomes must be measured after the fact and independently verified; in practice this means high-integrity carbon credits, retired at the moment they are claimed. Avoided emissions calculated at product level are explicitly not eligible.

- A contribution budget. Applying a carbon price to covered emissions and directing the money toward eligible activities: verified mitigation, forward agreements for removals not yet delivered, low-carbon research and development, adaptation and resilience, or loss-and-damage response (C41.3).

The first route delivers measurable tonnes now. The second also funds the scale-up of solutions the world will need later. A company can use either, or both, and the budget route is what makes forward offtakes for early-stage removal projects count.

Every company must answer, publicly

This is the part of the final standard that changes the conversation in most boardrooms. Participation in OER is voluntary, but taking a position is not. At target validation, every company states whether it takes part. The answer is displayed on the public SBTi Dashboard, and a "no" requires a written explanation to SBTi (criterion C38).

That inverts the usual dynamic. Until now, the company buying credits was the one explaining itself. From the first V2.0 validations in 2027, the company not buying is the one writing the explanation, in public, where customers, investors, and procurement teams can read it.

Recognition itself is awarded at the end-of-cycle assessment, and only to companies that are delivering on their validated targets (C39). OER is designed as a complement to cutting your own emissions, never a substitute.

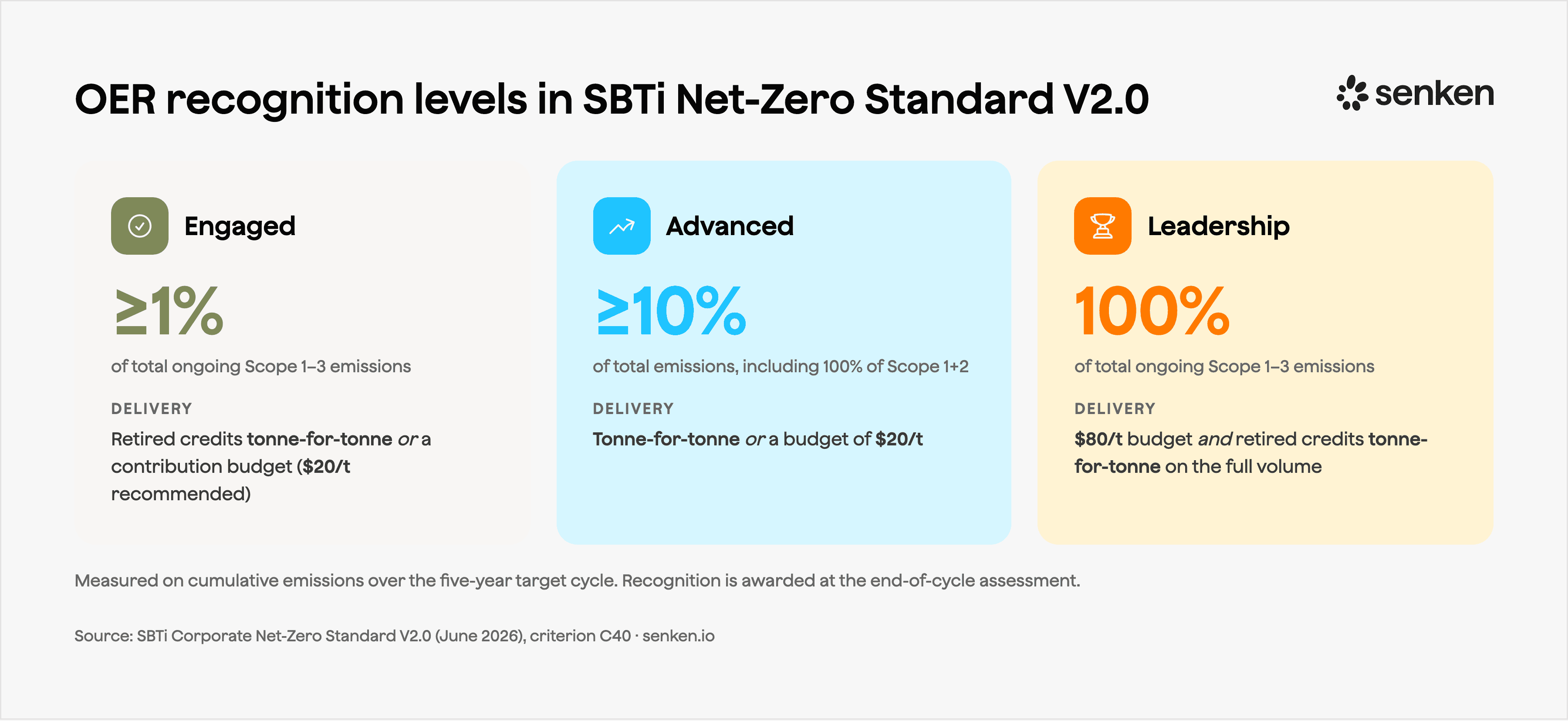

Engaged, Advanced, Leadership: the three levels

The final standard defines three recognition levels (criterion C40), all measured against cumulative scope 1, 2, and 3 emissions over the five-year target cycle. The two-tier structure from the draft (Recognized and Leadership) is gone.

