Waiting until Q4 could cost you the best credits

Here’s what changed.

For years, buying carbon credits was a year-end chore. Total the footprint, go to market in Q4, buy spot, retire, repeat.

That model still works in some cases, but the centre of gravity has moved.

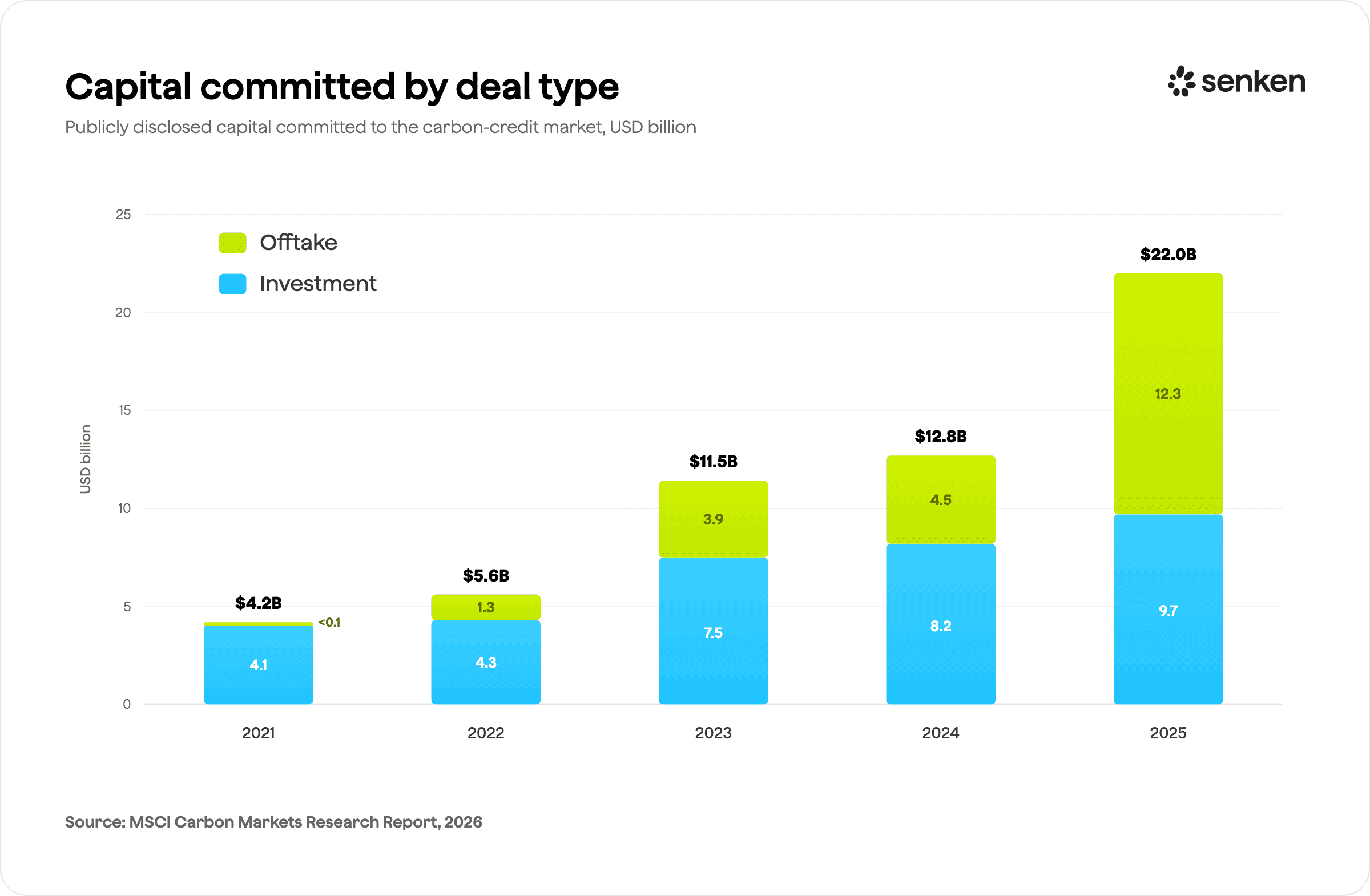

New MSCI data shows that serious buyers are increasingly moving earlier, locking in supply years ahead, and treating carbon credits more like strategic procurement than a last-minute annual purchase. In 2025, offtake commitments overtook direct project investment for the first time.

