Double Materiality Assessment

Key Takeaways

- Your double materiality assessment is the gateway to CSRD compliance—it determines which ESRS topics and datapoints you must report, so invest in a clear, documented methodology from day one, not just a pretty matrix for the sustainability report.

- For large EU companies, expect your first double materiality assessment to take 2–6 months and require input from at least eight business functions—sustainability, finance, risk, operations, procurement, HR, legal, and IT—with Board-level sign-off to ensure the process stands up to audit.

- A practical five-step framework—define scope and boundaries, identify IROs across your value chain, engage stakeholders with structured evidence gathering, score impact and financial materiality using defensible rubrics, then validate and document—turns ESRS theory into a repeatable workflow you can embed in annual planning.

- Climate change (ESRS E1), own workforce (S1), and value chain workers (S2) are almost universally material across sectors, which means your double materiality assessment should directly inform Scope 3 prioritisation, decarbonisation roadmaps, and—where residual emissions remain—your approach to high-integrity carbon credits that won't trigger greenwashing risk.

Double materiality assessment under CSRD

A double materiality assessment under CSRD is your gateway to the European Sustainability Reporting Standards. It determines which sustainability topics and datapoints you must report and which will be examined under assurance. Simply put, this assessment decides the scope of your entire CSRD disclosure programme.

At its core, double materiality asks you to look through two lenses. Impact materiality examines how your business affects people and the environment across your operations and value chain, both positively and negatively. Think inside-out: what actual or potential impacts does your company create over the short, medium and long term? Financial materiality flips the perspective, examining how sustainability matters could trigger material financial effects on your development, financial position, performance, cash flows, access to finance or cost of capital. This is the outside-in view.

Both lenses work through what ESRS calls impacts, risks and opportunities (IROs). Impacts are the sustainability-related effects your business creates or contributes to. Risks and opportunities are the financial consequences that sustainability matters, including dependencies on natural, human and social resources, might have on your company. A topic can be material from one lens, both lenses or neither.

