SBTi Net-Zero Standard V2.0: What the June 2026 Update Changes for Corporate Carbon Credit Strategy

Updated June 11, 2026.SBTi published the final Corporate Net-Zero Standard V2.0 today.

The Science Based Targets initiative (SBTi) published the final Corporate Net-Zero Standard V2.0 on June 11, 2026. The standard becomes effective on February 1, 2027, with target validation under the new rules starting in Q1 2027. After two consultation drafts and more than a year of public debate, the rules for corporate net-zero are now fixed, and they answer the question buyers have been asking all year: what role do carbon credits actually play?

The short answer has three parts. Credits still cannot be counted toward scope 1, 2, or 3 targets. From 2027, a voluntary recognition program rewards companies that take responsibility for the emissions they have not yet cut. And from 2035, large companies are required to buy carbon removals, starting at 1% of their footprint and rising every year until their net-zero year.

What the final standard changed from the draft

If you planned against the November 2025 draft, these are the revisions that matter as of the final text published on June 11, 2026:

- The recognition tiers were renamed and restructured. The draft's two tiers (Recognized and Leadership) became three: Engaged, Advanced, and Leadership.

- Leadership got more demanding. The draft asked for at least 40% of the contribution budget to flow into credits. The final version requires retired credits matching 100% of covered emissions, on top of the $80 per tonne budget.

- The 41% durability rule is gone. Instead of a fixed durable share by 2050, the final standard phases durable removals in from 10% in 2035 to 100% by the net-zero year.

- The double-claiming ban became a recommendation. The draft required removals used for neutralization to carry host-country corresponding adjustments and barred credits that are also claimed toward a country's climate targets. The final standard asks companies to report the authorization status (criterion C46.6) and recommends avoiding double-claimed removals, nothing stricter.

- The timeline is now fixed. Effective February 1, 2027. Version 1 remains open for target setting until the end of 2027, and there is no forced migration in 2028: companies with 2030 targets set their next target cycle (2030 to 2035) under V2.0 from 2028.

- Net-zero targets are now optional. What every company must set are near-term five-year targets (scope 1 and 2 for all, scope 3 for large companies). The overarching net-zero target, including neutralization, is a choice.

- Scope 3 responsibility can be shared. Both the voluntary program and the 2035 requirement let companies split coverage of the same scope 3 emissions with value chain partners under a written agreement.

Where carbon credits count under V2.0

The standard sorts every possible use of a credit into four distinct roles, each with its own rules:

- Your emissions targets: no credits, ever. Progress against scope 1-3 targets is measured on your physical greenhouse gas inventory alone. Credits used for the recognition program, credits sold on to someone else, and reductions that exist only on paper before delivery are all explicitly excluded (criterion C26.2).

- Ongoing Emissions Responsibility, from 2027: voluntary, open to all credit types. Reduction credits from outside your value chain, projects that protect or restore natural carbon sinks, and removals all qualify.

- The 2035 requirement: mandatory, removals only. Category A companies must support removals covering a rising share of their ongoing emissions.

- The net-zero year: removals only, durability-matched. Whatever a company still emits at and after its net-zero year is neutralized with removals, and long-lived gases need long-lived storage.

One instrument class sits outside all four roles: market instruments. The final standard formally recognizes energy attribute certificates and commodity certificates, including book-and-claim and mass-balance chains of custody, as legitimate target implementation where emissions sit in shared systems such as power grids, gas grids, or logistics networks (section 4.2 of the standard). They are reported separately from the inventory, must meet integrity criteria on activity matching, conservative quantification, and double-counting prevention, and for scope 1 they are limited to fuels and feedstocks. For procurement teams the line to draw is this: a sustainable aviation fuel certificate is a recognized way to work on a scope 3 target under these rules, while a carbon credit belongs to the recognition program, the 2035 requirement, and neutralization.

Ongoing Emissions Responsibility: the new home for credit purchases

Ongoing Emissions Responsibility (OER) is V2.0's answer to a structural gap: companies emit for decades while working toward their targets, and until now the SBTi framework said nothing about those ongoing emissions. Our OER deep-dive covers the program in full; here is what the final standard, as published on June 11, locks in.

Participation is voluntary, but the declaration is not. At target validation, every company states whether it takes part. The answer is displayed on the public SBTi Dashboard, and a "no" requires a written explanation to SBTi (criterion C38). That inverts the usual dynamic: instead of defending a credit purchase, companies will publicly explain why they are not making one.

