CSRD

Key Takeaways

- CSRD reporting requirements apply to large DACH companies with >1,000 employees from FY 2025–2026 onwards, with ESRS E1 climate disclosures almost always material and the most technically demanding standard to implement.

- You must report gross Scope 1, 2, and 3 emissions separately from any carbon credits or removals—no netting allowed—and demonstrate a credible 1.5°C-aligned transition plan with interim targets tied to capital allocation.

- Carbon credits require strict separate disclosure under ESRS E1-7 with full documentation of quality, additionality, and permanence; weak evidence creates greenwashing risk and will not survive limited assurance.

- Build an audit-ready climate data system now: clear data lineage from source to disclosure, documented methodologies aligned with GHG Protocol and ESRS, and version-controlled evidence packs for emissions, targets, and any credits purchased.

If you're leading sustainability for a large company in Europe, you've likely spent the past year watching CSRD timelines shift while trying to figure out what it actually means for your climate reporting. Here's what matters: CSRD reporting requirements are now in force across the EU through the European Sustainability Reporting Standards (ESRS), and if your group has more than 1,000 employees and significant EU operations, you're almost certainly in scope for reporting on financial years starting 2025 or 2026.

The regulation is broad, covering environmental, social, and governance topics, but climate (ESRS E1) is where the real work sits. It's technically complex, almost always material under double materiality, and closely scrutinised by auditors, investors, and NGOs. Most large DACH companies already have GHG inventories, SBTi targets, and CDP responses in place, but CSRD demands more: granular Scope 3 data, forward-looking transition plans tied to financials, and, critically, transparent, defensible treatment of carbon credits that won't fall apart under limited assurance. This guide skips the legal details and shows you, in practical terms, what climate data you actually need, how to handle carbon credits without greenwashing risk, and how to be ready for your first audit.