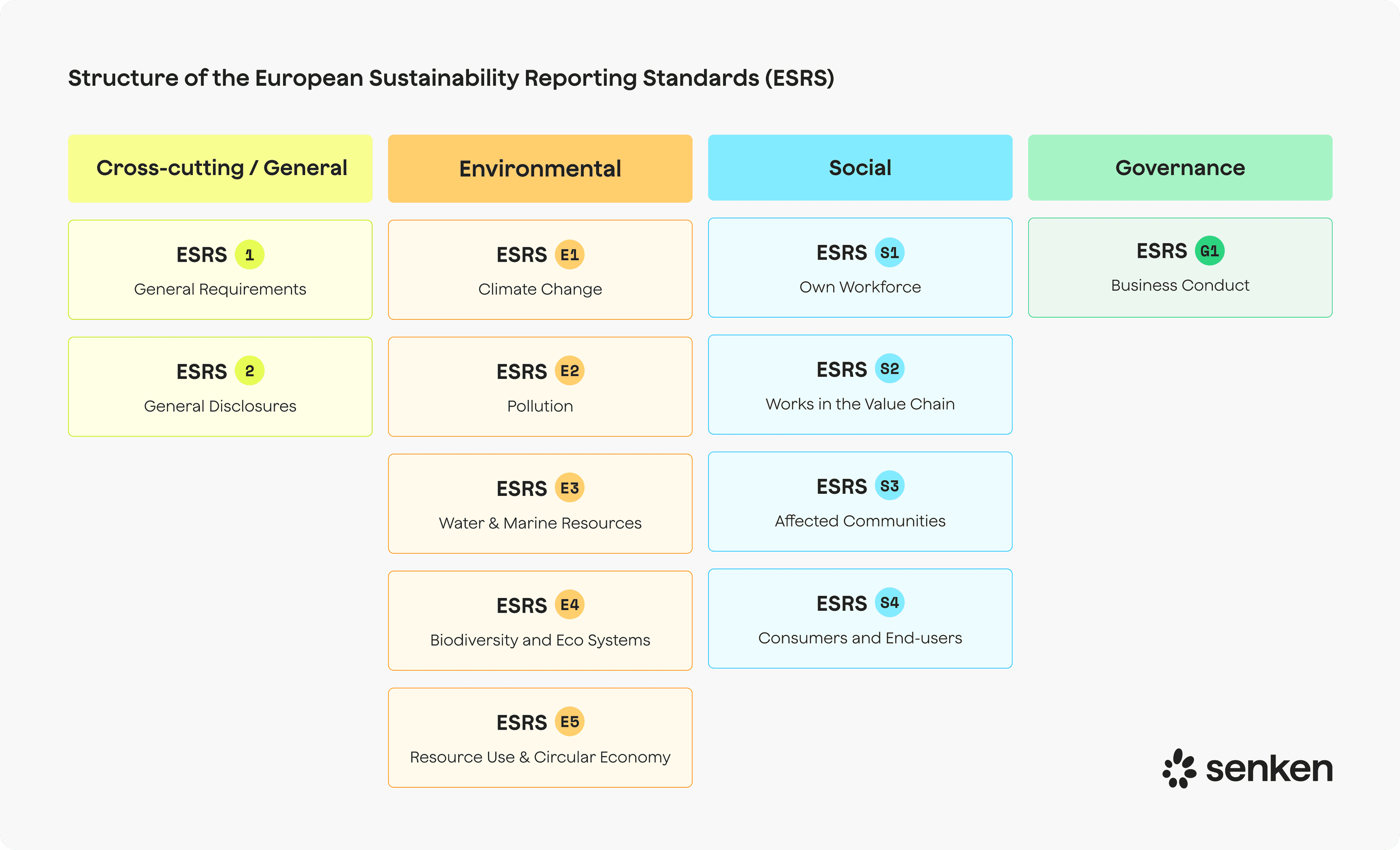

Your double materiality assessment must cover your full value chain, including upstream suppliers and downstream activities, and consider three standardised time horizons: short-term (the reporting period), medium-term (up to five years) and long-term (beyond five years). The outcome directly shapes which of the topical ESRS standards (E1 Climate, S1 Own Workforce, G1 Governance, and so on) you report against and which datapoints within those standards are mandatory or voluntary for you.

Here's what matters most: your assessment will be subject to limited assurance initially, moving to reasonable assurance after 2028. Auditors will expect a documented methodology, clear thresholds, traceable decisions and evidence that you've genuinely engaged with the process, not simply filled in a template. Getting the design right from day one saves rework and protects you from audit challenges later.

Designing your double materiality assessment: scope, governance and realistic timelines

Before you dive into scoring and matrices, get the scaffolding right. Define your reporting boundary by aligning with the entities included in your financial consolidation under CSRD. If you're a large EU group with multiple subsidiaries and joint ventures, clarify early which legal entities sit inside the assessment and which sit just outside but might still contribute value chain IROs.

Value chain coverage is where things get real. ESRS expects you to consider material impacts, risks and opportunities connected through your direct and indirect business relationships, both upstream (suppliers, raw materials, logistics) and downstream (distribution, product use, end-of-life). You don't need to map every supplier or customer on day one, but you do need a defensible method for identifying hotspots. Use spend data, sectoral studies, prior risk assessments and peer benchmarks to focus your effort where it will count.

Governance makes or breaks your double materiality assessment. Set up a core team with clear ownership: sustainability as the orchestrator, finance and risk co-owning financial materiality, and subject-matter experts from operations, procurement, HR, legal and communications feeding in topic-specific input. Appoint an executive sponsor, ideally the CFO or CSO, and plan at least two touchpoints with the Board or Audit Committee to validate scope, review draft results and approve the final outcome.

For timelines, expect a first-time double materiality assessment to take between two and six months, depending on your size, complexity and data maturity. A manufacturing group with a global supply chain and limited ESG infrastructure will sit at the longer end; a services business with strong existing risk management and prior GRI reporting can move faster. Typical phases look like this: one to two weeks for scoping and kick-off, four to six weeks for IRO identification and stakeholder engagement, two to four weeks for scoring and validation, and two weeks for documentation and sign-off. If you're starting late in your CSRD cycle, prioritise governance, stakeholder mapping and scoring methodology over perfecting every data point. You can refine in year two.