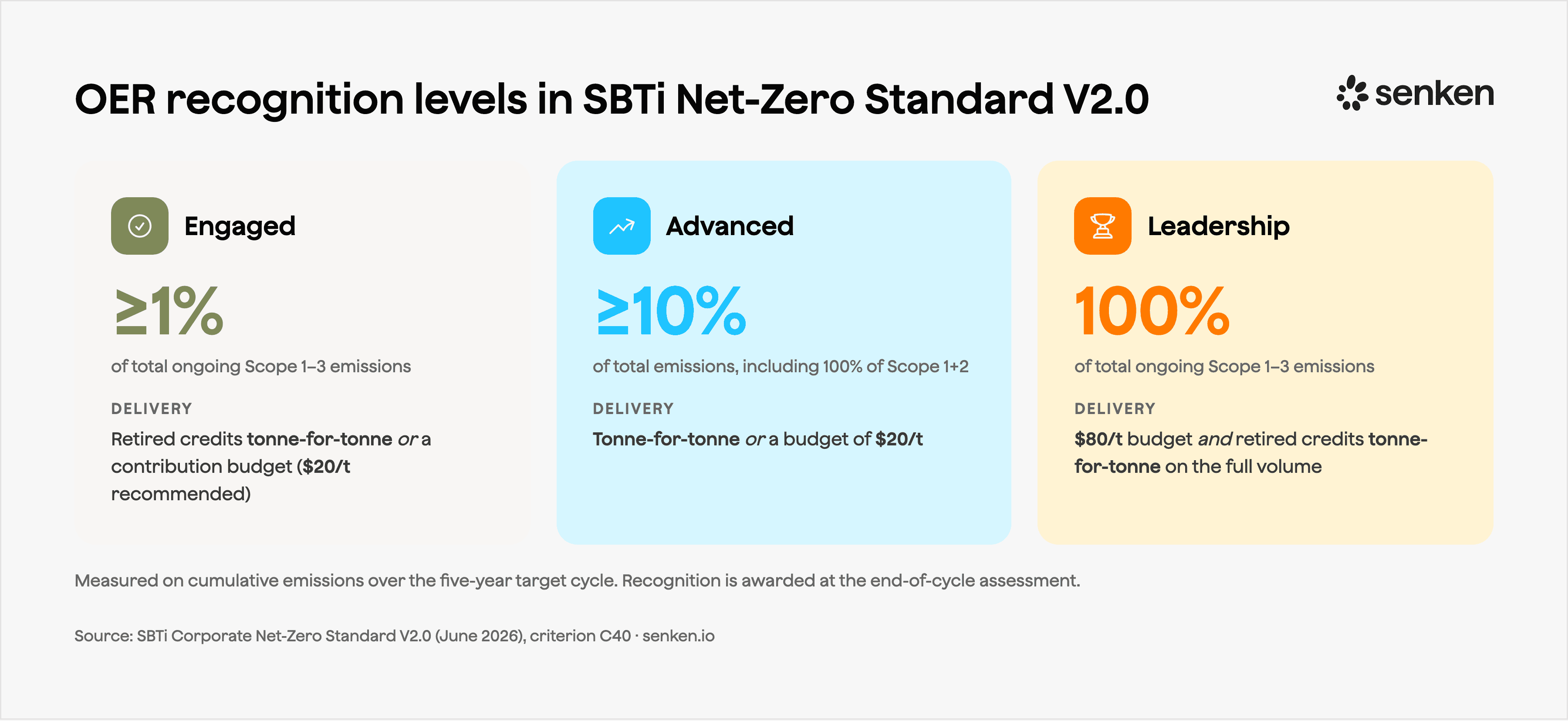

The program recognizes three levels, all measured against cumulative scope 1, 2, and 3 emissions over the five-year target cycle:

- Engaged. Cover at least 1% of total ongoing emissions, either with retired credits matching the covered volume tonne for tonne, or with a contribution budget (no price is mandated; SBTi recommends at least $20 per tonne).

- Advanced. Cover 100% of scope 1 and 2 emissions, and at least 10% of total ongoing emissions, again tonne for tonne or with a budget of $20 per tonne.

- Leadership. Cover 100% of all ongoing emissions with a budget of $80 per tonne, and deliver retired credits for the full covered volume. Remaining funds go to other eligible climate actions. SBTi describes this level as the full internalization of the cost of climate change.

