Carbon Credit Prices in 2026: What Companies Actually Pay

How much does a carbon credit cost in 2026?

In 2026, carbon credit prices range from €12 per tonne for REDD+ in the Brazilian Amazon to over €1,000 per tonne for direct air capture. A typical corporate buyer pays a blended portfolio average of €25 to €80 per tonne, depending on how much durable removal sits inside the portfolio.

The widely cited "$6.34 average" from the Ecosystem Marketplace State of the Voluntary Carbon Market 2025 is misleading for any company actually buying credits today. That figure is dragged down by legacy renewable-energy and avoidance credits that no longer pass quality screens. The prices below are what corporates in the DACH region pay for credits that meet ICVCM Core Carbon Principles, hold up to CSRD audit, and survive third-party rating reviews from Sylvera, BeZero, or Calyx.

The price points in this article come from Senken's internal data on the project developers in our supply network and the portfolios we have seen close in 2024 and 2025. Project names are not disclosed. Methodology and region are.

Carbon credit prices by methodology in 2026

| Methodology | Price range (€/tonne) | Removal type |

|---|---|---|

| Direct air capture | €450 to €1,000+ | Permanent removal |

| Enhanced rock weathering | €350 to €450 | Permanent removal |

| Microbial mineralisation | €170 to €200 | Permanent removal |

| Biochar | €105 to €200 | Permanent removal |

| Mangrove restoration | €50 to €75 | Temporary removal |

| ARR (afforestation, reforestation, revegetation) | €22 to €50 | Temporary removal |

| Regenerative agriculture | €15 to €60 | Temporary removal |

| Improved forest management | €25 to €30 | Avoidance |

| Peatland restoration | €17 to €90 | Avoidance |

| REDD+ | €12 to €15 | Avoidance |

Prices reflect 2024 and 2025 transaction data plus 2026 forward offers from project developers in Senken's vetted supply network.

Biochar carbon credit price: €105 to €200 per tonne

Industrial biochar is the most-bought permanent removal by volume in the portfolios we see. South American industrial biochar trades at €142 to €190, with the typical price clustering between €160 and €180. German biochar runs higher, in the €189 to €200 range, because of domestic origin premium and higher production costs. Indian biochar is the lowest-cost permanent removal we transact, with industrial-scale projects landing around €105 and artisanal at €120 to €150.

Biochar scales today, certifies under Verra, Puro, and the EU CRCF, and has permanence measured in centuries. The €100 spread within biochar reflects feedstock, region, and how much traceability the buyer needs for audit and reporting.

Regenerative agriculture price: €15 to €60 per tonne

Regenerative agriculture sits at the lower end of the temporary-removal tier. German projects sell at €49 to €60 per tonne. The same methodology in Scandinavia or the UK runs €18 to €55 depending on documentation tier. Indian regenerative agriculture is the lowest, at €15 to €27.

The 4x spread within one methodology comes from three things: where the soil is, who certifies it, and whether the project developer can supply the audit trail a CSRD reporter needs. German buyers consistently pay 2 to 3 times more for German-origin credits, even when the underlying methodology is identical to a project in Scandinavia. Domestic procurement is a stakeholder story as much as a climate story.

Peatland restoration price: €17 to €90 per tonne

Peatland restoration in Indonesia trades at €17 to €18 per tonne in our transactions, which makes it the lowest unit price for high-volume nature-based avoidance in our catalogue. German peatland restoration costs around €89 when bundled inside a Germany-only portfolio, again reflecting the domestic premium.

Peatland is a workhorse credit for portfolios that need real tonnage at a low blended price without dropping into the discredited generic-avoidance territory.

REDD+ price: €12 to €15 per tonne

REDD+ credits from the Brazilian Amazon trade at €12 to €15 per tonne for Verra-certified projects in our network. That sits well above the sub-$5 generic-avoidance prices reported in some market summaries, and below the €25 and above levels that high-integrity REDD+ commands when paired with strong co-benefits and updated baselines.