Recent surveys show only about a third of in-scope companies had completed their double materiality assessment by late 2024. If you're behind, you're not alone, but the clock is ticking.

A 5-step process to run a robust double materiality assessment

Step 1: Define scope, boundaries and time horizons

Start with clarity. Document which legal entities are in scope, which value chain tiers you will assess (typically tier 1 suppliers as a minimum, extending deeper for high-risk categories), and how you define short, medium and long-term for your business context. Confirm these boundaries with finance and legal to ensure consistency with financial reporting and enterprise risk processes. This step also includes gathering existing data: your GHG inventory, risk registers, supplier lists, materiality matrices from prior GRI or investor ESG work, and any relevant sector studies or peer disclosures. Output: a scoping memo and data inventory that your assurance provider can review.

Step 2: Map activities and build your longlist of IROs

Identify your business activities (what you do, where, and with whom) and use them to generate a longlist of potential sustainability matters and associated IROs. Start with the full universe of ESRS topical standards as a checklist, then layer in sector-specific issues (for example, water use in beverage manufacturing, data privacy in tech, fair wages in apparel supply chains) and stakeholder concerns from past engagement. Cross-reference your enterprise risk register and recent regulatory, reputational or operational incidents. Don't self-censor at this stage; it's easier to filter a long list than to add back forgotten topics later. Output: a structured IRO register with each item tagged to ESRS topic, value chain stage, and time horizon.

Step 3: Engage stakeholders and gather evidence

ESRS requires you to engage affected stakeholders to inform your severity and likelihood assessments. Affected stakeholders include your own workforce, workers in your value chain, communities near your sites or supply chain, and customers where relevant. For large companies, this typically means a mix of internal workshops (HR, operations, procurement), external interviews or surveys (key suppliers, community representatives, NGOs, trade unions), and desk research (academic studies, NGO reports, media coverage, peer CSRD disclosures). Keep it pragmatic: aim for 8 to 15 substantive engagements rather than a 500-respondent survey. Document who you engaged, how, when and what you learned. This evidence will feed directly into your scoring in Step 4 and will be one of the first things auditors ask to see.