What qualifies is tightly defined. Outcomes must be measured after the fact, independently verified, and permanently retired at the moment they are claimed, and they must have occurred within the five years before the reporting year. A contribution budget can also fund forward agreements for removals that have not yet been delivered, low-carbon research, adaptation, and loss and damage.

One wall the final standard did not soften: OER never reduces your reported footprint. Contributions are accounted for separately from the inventory and cannot be netted against scope 1, 2, or 3. A company claiming its scope 3 went down because it bought credits is making a claim V2.0 explicitly rules out.

The gap between these levels and current practice is wide. Sylvera's day-one analysis estimates that companies with science-based targets retired around 20 million tonnes of credits in 2026, roughly 0.06% of their combined footprint, or about a sixteenth of what the Engaged floor alone implies. Their scenarios put SBTi-driven credit demand between 293 million and 1.1 billion tonnes a year by 2035 if companies pursue recognition at scale.

Mandatory removals from 2035

This is the part of the standard with the longest fuse and the largest budget implications. From 2035, Category A companies (broadly: turnover of €450 million or more, or 1,000+ employees, with lower thresholds for companies in high-income countries) are required to support carbon removals (criterion C45).

Two percentages govern the obligation, and they climb at the same time:

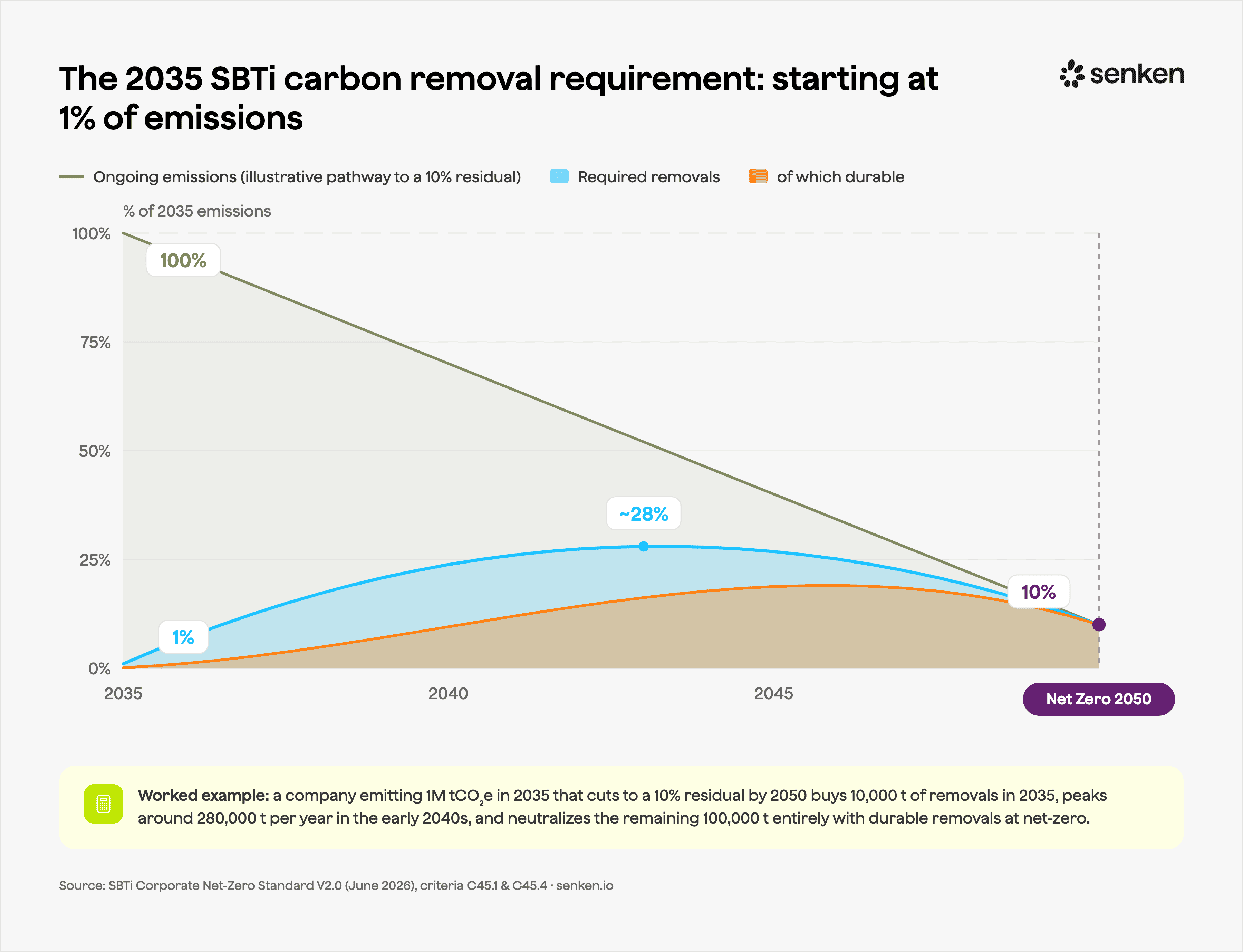

- Coverage. Removals must cover 1% of ongoing scope 1, 2, and 3 emissions in 2035, rising in a straight line to 100% by the company's net-zero target year, and no later than 2050.

- Durability. Of the covered CO2, at least 10% must be met with long-lived removals in 2035, meaning storage measured in centuries to millennia, such as direct air capture with geological storage or mineralization. That share also rises in a straight line to 100% by the net-zero year.