REDD+ remains controversial. It still appears in portfolios because demand for high-volume nature-based credits has not gone away, but every project in our supply gets re-screened against the latest ICVCM CCP assessments and third-party ratings.

Direct air capture, enhanced rock weathering, and microbial mineralisation: €170 to €1,000+ per tonne

The durable-removal tier covers methodologies with sequestration measured in centuries to millennia. Direct air capture sits at the top of the price range at €450 to over €1,000 per tonne. Enhanced rock weathering trades at €350 to €450 per tonne. Microbial mineralisation is the more accessible end of the durable tier at €170 to €200.

These methodologies show up in small allocations inside larger portfolios, usually 1 to 5 percent of total volume. Buyers use them to anchor a permanence story for SBTi or net-zero communications without inflating the blended portfolio price beyond what the budget allows.

ARR and mangrove restoration: €22 to €75 per tonne

Smallholder ARR in East Africa trades at €46 per tonne in our data, with the broader range running €22 to €50. Non-profit tree-planting in Germany comes in at €22, but those credits are typically not Verra-certified and serve a marketing-narrative role rather than a CSRD-grade reporting role.

Blue carbon mangrove restoration runs €50 in West Africa and €72 in Colombia. Volumes are limited, prices are climbing, and demand is currently outpacing supply for verified blue carbon in our pipeline.

What corporate carbon portfolios actually cost in 2026

The single-project unit price is rarely the number a sustainability lead actually budgets against. The number that matters is the blended portfolio price, including service fees, after the methodology mix is set.

Based on Senken's internal data, the blended portfolio price varies less by company size and more by industry sector and climate strategy. Following the Oxford Principles for Net Zero Aligned Carbon Offsetting, every credible portfolio needs a mix of avoidance, short-lived removals (regenerative agriculture, ARR, peatland), and long-lived durable removals (biochar, ERW, DAC, BECCS). The portion of long-lived storage has to grow over time as the company moves toward its net-zero target year. What changes by sector is the share each layer takes today.

Advanced technology and AI: €200 and above per tonne

Hyperscalers and frontier-tech companies (Microsoft, Google, Stripe, Frontier coalition members) anchor their portfolios in the most expensive durable removals on the market: direct air capture, BECCS, mineralisation, and ERW. These companies are willing to pay €450 and above per tonne for permanence, often through long-term offtake agreements that fund first-of-a-kind facilities. They typically pair the durable layer with smaller allocations of nature-based removal, landing on a blended portfolio price north of €200 per tonne. The strategy is explicit: catalyse the durable-removal supply chain that everyone else will eventually need.

High-margin services: €80 and above per tonne

Software, financial services, professional services, and consultancies tend to land in the €80 to €150 per tonne range. These sectors have small physical footprints relative to revenue, so paying €100 per tonne to retire a few thousand credits is affordable and signals genuine ambition. The typical mix is regenerative agriculture and peatland for the avoidance and short-lived removal layer, biochar for the durable removal layer at 20 to 40 percent of volume, and a small allocation of DAC or ERW (1 to 5 percent) to align with Oxford Principles on long-lived storage.

Heavy emitters: €30 to €50 per tonne

Industrial manufacturers, utilities, transport, and other hard-to-abate sectors with large absolute footprints prefer cheaper portfolios while staying inside the high-integrity boundary. Blended prices land at €30 to €50 per tonne. The mix is heavy on Indonesian peatland and African ARR for tonnage, supplemented by Indian or Scandinavian regenerative agriculture, and a smaller share of biochar (5 to 15 percent) to start building the durable layer the Oxford Principles require. The total bill is large because the volume is large, but the per-tonne price stays disciplined.

Consumer brands and retail: €50 and above per tonne

Consumer-facing brands, especially those offering an opt-in climate contribution at checkout, tend to budget €50 and above per tonne. The premium funds a stronger story: more recognisable methodologies, project-level traceability, biodiversity co-benefits, and sometimes a small biochar or DAC allocation that customers can see on the impact page. Many consumer brands pass some or all of the cost to the end customer through a small surcharge or a flat percentage on top of the basket value.

