⌛SBTi V2 just put corporate removals on the clock

Last week, SBTi published the final Corporate Net-Zero Standard V2.0.

After two consultation drafts and a year of debate, the rules are now fixed. This is the first time SBTi has given carbon credits a defined role inside a corporate net-zero pathway.

And it comes with a twist. From 2027, every company has to declare publicly whether it is taking part. The companies that opt out are required to explain themselves.

That changes the conversation.

Below, I’ll break down what changed, the two new ways to use credits, how to act on Ongoing Emissions Responsibility, and a calculator that turns your own scope 1, 2 and 3 numbers into a budget.

P.S. I am doing a webinar on Friday, Jun 19th, 10:00 CEST where I am going to walk through the SBTi changes with Tobias Martetschlaeger, founder & CEO of Global Changer. Sign up for the webinar here →

What just changed

For years, the message was simple: cut first, think about credits somewhere near 2050.

V2.0 changes that. The new standard introduces Ongoing Emissions Responsibility (OER). It replaces the old Beyond Value Chain Mitigation concept and, for the first time, writes carbon credits into the standard with their own criteria, levels and reporting rules.

One thing to keep straight:

Credits still cannot count towards your scope 1, 2 or 3 targets. Those targets are still measured against your physical emissions inventory. Full stop.

What is new is that credits now have an official home alongside the target, not instead of it.

The two new ways to use credits

There are two routes, and they arrive on different timelines.

1. OER, from 2027

This is voluntary recognition for taking responsibility for the emissions you are still producing on the way down, not just the residual emissions left at the end.

OER can include reduction credits from outside your value chain, projects that protect or restore natural sinks, and removals.