For a company emitting 1 million tonnes in 2035 that reduces to a 10% residual by 2050, the obligation starts at 10,000 tonnes of removals in 2035, peaks around 280,000 tonnes a year in the early 2040s, and settles at 100,000 tonnes at net-zero, by then fully durable and neutralizing everything that remains. The 1% start is the smallest the obligation will ever be.

Worth knowing: the post-2035 criteria carry an explicit disclaimer that they will be reviewed in Version 3 of the standard before they take effect, and SBTi plans a Call for Evidence on whether removals with shorter storage, biochar sits at 100 to 1,000 years for example, can be treated as equivalent to long-lived storage through contractual or financial mechanisms. The direction is settled, even if the exact parameters may move once more.

What happens at the net-zero year

For companies that set the optional net-zero target, criterion C46 defines the end state. All scopes are reduced to residual levels, and every remaining tonne is neutralized with removals in the same reporting period it is emitted. Removals may come from inside or outside the value chain. Residual long-lived gases require long-lived storage. Companies answer directly for their scope 1 residuals; scope 3 residuals can be neutralized jointly with value chain partners, but the obligation falls back on the company where no partner demonstrates it.

One detail with Article 6 implications: companies must report whether the removal credits used for neutralization are authorized by the host country and subject to corresponding adjustments, and SBTi recommends avoiding removals that are simultaneously claimed against national climate targets. For European buyers this is one of the quiet wins of the final text. The draft made corresponding adjustments a hard requirement, which would have excluded removals certified under the EU Carbon Removal Certification Framework (they count toward EU member states' national targets) and state-supported BECCS projects in Denmark and Sweden. As a reporting duty plus a recommendation, the final standard keeps those European removals eligible for neutralization.