"When a sustainability lead asks me what carbon credits cost, the honest answer is: it depends entirely on what mix you can defend to your auditor and your CFO. The Oxford Principles are clear that every credible portfolio has to include some durable removal today, even if it is a small share, and shift toward long-lived storage over time. We have seen software companies blend up to €150 per tonne and heavy emitters land at €35. Both are correct for their company. The expensive ones bought permanence early; the disciplined ones bought tonnage and started building the removal layer."

Adrian Wons, CEO, Senken

Why carbon credit prices vary 30x within the voluntary market

Five drivers explain almost all of the price variation in our data.

1. Removal vs avoidance

Permanent removals (DAC, ERW, biochar) cost 10 to 80 times more than avoidance (REDD+, peatland). The cheapest avoidance credit we transact sits at €12 and the most expensive durable removal sits above €1,000. That is an 80x spread inside the same legal market, driven entirely by the durability of the storage.

2. Region of origin

German credits trade at a 2x to 3x premium over identical methodologies in lower-cost geographies. German biochar at €189 to €200 versus Indian biochar at €105. German regenerative agriculture at €49 to €60 versus Indian regenerative agriculture at €15 to €27. The premium is real and reflects genuine procurement preference, not just transport cost.

3. Vintage

Recent vintages (2023 and newer) command 20 to 40 percent more than 2018 to 2020 vintages of the same methodology. Older vintages were verified under earlier standards and many have been delisted by ratings agencies. We rarely transact pre-2020 vintages anymore.

4. Certification and rating tier

Verra and Gold Standard certification are the floor. The premium tier is ICVCM Core Carbon Principles approval plus a third-party rating from Sylvera, BeZero, or Calyx in the A-band. This combination adds €5 to €15 per tonne and is increasingly required for CSRD reporting.

5. Co-benefits and SDG alignment

Co-benefits (biodiversity, smallholder income, water quality) add €5 to €20 per tonne in our pricing. This is the easiest premium to justify in stakeholder communication, and the hardest to fake in a CSRD assurance review.

Compliance carbon market prices in 2026

The compliance market operates separately from the voluntary market, and prices are set by allowance auctions rather than project economics.

| System | 2025 range | Early 2026 level |

|---|---|---|

| EU ETS | €60 to €80 | €75 to €90 |

| UK ETS | £41 to £52 | £45 to £55 |

| California–Québec | $25 to $29 | $27 to $32 |

| Washington State | $50 to $64 | $55 to $65 |

| RGGI | $22 | $20 to $25 |

| CORSIA-eligible (aviation) | ~€19 | ~€20 |

EU ETS allowances are the global benchmark. Analyst projections see EU ETS averaging €91 to €93 per tonne in 2026, climbing toward €130 and above by 2030 as the cap tightens and the market stabilisation reserve absorbs supply.

Compliance prices are not interchangeable with voluntary prices. EU ETS allowances cannot be used to retire against a voluntary net-zero claim, and vice versa. The two markets co-exist with different buyers, different intermediaries, and different price signals.

What you should budget for carbon credits in 2026

Use these blended price assumptions for 2026 budget planning, derived from Senken's internal portfolio data.

Carbon-neutral portfolio: €25 to €80 per tonne

Mostly nature-based avoidance and short-lived removal (peatland, REDD+, regenerative agriculture, ARR), with a small durable-removal allocation to satisfy the Oxford Principles direction of travel. Defensible if every credit is CCP-approved and rated. Acceptable for marketing claims that comply with the Empowering Consumer Directive and the Green Claims Directive.

SBTi-aligned net-zero portfolio: €60 to €220 per tonne

The blended price climbs because durable removal moves from a token allocation to a meaningful share, often 30 to 50 percent of volume by 2030. Biochar at €105 to €200 carries most of the durable layer, with smaller allocations of ERW and DAC anchoring the long-lived storage tier the Oxford Principles ask for. The high end of the range reflects companies that front-load DAC and ERW today rather than wait for prices to compress.