1. CSRD Reporting Requirements in Plain Language and What They Mean for EU Corporates

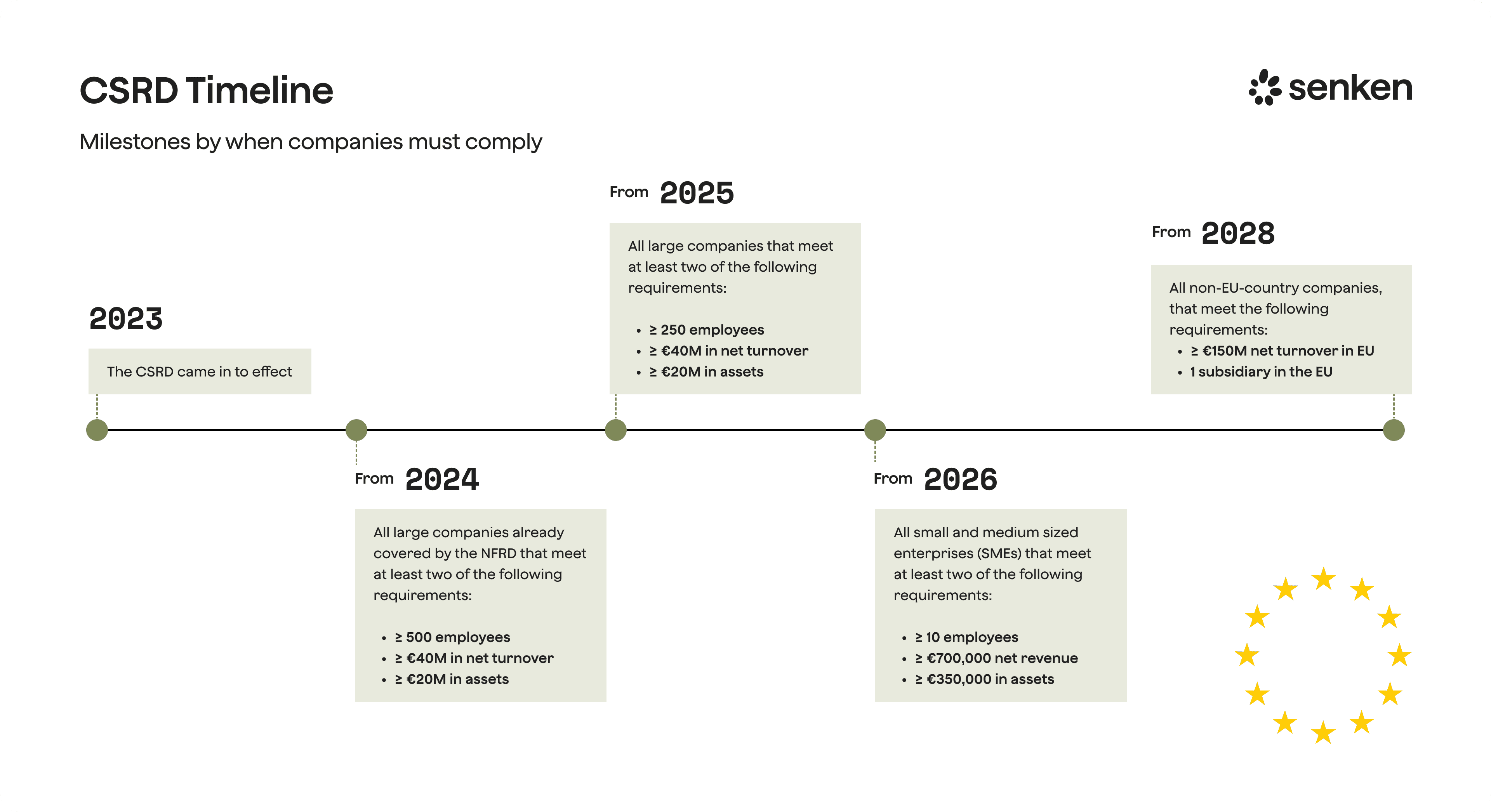

CSRD reporting requirements stem from the EU's Corporate Sustainability Reporting Directive (EU 2022/2464), which replaces the older NFRD and mandates much broader, more detailed sustainability disclosures. The directive is operationalised through the ESRS Delegated Regulation, applicable from financial years starting 1 January 2024. Large DACH companies need to understand three things quickly: who is in scope, when reporting starts, and what actually needs to be disclosed.

Scope focuses on large undertakings (typically those meeting two of three criteria: more than 250 employees, €50 million turnover, or €25 million in assets), listed entities, and non-EU parent companies with substantial EU operations. However, late 2025 developments have changed the timeline and thresholds. The EU's "stop-the-clock" decision delayed reporting waves by two years, and the proposed Omnibus simplifications are refocusing requirements on companies with over 1,000 employees and raising revenue thresholds to €450 million. For DACH groups, this means most large manufacturers, telcos, and financial institutions remain firmly in scope, but timing has shifted.

Timing for DACH is complicated by delayed national transposition. Germany and Austria faced infringement procedures for not implementing CSRD by the May 2025 deadline, so large groups should plan conservatively for first ESRS reports covering FY 2025 or 2026. Swiss companies face separate TCFD-based climate rules paused until 2027 to align with EU simplifications, but cross-border DACH groups with EU operations cannot wait.

For most large DACH companies, climate under ESRS E1 is the most material and technically demanding area. While ESRS covers environmental, social, and governance topics, nearly every large company finds climate material from both impact and financial perspectives. That's why this guide focuses on turning CSRD reporting requirements for climate into a concrete, audit-ready process.