The V2.0 timeline at a glance

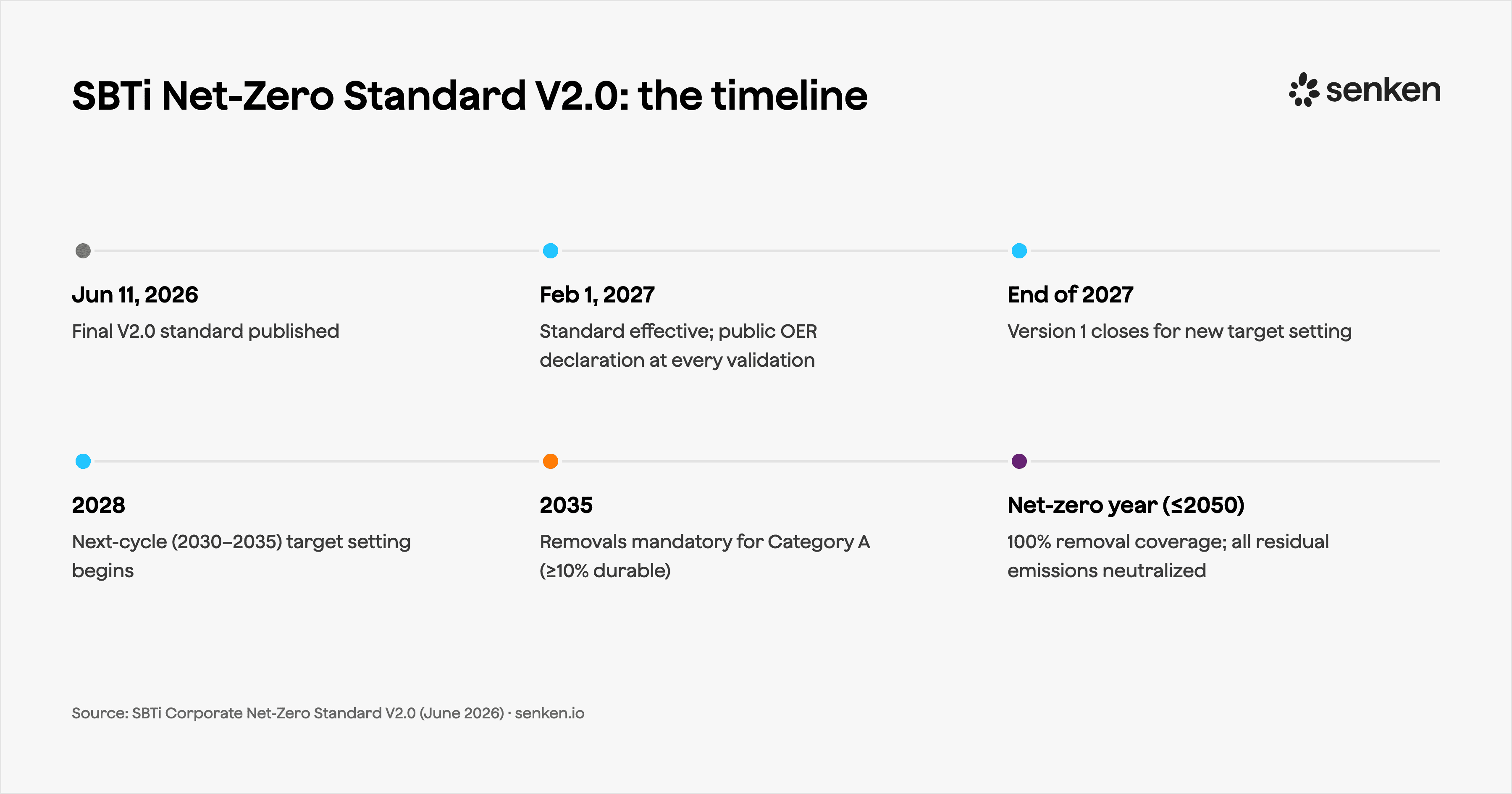

- June 11, 2026: Final Corporate Net-Zero Standard V2.0 published.

- February 1, 2027: The standard becomes effective; validation under V2.0 begins in Q1 2027. From the first validation, every company declares its OER position publicly.

- End of 2027: Last chance to set targets under Version 1.

- 2028: Companies with 2030 targets start setting their 2030 to 2035 cycle targets under V2.0.

- 2035: Removal purchases become mandatory for Category A companies, with at least 10% of covered CO2 met by durable removals.

- Net-zero year (2050 at the latest): Removal coverage reaches 100% and all residual emissions are neutralized.

What corporate buyers should do before 2027

Three moves cover most situations:

- Model the ramp against your own footprint and net-zero year. The arithmetic is mechanical: take scope 1, 2, and 3 emissions, apply the coverage ramp, and you have a year-by-year volume schedule. For most Category A companies the line crosses tens of thousands of tonnes per year well before 2040, which puts 2035 inside a normal procurement planning horizon today.

- Decide your OER answer before your next validation. You will be asked, and the answer is public. Engaged at 1% is deliberately accessible, and the $20 and $80 benchmarks give finance teams a defensible anchor for the budget conversation.

- Line up durable removal supply early. Long-lived removal capacity is the scarcest part of the market today. At Senken we screen projects across more than 600 data points, and roughly the top 5% pass. Contract structure matters as much as project quality here: delivery-matched payment keeps capital free until the obligation actually lands.

If you want to act on SBTi V2.0 now, Senken offers two ways to start. The OER Portfolio covers the voluntary recognition program from the Engaged level up. The 2035 Reserve secures durable removal supply against the mandatory requirement, with payment on delivery. Reach out to the Senken team to model your numbers.

The final standard gives buyers what the drafts could not: fixed dates and numbers to plan against. The 2027 budget round is the natural place to start.