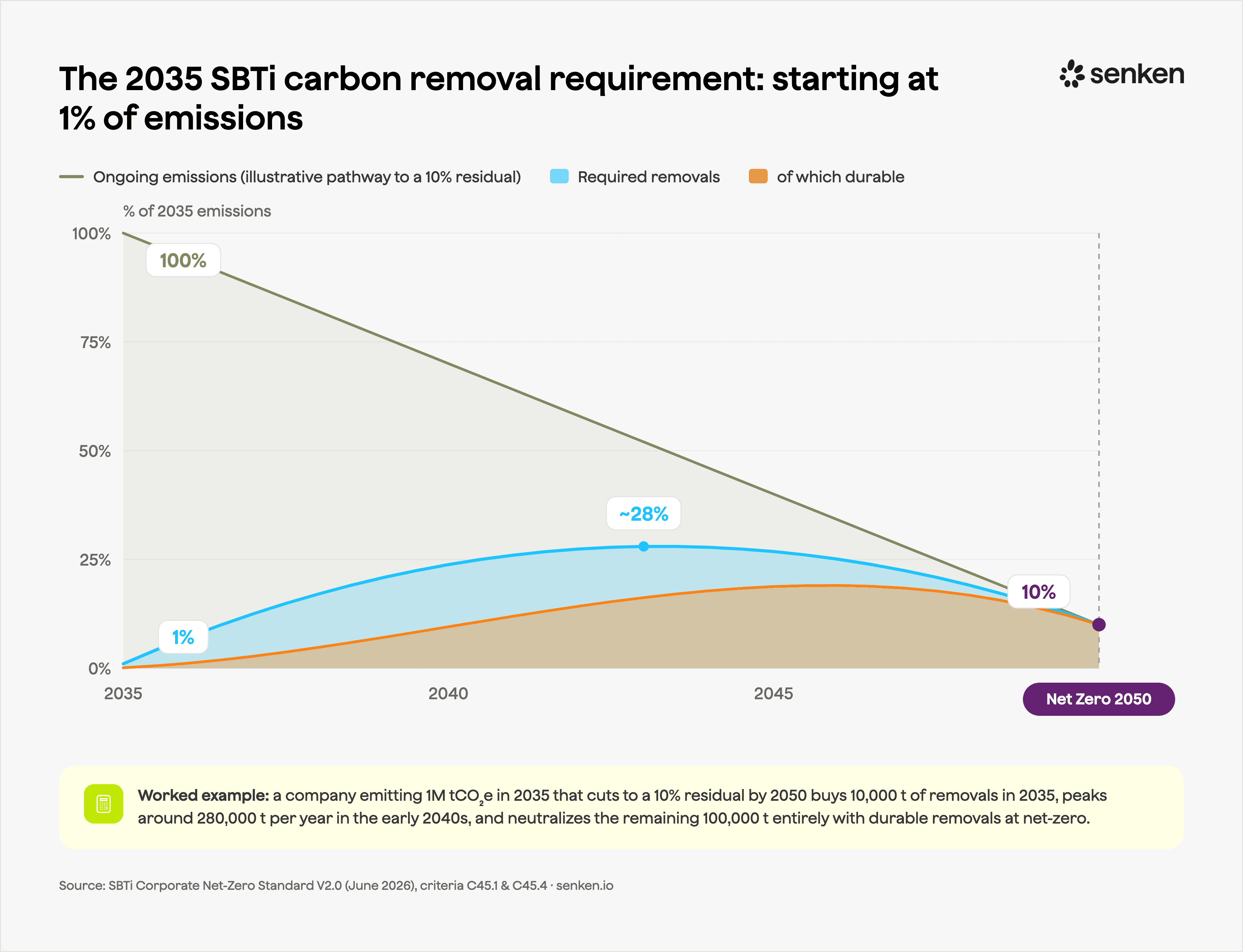

2. Mandatory removals, from 2035

For large companies, supporting carbon removals stops being optional from 2035. This applies to Category A companies, broadly those with turnover of €450 million or more, or 1,000+ employees.

Coverage starts at 1% of ongoing scope 1, 2 and 3 emissions in 2035 and rises in a straight line to 100% by your net-zero year, 2050 at the latest. This obligation is removals only. The durable share starts at 10% and also rises to 100% over the same period.

The 1% start is the smallest the obligation will ever be.

The part that changes the boardroom conversation

Participation in OER is voluntary. Taking a position is not.

From the first V2.0 validations in 2027, every company will state whether it is taking part. That answer will be published on the public SBTi Dashboard. If the answer is no, the company has to give SBTi a written explanation.

That inverts the old dynamic. Until now, the company buying credits was usually the one explaining itself. From 2027, the company not taking part is the one writing the explanation, in public, where customers, investors and procurement teams can read it.

That is the part I think many companies are still underestimating.