2. ESRS and Double Materiality: How They Shape Your Climate Story

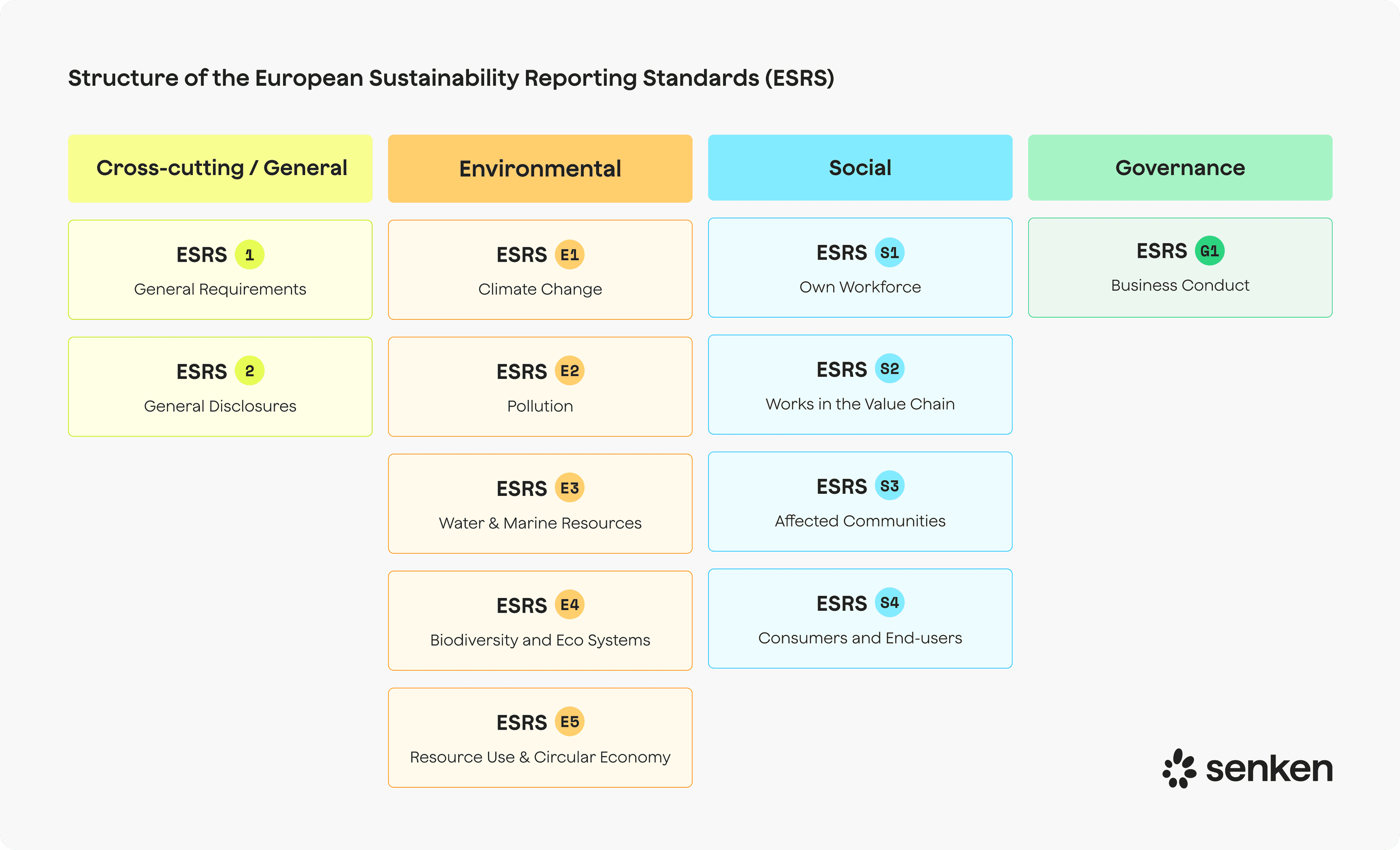

ESRS is structured in three layers: ESRS 1 and 2 provide cross-cutting principles and general disclosures, while topical standards cover environmental (E1–E5), social (S1–S4), and governance (G1) areas. ESRS E1 on climate change sits at the heart of this framework and will almost always be material for large DACH groups due to regulatory pressures, investor scrutiny, and value chain impacts.