Heavy-emitter portfolio: €25 to €50 per tonne

Industrial sectors with very large absolute footprints buy in volume and stay disciplined on per-tonne price. The total budget is still significant in absolute terms because the volume runs into hundreds of thousands of tonnes per year. The mix prioritises high-integrity nature-based credits (Indonesian peatland, East African ARR) and pairs them with a growing biochar share to satisfy Oxford Principles requirements without breaking the per-tonne ceiling.

For the full step-by-step on calculating your number, see how to determine your carbon credit budget and how to plan for procurement of carbon credits.

Carbon credit price forecast 2026 to 2030

Three forecasts converge on the same direction even though they disagree on speed.

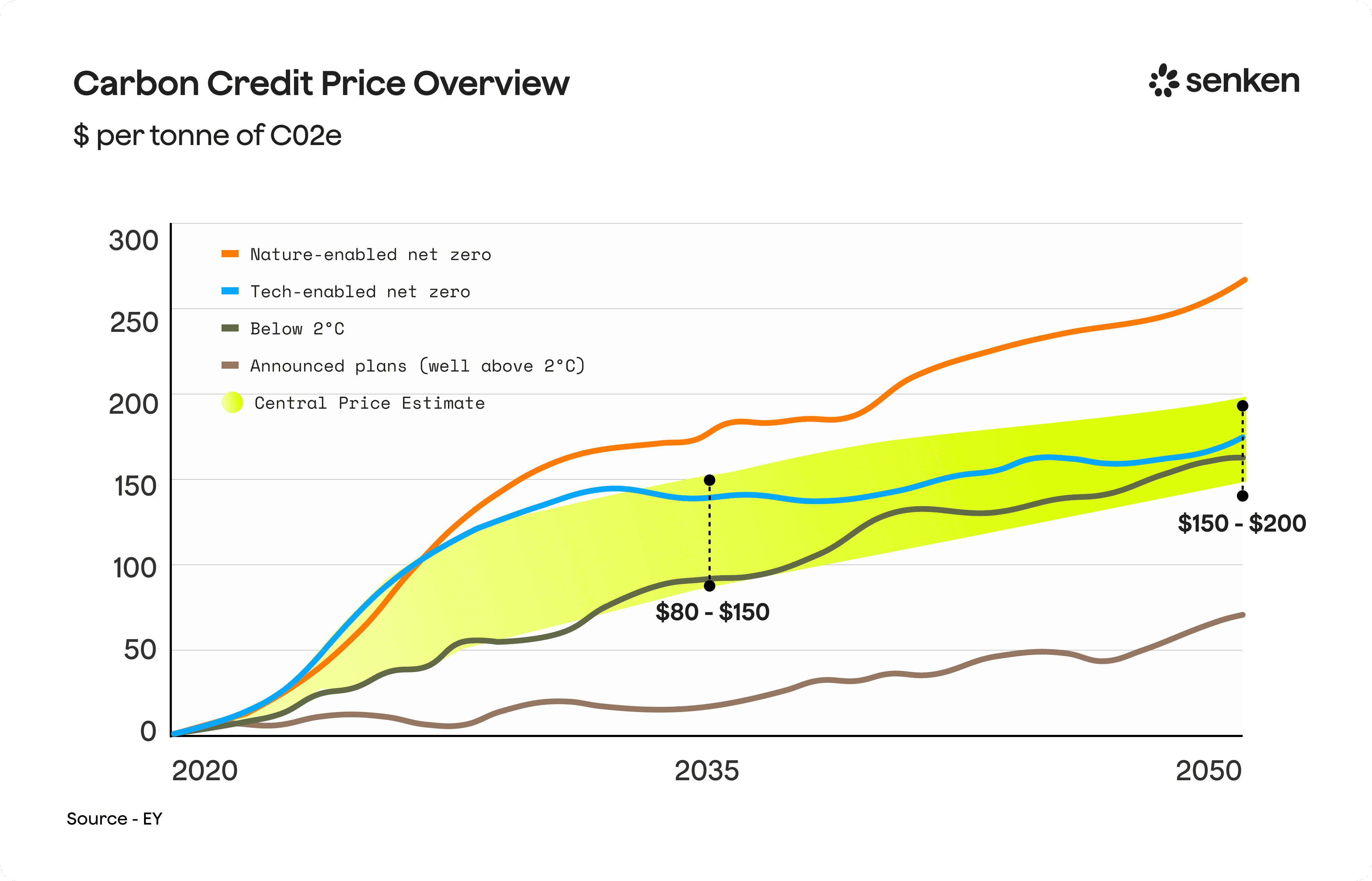

- EY Net Zero Centre: $75 to $125 per tonne by 2035, rising to $125 to $175 by 2050. Roughly 30 to 50 percent of credits on the market will cost more than $50 per tonne by 2035.