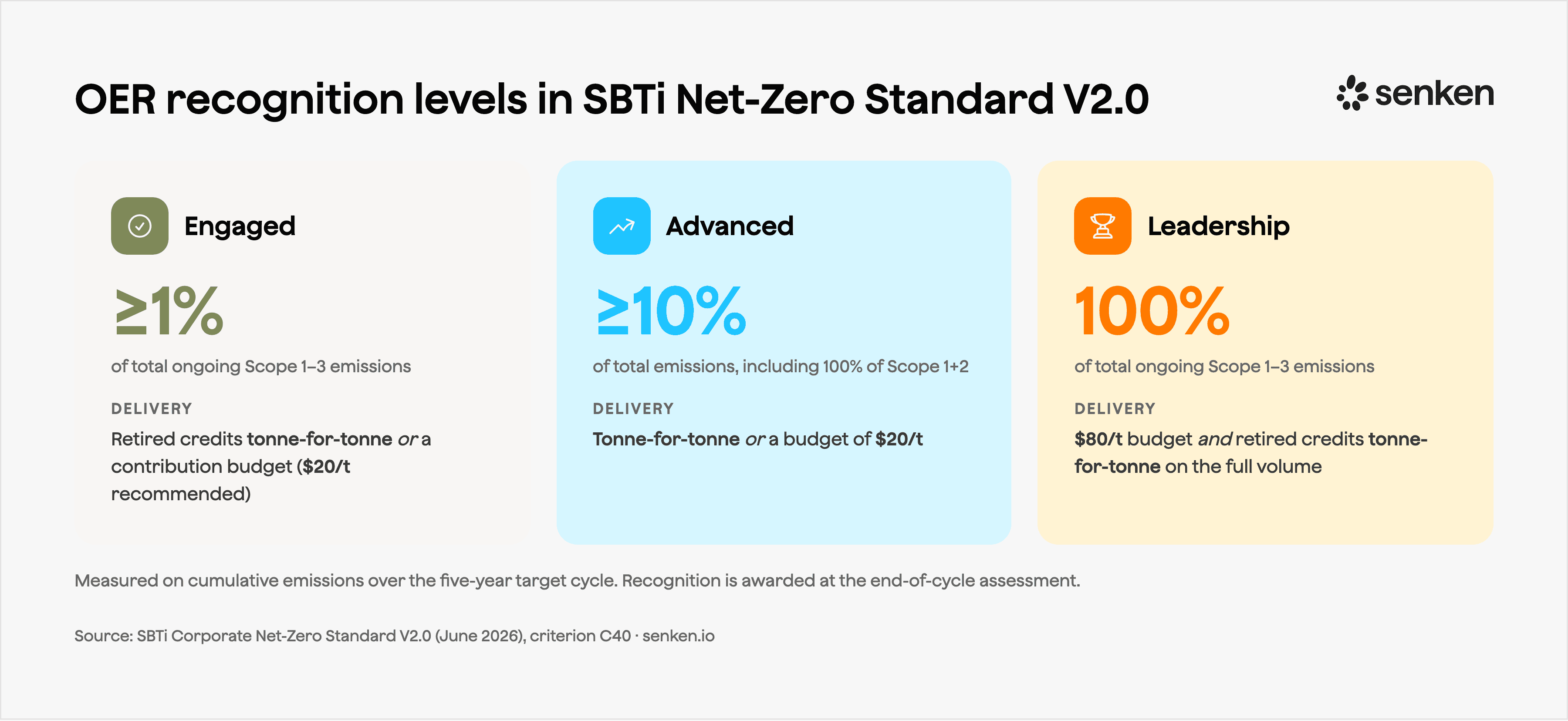

The three OER levels

All three OER levels are measured against your cumulative scope 1, 2 and 3 emissions over the five-year target cycle.

Cover at least 1% of total ongoing emissions, either with retired credits tonne for tonne or with a contribution budget. SBTi recommends at least $20 per tonne.

Advanced

Cover 100% of scope 1 and 2, plus at least 10% of total emissions, again either tonne for tonne or at $20 per tonne.

Leadership

Cover 100% of all ongoing emissions at $80 per tonne, and retire credits for the full volume. SBTi calls this the full internalisation of the cost of climate change.

One wall to respect in every report you publish: OER never reduces your reported footprint. Contributions are accounted for separately and cannot be netted against scope 1, 2 or 3.

How to act on OER

Here is the simple version.

1. Measure your base

Start with ongoing scope 1, 2 and 3 emissions, not just operations. The basis is cumulative emissions over your five-year cycle, so take a typical year and multiply it by five.

2. Pick your level

Engaged at 1% is deliberately accessible. Advanced and Leadership send a stronger signal.

3. Choose your route

You can retire credits tonne for tonne, or set a contribution budget at your chosen carbon price. The budget route is important because it lets forward removal agreements count.

4. Buy and retire high-integrity credits across the cycle

SBTi recommends progressive disbursement, not one purchase at the end. Quality is the constraint here. The integrity criteria are strict, so screen hard before you buy.

5. Declare and report

State your OER position at validation. That position becomes public on the SBTi Dashboard. Then report delivery. Recognition is awarded at the end-of-cycle assessment, and only to companies that are hitting their validated targets.