Double materiality drives which topics you report and how deeply. It requires assessing sustainability matters from two angles: impact materiality (how your operations affect climate, people, and environment) and financial materiality (how climate risks and opportunities affect your business). For climate, most large companies find materiality on both sides: significant Scope 1, 2, and 3 emissions create impact materiality, while physical risks (flooding, heat stress) and transition risks (carbon pricing, stranded assets) drive financial materiality.

EFRAG's Implementation Guidance (IG 1 and IG 2) provides the operational backbone. The process involves identifying climate-related impacts, risks, and opportunities (IROs) across your entire value chain, scoring them against thresholds, engaging stakeholders, and documenting your methodology. For DACH groups with complex manufacturing or long supplier chains, this means mapping upstream emissions from raw materials and logistics, downstream use-phase emissions from sold products, and physical or regulatory risks at key sites and suppliers.

In practice, good-enough documentation for climate materiality includes: a short narrative of your assessment process, evidence of stakeholder input (internal workshops, investor feedback, supplier surveys), scoring criteria and thresholds, and a clear statement of why climate is material. Most large DACH companies will conclude ESRS E1 is material from both perspectives, so the real question is the depth and scope of disclosure, not whether E1 applies at all.

3. ESRS E1 Climate Change: What You Actually Need to Report

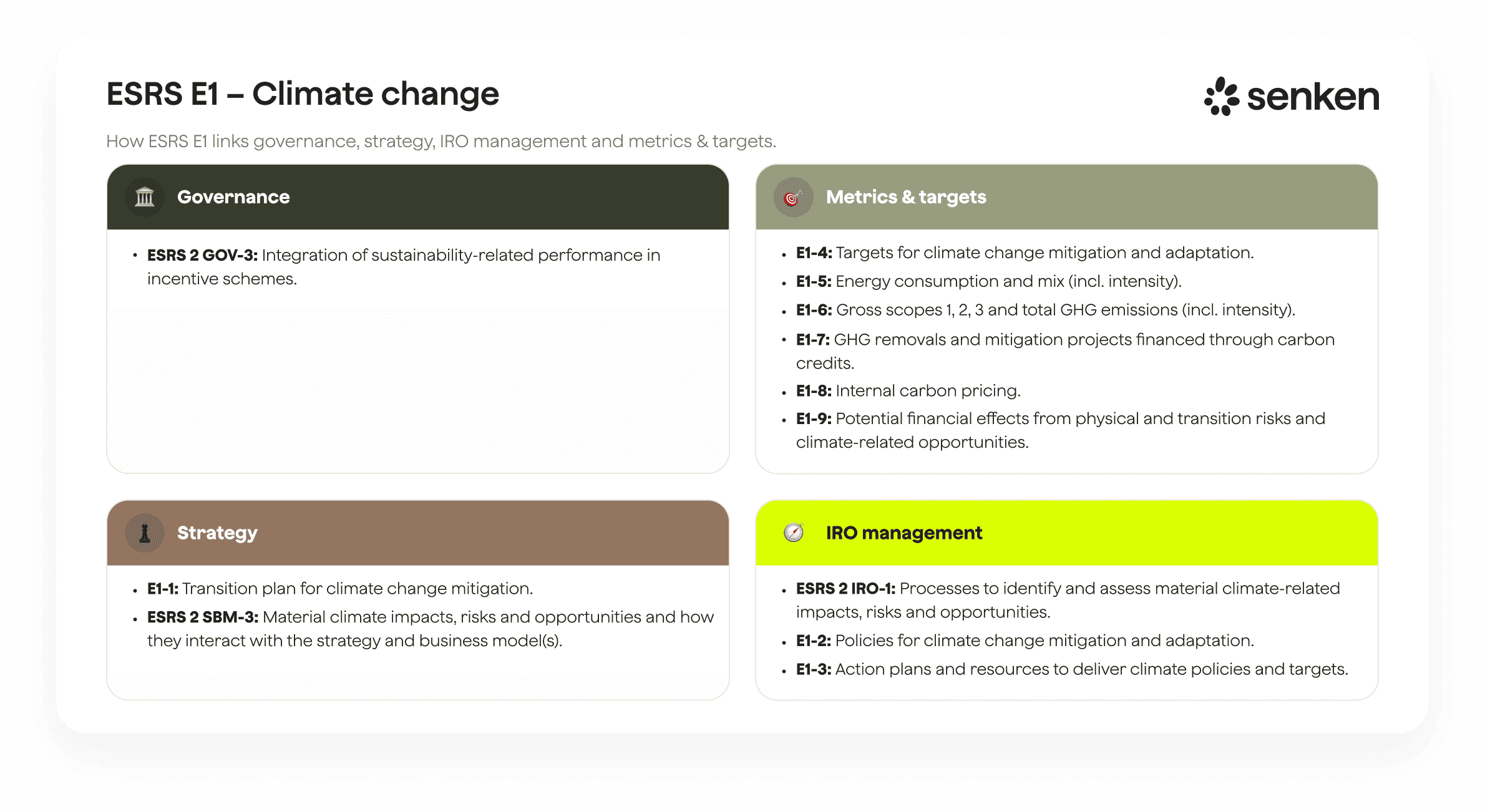

ESRS E1 translates climate ambitions into hard data. It requires disclosure across five core areas: transition plan and strategy, GHG emissions, targets, financial effects of climate risks and opportunities, and adaptation measures. For DACH sustainability leaders, the challenge is turning these into a concrete data model with clear owners.