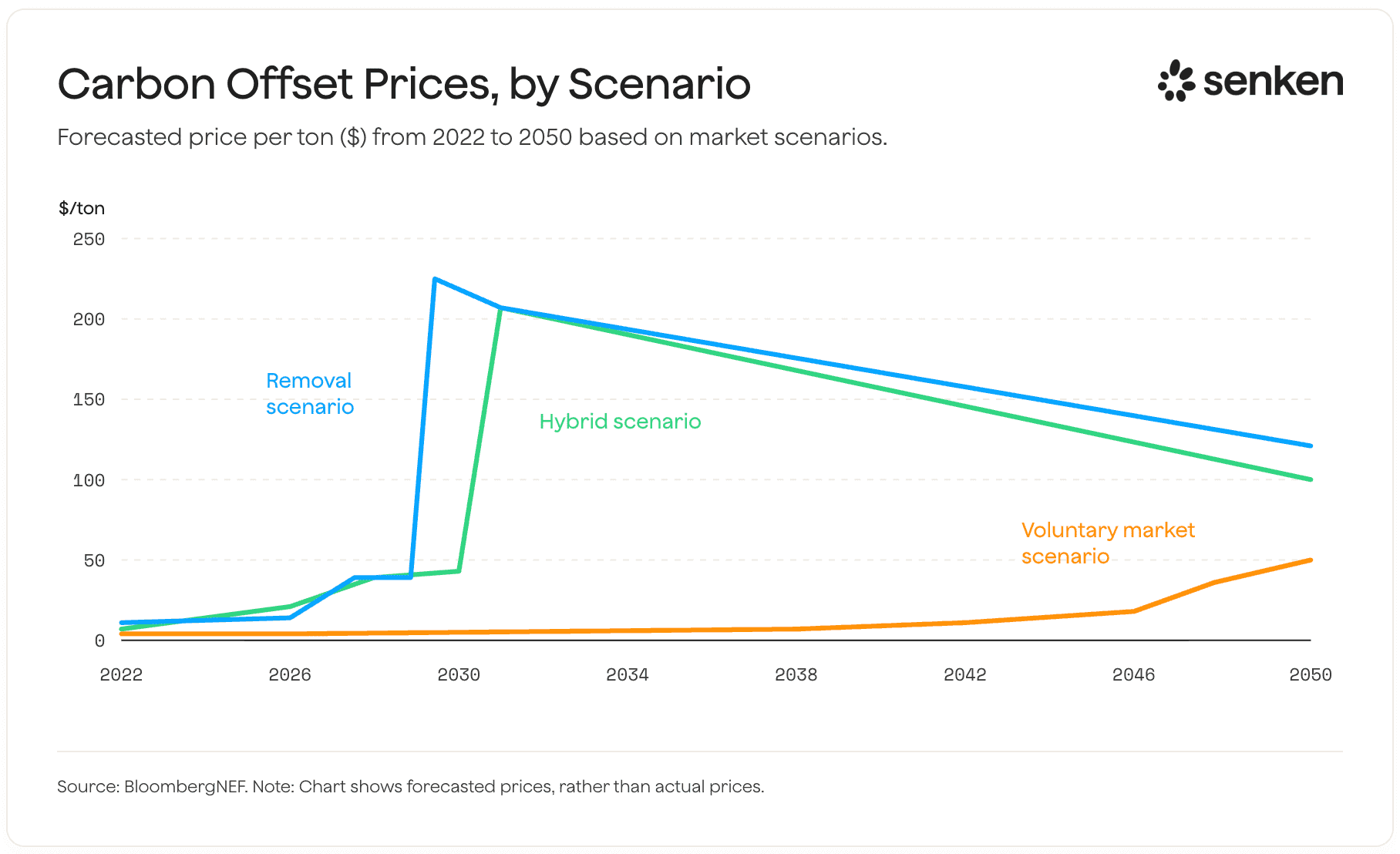

- BloombergNEF removal-led scenario: $42 per tonne in 2030, $105 in 2032, $254 in 2037. Driven by net-zero buyers shifting from avoidance to removal.

- BloombergNEF voluntary status-quo scenario: Only $13 per tonne in 2030, $35 in 2050. This scenario assumes the integrity flight stalls.

Senken's view, based on developer offers in our 2026 pipeline:

- Biochar prices will hold at €100 to €200 per tonne through 2027, then trend upward as demand from SBTi-aligned buyers absorbs near-term supply.

- ERW and DAC will compress slightly as more projects come online, but stay above €250 per tonne through 2030.

- Nature-based avoidance below €15 per tonne will continue to disappear from buyer-grade portfolios as ICVCM CCP filtering tightens.

- The blended price for a credible corporate portfolio will move from today's €40 to €60 toward €60 to €90 by 2028.

Why a higher carbon credit price usually does mean better quality

The cheapest credits available carry the highest reputational risk. Generic avoidance credits trading under €5 per tonne fail ICVCM screens, struggle in third-party ratings, and rarely survive a CSRD assurance review. Buying them to reduce average portfolio cost can cost more in retraction risk than the savings are worth.

That does not mean price is a clean quality proxy. A €400 enhanced rock weathering credit is not necessarily a better climate investment than a €50 mangrove credit, because the two answer different questions. The right test is methodology-specific quality: methodology rigour, MRV transparency, additionality, permanence, and verified co-benefits.

For the deeper framework, see carbon credit quality.

Why public market data understates real corporate prices