Below, I’ll break down what offtake actually means, why the new MSCI numbers matter, and how to decide when spot or offtake is the better fit.

The two ways to buy, in plain terms

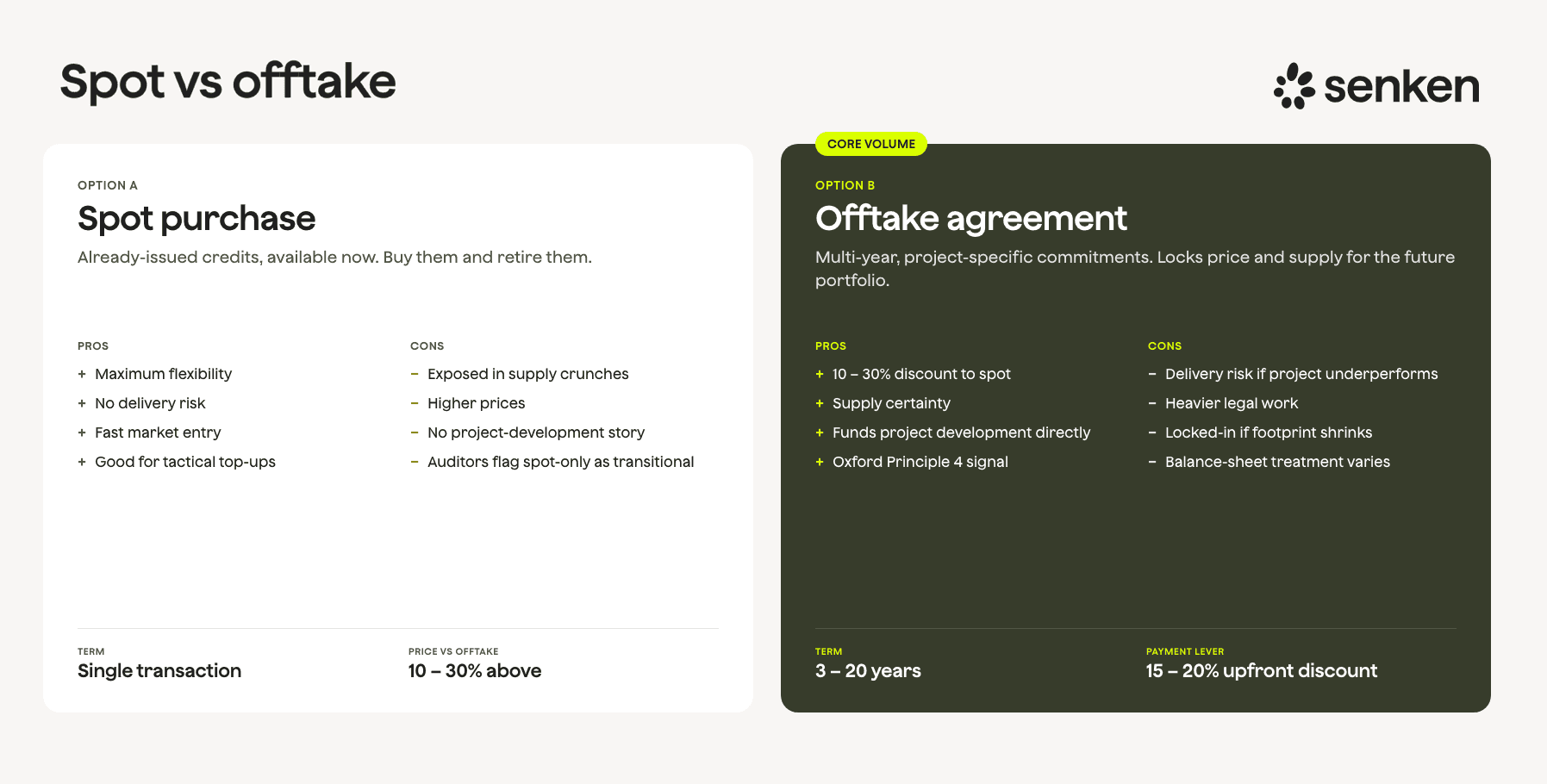

A spot transaction is what most people picture when they think about buying carbon credits.