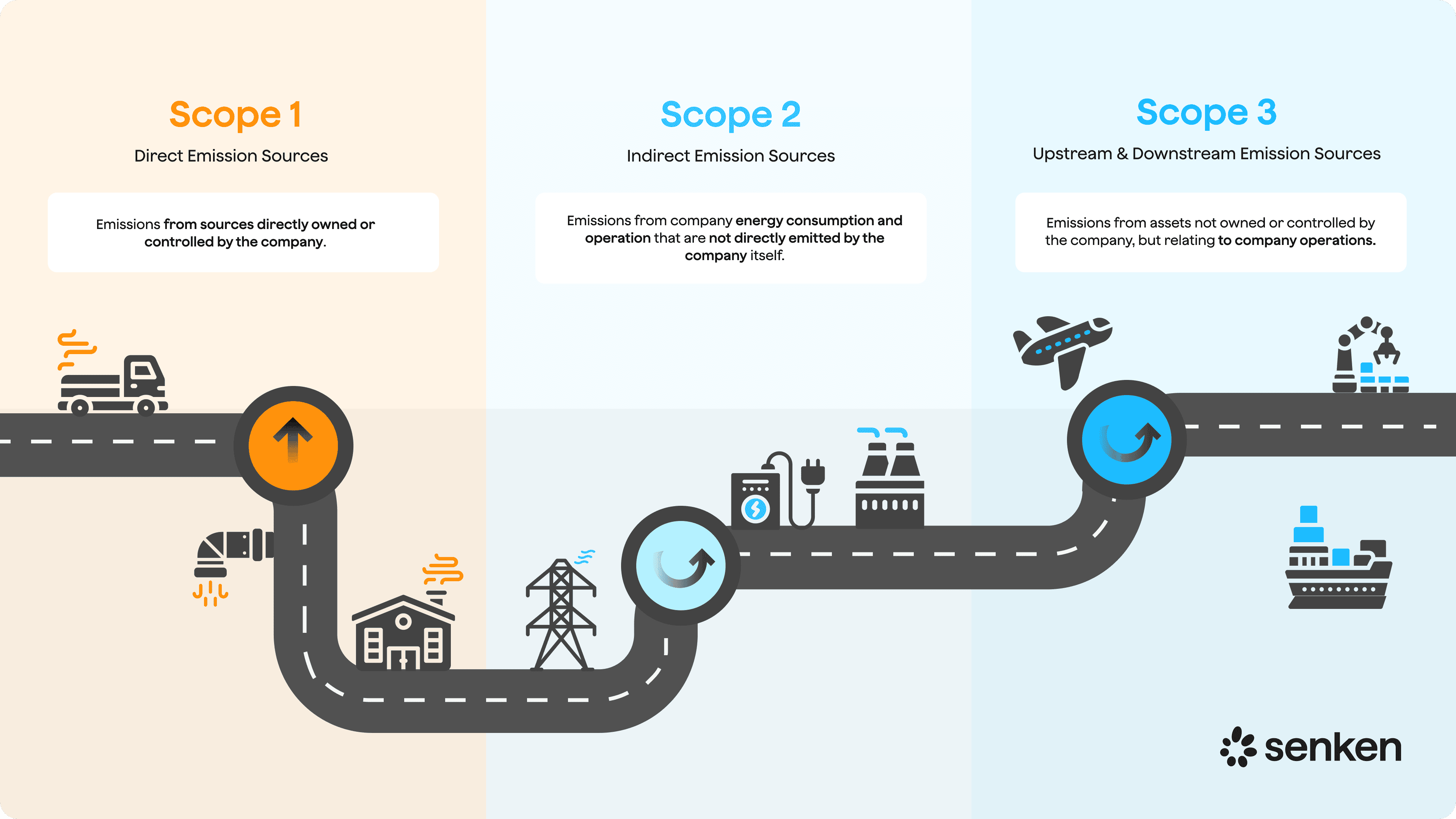

ESRS E1-6 mandates reporting of gross Scope 1, 2, and 3 emissions with no netting of removals or credits. Scope 2 must be reported using both location-based and market-based methods in line with the GHG Protocol Scope 2 Guidance. Scope 3 must be broken down by significant categories—typically purchased goods and services, upstream and downstream transport, use of sold products, and end-of-life treatment for DACH manufacturers and telcos.

Granularity matters. You need totals by scope, intensity metrics (e.g., emissions per revenue or per unit produced), and a clear explanation of methodologies, emission factors, and data sources. For Scope 3, this is where DACH groups face the biggest gaps: supplier-specific data is rare, so spend-based estimates dominate. EFRAG's IG 2 on value chain boundaries helps here, allowing proportional approaches and proxies when primary data is unavailable, but you must document assumptions clearly and show plans to improve data quality over time.

Phase-ins exist for smaller entities, but DACH groups over 1,000 employees should not rely on them. Regulators and auditors expect full scope coverage from year one, especially when you already report GHG inventories under CDP or SBTi.

3.2 Transition plan, targets, risks and resilience in practice

ESRS E1-1 and E1-4 require a transition plan aligned with the EU's 1.5 °C climate law. This means setting science-based targets with a clear base year, interim milestones (e.g., 2030), scope coverage (ideally all three scopes), and linkage to capital expenditure and operational plans. If your company has SBTi-validated targets, you're halfway there—but CSRD goes further, asking how capex, R&D, and procurement budgets support decarbonization.

For example, a DACH manufacturing group might disclose €50 million annual capex for electrification of production lines and €10 million for supplier engagement programs to cut Scope 3 emissions. The transition plan should also address decarbonization levers: energy efficiency, renewables procurement, product redesign, and—transparently—any planned use of carbon removals to address residual emissions post-2040.

ESRS E1-9 covers the financial effects of climate risks and opportunities. You must describe physical risks (e.g., supply chain disruption from flooding at a key supplier site) and transition risks (e.g., exposure to rising carbon prices in the EU ETS or tightening product standards). Scenario analysis is encouraged, but qualitative disclosure is acceptable in the early years. The key is showing your board, and the CFO understands and prices climate into financial planning.