Step 4: Score impact and financial materiality with a clear rubric

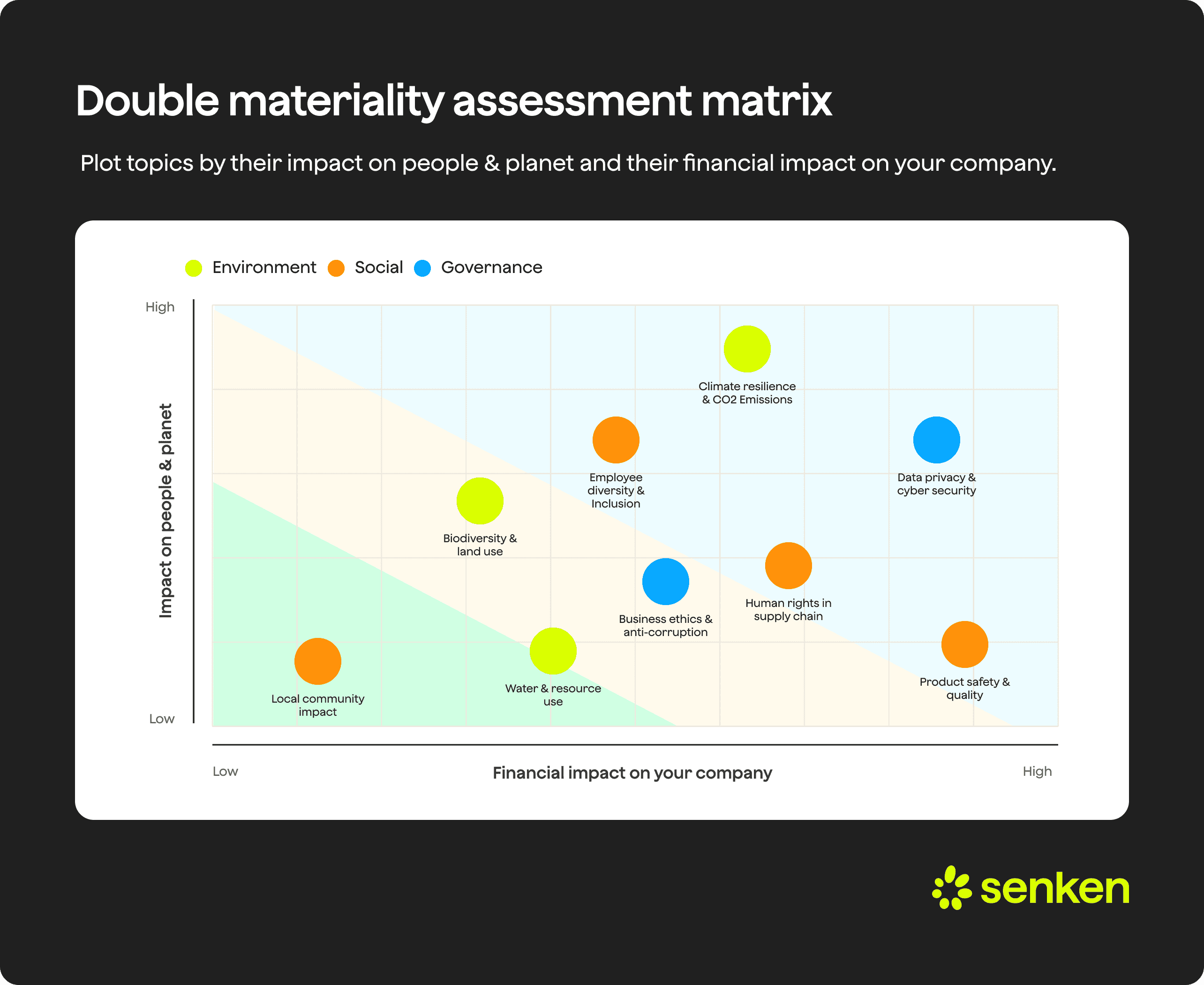

This is the analytical heart of your double materiality assessment. For impact materiality, score each IRO across four dimensions: scale (how severe is the impact?), scope (how widespread?), irremediability (can it be reversed or remediated?) and likelihood. Use a consistent scale, typically 1 to 4 or 1 to 5, and define each level with examples relevant to your business. Combine the four scores into a composite impact materiality rating (for example, by multiplying severity, which itself combines scale, scope and irremediability, by likelihood).

For financial materiality, assess magnitude of potential financial effect, likelihood of occurrence, and time horizon. Magnitude should align with your financial reporting thresholds (for instance, could this reasonably affect revenue, EBITDA or enterprise value by more than X%?). Likelihood asks: how probable is this effect? Time horizon gives more weight to near-term impacts but doesn't ignore long-term systemic risks like physical climate impacts or regulatory shifts.

Plot your scores on a two-axis matrix (impact materiality on Y, financial materiality on X) and set a clear threshold for what counts as "material." Many companies use a quadrant approach: anything above a certain score on either axis (or both) crosses the line. A worked example: value chain GHG emissions in a logistics company might score high on scale (contributes significantly to climate change), high on scope (affects global climate system), medium on irremediability (emissions are long-lived but removals exist) and high on likelihood (already happening). On financial materiality, the same IRO scores high on magnitude (carbon pricing, fuel costs, customer requirements for low-carbon transport) and high on likelihood, especially in the medium term. Result: clearly material under both lenses, so ESRS E1 becomes mandatory and detailed Scope 3 disclosure is required.

Step 5: Validate, document and finalise your material topics

Take your draft material topics back to your cross-functional working group and executive sponsor for challenge and validation. Ask: does this list make strategic sense? Are we missing anything obvious? Are we over- or under-rotating on certain themes? Once validated internally, document your full methodology (definitions, scoring scales, thresholds, data sources, stakeholder engagement summary) in a single materiality assessment methodology paper that will sit as an appendix to your sustainability statement. Map each material topic to the relevant ESRS disclosure requirements and confirm which datapoints are now mandatory for you. Get formal sign-off from the Board or Audit Committee, and schedule the first refresh cycle (typically every two to three years or sooner if there's a significant change in your business model or external environment).