You buy credits that already exist, take delivery now, and retire them against this year’s footprint. It is fast, flexible, and does not create a long-term commitment.

An offtake transaction is different.

You commit to buy a set volume from a project or portfolio over several years, often at a fixed or pre-agreed price. Credits are delivered as they are issued. Terms of three years or more are common, especially for removals.

Think of it as the carbon equivalent of a renewable energy Power Purchase Agreement.

What the latest MSCI data shows

MSCI’s latest analysis puts a number on the shift.

Capital committed and deployed into the carbon credit market reached $22 billion in 2025, a 72% increase on 2024 and more than five times the level of 2021.

But the split inside that figure is the real story.

Offtake agreements nearly tripled year on year to $12.3 billion and, for the first time, overtook direct project investment, which reached $9.7 billion.

Two more signals worth noting:

The trade-offs, honestly

Offtake is not automatically better than spot. It is a different risk profile.

What you gain with offtake:

- Price certainty. You lock in a cost today and protect against the quality premium widening further. MSCI’s spread between higher-rated and lower-rated credits reached over $17/t by end-2025, a premium of around 380%.

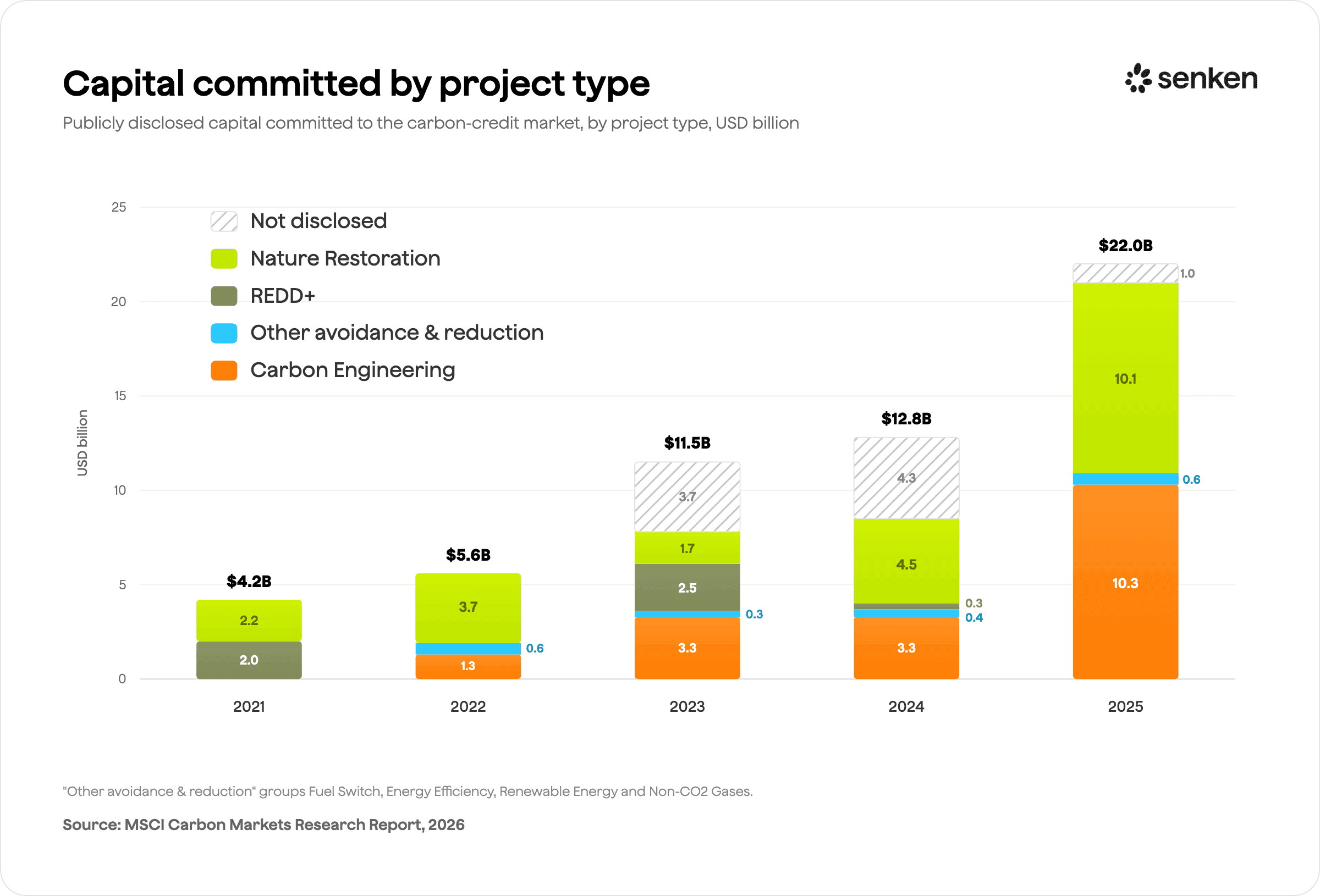

- Secured supply. You get first call on a high-quality stream for years. This matters most in tight segments like ARR and engineered removals, where only a fraction of credits reach BBB or above.

- Lower repeat diligence. Due diligence is done once, rather than starting again every year with annual spot buys.

What you take on:

- Delivery risk. Credits may underdeliver or arrive late because of developer insolvency, methodology issues, political risk, or lower-than-expected reductions. Good contracts can manage this with release clauses, but the risk is real.

- Capital and balance-sheet commitment. Multi-year volumes can mean many millions of tonnes and many millions of euros, sometimes with upfront pre-payment.

- Reduced flexibility. You are committed even if your footprint, strategy, or the science shifts.

(Some of these risks can be prevented with smart contracting.)

When offtake makes sense, and when it doesn’t

MSCI’s own conclusion is the honest one: offtake does not suit every buyer.