This is where existing TCFD, ISSB, or CDP work can be reused. EFRAG and IFRS published detailed interoperability guidance in 2024, confirming high alignment between ESRS E1 and IFRS S2 (ISSB climate standard). You can use a "top-up" approach: start with your ISSB or CDP response, then add ESRS-specific datapoints like dual Scope 2 methods or EU-specific policy risks.

4. Carbon Credits and Removals Under CSRD: Separate, High-Quality, and Defensible

CSRD reporting requirements treat carbon credits and removals with strict discipline. ESRS E1-6 requires gross emissions reporting—no netting of removals or credits. E1-7 demands a separate disclosure of removals within your value chain and any credits financing projects outside your value chain. Critically, credits cannot be used to show progress against E1-4 reduction targets or to claim your emissions are lower than they are.

This separation matters for two reasons. First, it protects against greenwashing: stakeholders see your real emissions trajectory independent of credit purchases. Second, it forces transparency on credit quality. E1-7 asks for volumes, project types, registry details, whether projects are in or out of your value chain, and key quality attributes like additionality, permanence, and avoidance of double counting.

What does high-quality mean in a CSRD context? The ICVCM Core Carbon Principles (CCPs) have become the emerging market baseline. Credits should demonstrate robust additionality (the project wouldn't happen without carbon finance), permanence (carbon stays locked away for centuries, not years), minimal leakage, and verified quantification. For removals, durability is critical—DACH companies aligning with the Oxford Principles for Net-Zero should prioritise removals with over 200 years of storage.

In practice, build an internal carbon credit evidence register. Fields should include: registry ID and retirement certificate, methodology and validator/verifier, ICVCM CCP status, external ratings (BeZero, Sylvera), project type and location, volumes retired, and treatment of reversal risk. Senken's Sustainability Integrity Index evaluates credits across 600+ datapoints spanning these quality dimensions, offering CSRD-ready scorecards that stand up to auditor scrutiny.

DACH groups should also define internal eligibility rules. For example: "We only purchase credits rated A or higher by independent agencies, aligned with ICVCM CCPs, and verified under methodologies with low controversy." This policy becomes part of your E1-7 disclosure and demonstrates governance over carbon credit use. Recent research shows 68% of DAX 40 companies ended up with low-impact credit portfolios, often due to weak vendor due diligence—an avoidable risk with clear quality thresholds.

5. Making Climate and Carbon Data Audit-Ready from Day One

CSRD mandates limited assurance on sustainability information from the first reporting year, with a potential move to reasonable assurance later (though the Omnibus proposal may remove that requirement). Limited assurance under the ISSA 5000 standard means auditors will test whether your disclosures are plausible, consistent, and traceable—not whether they are perfect.

For ESRS E1 climate data, auditors will focus on four areas. Methodology consistency: Are you applying GHG Protocol and ESRS rules correctly, and are emission factors and calculation approaches documented? Traceability: Can you trace reported emissions back to source data (utility bills, fuel invoices, activity data from production systems)? Assumptions and estimates: Especially for Scope 3, are proxies and spend-based estimates clearly documented, justified, and regularly reviewed? Carbon credit evidence: For any removals or credits disclosed under E1-7, can you show registry confirmations, project documentation, and quality assessments?

Common early findings from CSRD readiness surveys include weak Scope 3 methodologies, undocumented estimation techniques, inconsistent emission factors across sites, and poor evidence on carbon credits. A 2024 PwC survey of DACH companies found data availability and value chain complexity as the top obstacles, with many still relying on spreadsheets rather than integrated ESG systems.

To be assurance-ready, assemble an ESRS E1 evidence pack structured around the disclosure areas. For GHG emissions, include: calculation files with clear formulas and factor sources, activity data extracts from ERP or operations systems, assumptions logs for estimates, sign-offs from data owners (e.g., procurement for Scope 3 categories), and reconciliations to financial data where relevant (e.g., energy spend). For carbon credits, maintain the evidence register described earlier plus contracts, retirement confirmations, and third-party project assessments.