Making your double materiality assessment audit-ready and repeatable

Auditors providing limited assurance on your CSRD reporting will examine whether you have complied with ESRS, including whether your materiality assessment methodology is sound, transparent and consistently applied. Expect them to ask: How did you set your thresholds? Can you show me the data and stakeholder input behind this scoring decision? Where is the audit trail from IRO identification to final topic selection? How did the Board review and approve this?

To be ready, maintain a central evidence repository for your double materiality assessment. At minimum, it should contain: your scoping and boundary memo; the full IRO register with scores and data sources noted; records of stakeholder engagement (meeting notes, interview transcripts, survey results); the methodology paper with scoring rubrics and thresholds; internal validation workshops and executive review meeting minutes; the final materiality matrix with mapping to ESRS; and the Board sign-off document. Treat this like a financial audit file: structured, version-controlled and accessible.

Controls matter too. Separate the roles of data provider, scorer and reviewer. For example, HR provides workforce data, the core DMA team scores the IRO, and finance or internal audit reviews for consistency with financial materiality thresholds. Document assumptions and use of estimates transparently. If you've used sector-average emissions data because primary supplier data isn't available, say so and note your plan to improve data quality.

Finally, make your assessment repeatable. Don't rebuild from scratch each cycle. Store your scoring rubrics, threshold definitions and IRO register in a format that can be updated with new data, refreshed stakeholder input and changes in regulation or strategy. Link the DMA to your existing enterprise risk management cycle so that new risks or incidents automatically prompt a materiality review. Many companies are integrating materiality into their annual internal control and risk reporting process, with a formal refresh every two to three years and a lighter update annually. This turns a compliance burden into a strategic planning asset.

Using DMA outcomes to drive climate strategy, Scope 3 and high-integrity carbon credits

Here's the reality: if you run a robust double materiality assessment in a large EU company, climate change and value chain emissions will almost certainly come out as highly material on both lenses. Sectoral evidence from early CSRD reporters shows that ESRS E1 (Climate Change) is disclosed as material by nearly every company, alongside ESRS S1 (Own Workforce) and S2 (Workers in the Value Chain). Climate isn't a nice-to-have; it's the presumptive baseline for your sustainability strategy and disclosure.