| Engaged | Advanced | Leadership | |

|---|---|---|---|

| Coverage of ongoing scope 1-3 emissions | At least 1% of the total | 100% of scope 1 and 2, and at least 10% of the total | 100% of the total |

| How to meet it | Retired credits matching the covered volume tonne for tonne, or a contribution budget | Same choice: tonne for tonne, or budget | Budget and retired credits for the full covered volume, both |

| Carbon price | None mandated; SBTi recommends at least $20 per tonne | $20 per tonne | $80 per tonne |

A few things worth pulling out. Engaged is deliberately accessible. SBTi's own modelling for the program weighed corporate profits, emissions intensity, and credit prices across sectors and landed on 1% as a level high enough to signal real action but low enough that most companies can reach it. The $20 benchmark sits between the cheapest reduction credits and widely available nature-based removals like afforestation.

Advanced is the new middle rung, and its logic is worth understanding: full coverage of the emissions you control directly (scope 1 and 2), plus a meaningful share of the value chain. For most companies scope 3 dominates the inventory, which is why full scope 1 and 2 coverage often lands well below the 10% total on its own.

Leadership got stricter than the draft proposed. The draft asked for at least 40% of the contribution budget to flow into verified mitigation; the final version requires retired credits matching 100% of covered emissions on top of the $80 per tonne budget, with remaining funds going to other eligible climate actions. SBTi describes this level as the full internalization of the cost of climate change. (Smaller Category B companies can reach Leadership at 10% coverage.)

Two mechanics matter for planning. Outcomes must have occurred within the five years before the reporting year (C41.2), and the budget must be fully disbursed within the same five-year cycle, with progressive disbursement recommended rather than a single end-of-cycle purchase (C40.8). Companies can also split coverage of the same scope 3 emissions with value chain partners under a written agreement (C40.7).

The timeline, and the 2030 versus 2035 question

This is where buyers get confused, so it is worth being precise. The dates are now fixed:

- June 11, 2026. The final standard is published. The structure below no longer moves.

- February 1, 2027. V2.0 becomes effective and validations begin in Q1 2027. From the first validation, every company declares its OER position publicly, and the Engaged, Advanced, and Leadership levels open.

- End of 2027. Version 1 closes for target setting. From 2028, companies with 2030 targets set their next cycle (2030 to 2035) under V2.0.

- From 2035. Supporting carbon removals stops being voluntary for Category A companies (broadly: turnover of €450 million or more, or 1,000+ employees, with lower thresholds in high-income countries). Coverage starts at 1% of ongoing scope 1, 2, and 3 emissions and rises in a straight line to 100% by the company's net-zero year, no later than 2050 (criterion C45).

So when a colleague asks "is it 2030 or 2035?", the answer is 2035 for the mandatory obligation. The 2030 date people half-remember is the global science milestone of halving emissions, not an OER deadline. And note what changes in 2035: the voluntary program accepts reduction credits and sink protection, but the mandatory requirement is met with carbon removals only.

One more date sits at the far end. In a company's net-zero target year, all residual emissions are neutralized with removals, and durability is matched to the gas: the share of covered emissions from long-lived greenhouse gases must be met with long-lived removals, phasing from 10% in 2035 to 100% by the net-zero year (C45.4, C46). The draft's fixed 41% durable share is gone. We walk through the removal volumes this produces, with a worked example, in the V2.0 breakdown.

Which credits actually count

The voluntary program is permissive on type. Reduction credits from outside your value chain, projects that protect or restore natural carbon sinks, and removals all qualify toward Engaged, Advanced, and Leadership (C41.1). The catch is the word integrity, and the final standard spells it out in criterion C42: unique registry recording, conservative ex-post quantification against baselines that tighten over time, leakage mitigation, project-level additionality, reversal-risk safeguards with compensation, and accredited third-party verification. The market's working proxy for that bar is the ICVCM Core Carbon Principles label. The 2024 Nature study on credit integrity found the large majority of assessed credits at high risk of not delivering what they claimed, which is why screening matters more than price.

One nuance buyers ask about: regulatory surplus. At the Engaged level, mitigation must go beyond what regulation already requires. At Advanced and Leadership, mitigation used for compliance purposes may be counted, subject to the same integrity criteria (C42.2.f).

In practice, the integrity bar pushes buyers toward a shrinking set of defensible categories. Here is how we see the methodology landscape for a portfolio that needs to survive scrutiny:

- Afforestation and reforestation (ARR). The highest-quality nature-based removal category, and badly supply-constrained. Roughly €17 to €70 per tonne.