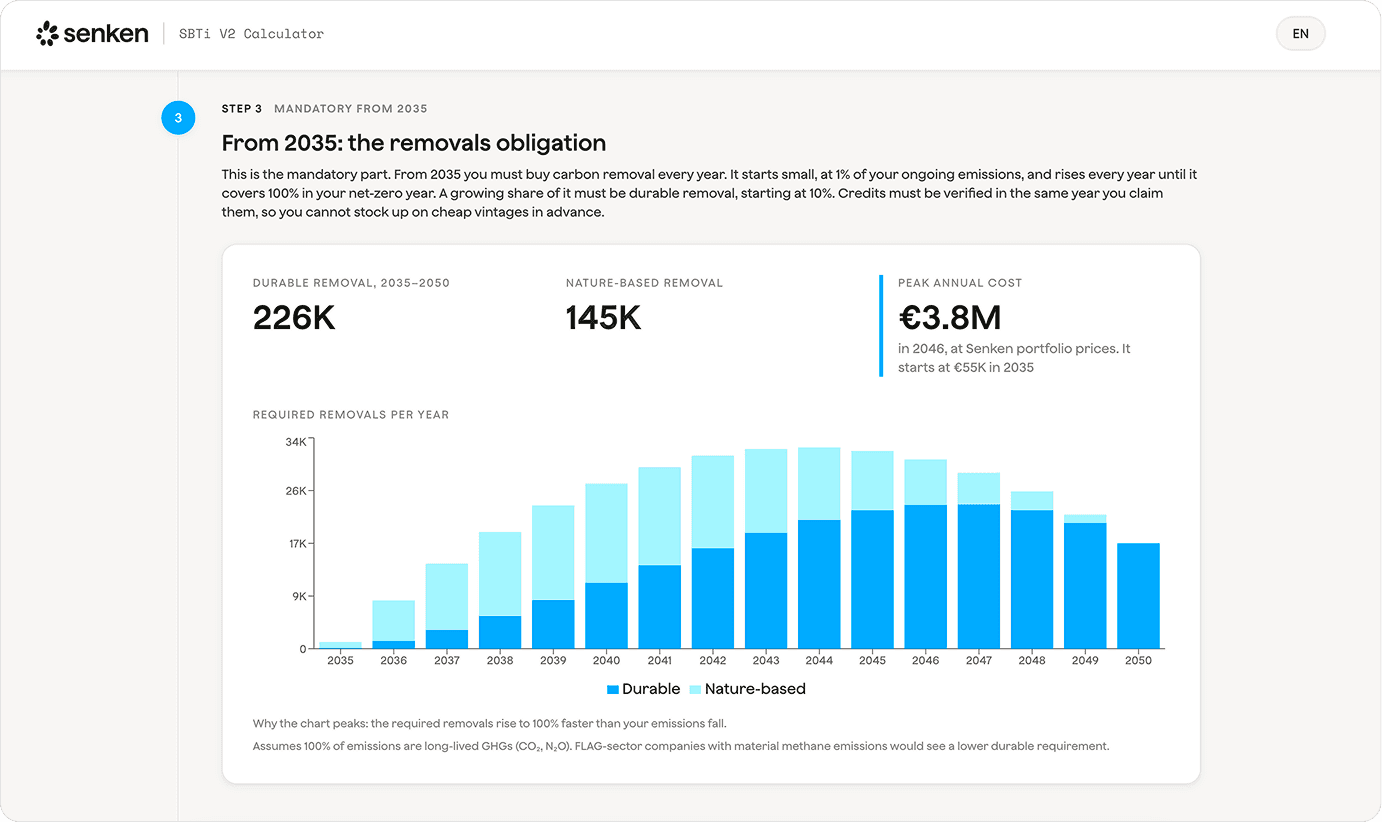

Calculate your own number

We built a calculator for exactly this. Put in your scope 1, 2 and 3 emissions and it returns all three OER levels and your budget, including the post-2035 removal ramp through to your net-zero year.

Open the SBTi V2.0 calculator →

One practical note on cost. High-quality removal supply, not demand, is the bottleneck. SBTi-driven demand could reach hundreds of millions of tonnes a year by 2035.

That is why forward delivery matters. Locking future supply through offtakes now is where the real discounts sit, before the ramp tightens the market. If you want the full picture in one place, here is our corporate guide to the standard.

Read the corporate guide to V2.0 →

Bottom line

SBTi has made carbon credits official, set a date when removals become mandatory, and made silence public.

The standard is final. The open question is whether you answer the 2027 declaration with a plan or with an explanation. The companies treating this as a planning problem now, not a scramble in 2035, will spend less and keep more options open.

If you want to integrate an OER strategy, or save on offtakes for 2035 and beyond, come talk to me. We’re happy to help — this is exactly what we specialise in.

One more thing: I’m running a webinar this Friday, 19 June at 10:00 CEST, on exactly what V2.0 changes for your carbon strategy.

Book a spot for Friday’s webinar

Thanks for reading,

Adrian

CEO & Co-Founder | Senken

📺 More from me on YouTube:

Would your CDR contract actually protect you?

Most removal contracts still leave buyers exposed. Here’s what stronger protection looks like, based on the Lufthansa deal.

Is Europe about to pull removals into the ETS?

CRCF, the EU Buyers Club and new ETS proposals are shifting the rules for CDR in Europe. Here’s what buyers should watch next.

Sources

- Corporate Net-Zero Standard V2.0 - SBTi

- What V2.0 changes for corporate carbon-credit strategy - Senken Blog

- Ongoing Emissions Responsibility (OER) explained - Senken Blog

- SBTi V2.0 OER calculator - Senken Tools

- Corporate guide to the SBTi Net-Zero Standard V2.0 - Senken

Information only. Not legal or investment advice.