For smaller budgets, near-term obligations, or companies still building their strategy, spot still has a clear role. It gives immediate access to a wider range of credits without locking the buyer into a long-term commitment.

A practical way to think about it:

Year one: start with spot. It is the lower-risk way to enter the market, learn what quality looks like, and meet this year’s obligations without locking yourself in.

Year two onward, consider offtake for the predictable core of your demand. Once you know your residual emissions are durable and your strategy is set, forward-buying that baseline volume can give you better pricing, secured high-quality supply, and a steadier audit trail.

Keep spot for the flexible top layer.

In short: spot for flexibility and entry, offtake to steer a maturing strategy with less price risk.

Bottom line

A market where forward commitments outweigh immediate investment is a market planning ahead, not reacting late.

$22 billion in 2025, with offtake now the larger share, tells us that serious buyers have made a simple calculation: high-quality supply is finite, and target deadlines are fixed.

The gap is already visible.

Offtake commitments in 2025 were worth more than 12 times the credits retired in the spot market. That matters for everyone, not just large buyers.

More high-quality supply is being locked up years in advance. Less of it is reaching the spot market. So if you wait until year-end to buy, you are increasingly competing for what is left over. The best projects may already be spoken for.

If you bought spot this year, the question for next year is simple:

Which part of your demand is predictable enough to lock in, and which part should stay flexible?

Getting that split right is where price risk and audit-readiness are won or lost.

Thanks for reading,

Adrian

CEO & Co-Founder | Senken

📺 More from me on YouTube

Two recent videos worth a watch:

Microsoft, SBTi and EU CRCF: what buyers need to know

The week’s biggest carbon updates, translated into buyer takeaways.

What DAX40, CBAM and ratings reveal about carbon buying

Episode 1 of CWN covers the market signals buyers should be watching out for.

Sources

- Investment and Offtake Trends in the Global Carbon Credit Market - MSCI Carbon Markets Research Report April 2026

- USD 22 Billion Points to Future Carbon-Market Demand - MSCI Blog

- Nature-Based Offtake Deals: Something Is Stirring in Voluntary Carbon Markets - MSCI Blog

- Carbon Credits Come of Age in 2025 - MSCI Blog

Information only. Not legal or investment advice.