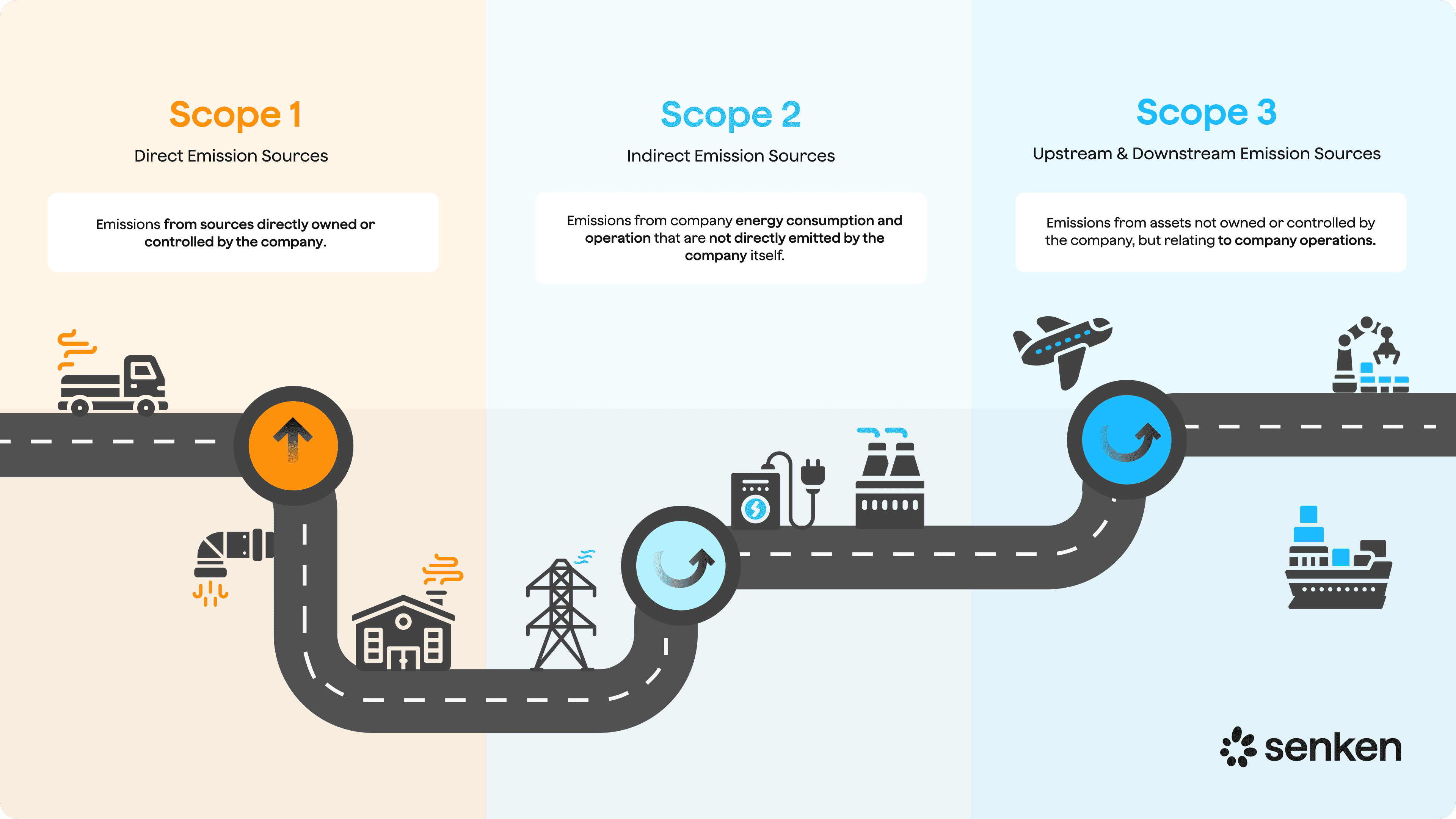

Once climate and Scope 3 are confirmed as material, your double materiality assessment tells you where to focus. Use your IRO scoring to identify Scope 3 hotspots: which categories (purchased goods, upstream transport, use of sold products, end-of-life) scored high on impact and financial materiality? Prioritise data collection and supplier engagement there. If downstream emissions in product use are material, that shapes your product development roadmap and customer engagement. If upstream emissions from raw materials dominate, procurement and supplier decarbonisation become strategic priorities.

This is also where carbon credits and removals enter the picture. A well-executed double materiality assessment highlights material climate risks (transition risk from carbon pricing, physical risk from extreme weather, reputational risk from climate claims) and material impacts (your value chain's contribution to global heating). High-quality carbon credits, used responsibly, can be one lever in your response to these material IROs, particularly for residual emissions where abatement is technically challenging or prohibitively expensive in the near term. But here's the critical point: low-quality or controversial offsets are themselves a material reputational and regulatory risk under CSRD.

Greenwashing via poor carbon credit procurement can trigger legal action, fines and lost stakeholder trust. Research shows that a significant share of carbon credits in the market have been found to deliver limited real climate impact, and regulators across Europe are tightening rules on environmental claims. If your double materiality assessment flags climate and reputational risk as material, then the quality, durability, additionality and transparency of any carbon credits you use become material issues too. This is where rigorous due diligence on carbon credit quality, backed by multiple layers of verification and transparent reporting, becomes non-negotiable. A framework that evaluates credits across hundreds of datapoints, covers carbon impact, social and environmental co-benefits, reporting integrity and compliance with emerging standards like ICVCM and CSRD, directly mirrors the level of rigour you should be applying in your double materiality assessment itself.

The connection is straightforward: your double materiality assessment identifies what's material, your climate strategy defines your response, and high-integrity carbon credits (when used) must meet the same standard of evidence and transparency that CSRD now demands across all your sustainability reporting.