The carbon market is still remarkably opaque. Most public price benchmarks aggregate every transaction in a registry, including legacy renewable-energy credits, pre-2020 vintages, and methodologies that no credible buyer would touch in 2026. The headline averages bear little resemblance to what a corporate sustainability lead actually pays for an audit-ready portfolio.

A 2024 meta-study by Dr. Benedict Probst at the Max Planck Institute, published in Nature Communications, reviewed 14 studies covering 2,346 climate projects (around one billion tonnes of issued credits) and found that less than 16 percent of carbon credits issued represented genuine emissions reductions. The remaining 84 percent failed on additionality, baseline inflation, leakage, or permanence. Those low-quality credits still trade and still appear in registry-wide averages, which is one reason the public benchmarks come in so low.

The credits that corporates actually buy in 2026 are a much smaller, more selective pool. Compare the public benchmarks to what shows up inside Senken-supplied portfolios:

- Ecosystem Marketplace 2025 average: $6.34 per tonne. Includes legacy renewable-energy and pre-2020 avoidance credits. No CSRD reporter is buying at this price.

- Allied Offsets average voluntary price: $5 to $10 per tonne. Same methodology issue, heavily weighted by historical low-integrity transactions.

- Senken closed-portfolio blended average 2024 to 2025: €25 to €80 per tonne. Reflects current corporate buyers in DACH paying for ICVCM-screened, Verra/Gold Standard/Puro-certified credits, with growing durable-removal allocations following the Oxford Principles.

The gap is not market disagreement. It is the difference between what is technically a tradable carbon credit and what is an audit-ready, communications-defensible carbon credit in 2026.

For the corporate-side view of how this opacity plays out in real disclosures, see Senken's Buying Blind: Analysis of DAX40 FY2025 CSRD Carbon Credit Disclosures.