- Biochar. The commercial workhorse on the removal side, with permanence measured in hundreds of years. From about €120 per tonne. German projects are a genuine advantage for German buyers.

- Direct air capture (DAC). A credibility anchor rather than a volume play, at €1,500 and up per tonne.

- Older avoidance categories like legacy REDD+, grid-connected renewables and many cookstove projects. We mostly screen these out. Additionality and over-crediting concerns make them hard to defend in a disclosure.

From 2035 the rules tighten: the mandatory requirement is removals only, with the durable share rising from 10% toward 100%. The market is moving toward durable removal, and the supply of high-quality removal credits is the constraint, not the demand. We made the fuller case for removal versus avoidance separately.

And one wall to respect in every report you publish: OER never reduces your reported footprint. Contributions are accounted for separately from the greenhouse gas inventory and cannot be netted against scope 1, 2, or 3 (C43). Credits must be permanently retired when claimed, no other actor may claim the same outcome, and tonnes used for OER cannot be reused for the 2035 requirement or net-zero neutralization.

What it is likely to cost

The honest answer is that it depends on your emissions and which level you target, but the final numbers let you model a range.

At the Engaged level, the budget route uses a simple formula: covered emissions multiplied by a carbon price of at least the recommended $20 per tonne. SBTi's modelling, published with the draft framework, illustrated the scale: for an emissions-intensive sector like chemicals, a 1% responsibility level works out to roughly 0.4% of annual profit, around $15 million; for a lighter sector like food and drink, closer to 0.1% of profit, around $5 million. Those figures scale as coverage rises through Advanced and toward the post-2035 ramp.

The tonne-for-tonne route is priced by what you actually buy. At current market prices, 1% covered with afforestation credits is cheaper than the same volume in biochar, which is far cheaper than DAC. The mix you choose is a quality and durability decision as much as a budget one.

Leadership is materially more expensive than the draft version, because the $80 price applies to 100% of ongoing emissions and the full covered volume must also be matched with retired credits. For most large emitters that runs into eight or nine figures a year, which is why SBTi frames it as full cost internalization and why it will stay rare.

One cost lever is timing. Sylvera's day-one analysis of the final standard estimates that the roughly 11,000 SBTi-aligned companies retired around 20 million tonnes of credits in 2026, about a sixteenth of what the 1% Engaged floor alone implies, and models SBTi-driven demand reaching 293 million to 1.1 billion tonnes a year by 2035 if companies pursue recognition at scale. Buying removal supply now, or locking future delivery through forward and offtake contracts, hedges against the price rises that demand will create.

How to calculate your 1%

Three practical steps for the Engaged level:

- Start from ongoing scope 1, 2, and 3 emissions, not just operational emissions. OER covers all three scopes, and for most companies scope 3 is the bulk of the number. The measurement basis is cumulative emissions over your five-year target cycle, so multiply a typical year by five for the full-cycle picture.

- Take 1% of that total. That is the tonnage you cover tonne for tonne, or the emissions base you apply your carbon price to for the budget route.

- If your scope 3 data is incomplete, use your best current inventory and a conservative estimate, and document the basis. A 1% commitment is forgiving of imperfect scope 3 data in a way that a 100% neutralization claim never would be, so missing scope 3 precision is not a reason to wait.

Should you opt in now, or wait?

The standard is final, so the question is no longer whether these rules arrive. It is whether you answer the declaration with a plan or an explanation.

The declaration makes inaction visible. From the first V2.0 validations in 2027, you state whether you participate, the answer is public, and declining requires a written explanation to SBTi. Several of the procurement teams we work with are already asking suppliers what their plan is.

Early movers also shape supply and price. The high-quality removal credits that will satisfy the rising post-2035 requirement are in short supply today. Companies that build relationships and lock forward contracts now will have more choice and better prices than those entering a crowded market in the early 2030s. The five-year disbursement rule rewards the same behavior: spreading purchases across the cycle is exactly what SBTi recommends.

This is exactly the problem our SBTi OER portfolio is built for: an audited, V2.0-aligned portfolio sized to your coverage level, with payment on delivery so you are not tying up capital. For the mandatory post-2035 removal requirement, our 2035 Reserve locks future removal supply at a fixed price today.

What is still open

Two things can still move. The post-2035 criteria carry an explicit disclaimer that they will be reviewed in Version 3 of the standard before they take effect in 2035. And SBTi plans a Call for Evidence on whether removals with shorter storage, biochar's 100 to 1,000 years for example, can be treated as equivalent to long-lived storage through contractual or financial mechanisms. The OER program itself, the three levels, the $20 and $80 benchmarks, the declaration, and the February 2027 start are fixed.

Ongoing Emissions Responsibility moves carbon credits from a 2050 afterthought to a question on this year's agenda. The companies that treat it as a planning problem now, rather than a compliance scramble in 2035, will spend less and have better options. If you want help sizing your coverage and building a portfolio that holds up to scrutiny, talk to our team.