Governance matters too. Set up a CSRD steering committee with finance, risk, operations, and sustainability, and implement version control and approval workflows for reported figures. Document your double materiality process and update it annually. This upfront investment in controls and documentation pays off in smoother audits, fewer qualifications, and greater stakeholder confidence.

6. A Six-Step Roadmap to Operationalise CSRD Climate Reporting in DACH

Here's a practical playbook for Heads of Sustainability in large DACH companies, designed to integrate CSRD into existing climate work rather than creating a parallel track.

Step 1: Run a focused CSRD/ESRS E1 gap and double materiality assessment. Map your current climate reporting (GHG inventories, SBTi targets, CDP, TCFD) against ESRS E1 requirements. Identify gaps—typically in granularity (Scope 3 by category, dual Scope 2 methods), documentation (double materiality evidence, assumptions logs), and new disclosures (financial effects of climate risks, carbon credit details). Conduct or refresh your double materiality assessment for climate, involving internal stakeholders and external perspectives (investors, NGOs, suppliers).

Step 2: Design a simple ESRS E1 data model and assign owners. Turn E1 requirements into a structured data inventory: which metrics, at what granularity, from which systems, owned by whom. For example, Scope 1 owned by operations, Scope 2 by facilities/energy, Scope 3 categories 1 and 2 by procurement, category 11 by product management, and financial risk impacts by risk/finance. Use a RACI matrix to clarify who is responsible, accountable, consulted, and informed for each datapoint.

Step 3: Prioritise Scope 3 categories and set up supplier engagement. Not all 15 Scope 3 categories will be significant. Focus on the largest (often purchased goods, upstream transport, use of sold products for DACH manufacturers). Develop a supplier engagement roadmap: start with top suppliers by spend or emissions, request primary data using standardized templates, and document estimation methods for suppliers who cannot provide data. EFRAG IG 2 allows proportional approaches, so show you are improving data quality year-on-year rather than achieving perfection immediately.

Step 4: Define an internal carbon credit policy and evidence register. Decide your approach to carbon credits and removals: which types are acceptable (removals only? nature-based and tech-based?), what quality bar (ICVCM CCP-aligned? Oxford Principles?), and how you will document and retire them. Build the evidence register template and integrate it into procurement workflows so every credit purchase automatically generates audit-ready documentation. Use tools like Senken's Sustainability Integrity Index to pre-screen projects and build a defensible portfolio aligned with CSRD expectations.

Step 5: Leverage interoperability with existing frameworks. Map your SBTi targets directly to E1-4 (they likely already meet the 1.5 °C alignment requirement). Pull your Scope 1/2/3 inventory from CDP into ESRS E1-6 format, adding dual Scope 2 and category breakdowns as needed. If you report under ISSB or Swiss TCFD rules, use the EFRAG/IFRS interoperability guidance to identify overlaps and top-ups. Connect EU Taxonomy capex KPIs to your ESRS E1 transition plan. Align value chain risk work under Germany's LkSG (Supply Chain Act) or upcoming CSDDD with E1 value chain assessments. The goal is a single climate data backbone serving multiple regimes, not separate silos.

Step 6: Build basic governance and assurance-readiness. Establish a CSRD reporting calendar aligned with your financial close, with milestones for data collection, validation, management review, and external assurance. Create the E1 assurance pack described earlier, with clear folder structures, document naming conventions, and version control. Run an internal dry-run or pre-assurance review six months before your first report to surface and fix gaps. Train data owners on what auditors will ask and why traceability matters. Finally, ensure board-level visibility: your CFO and audit committee should understand the CSRD climate data process, timelines, and key judgments (especially around Scope 3 estimates and carbon credit use).

Each step produces a tangible output—gap assessment memo, data model spreadsheet, supplier engagement tracker, carbon credit policy document, framework mapping table, assurance pack folder structure—that moves you from regulatory text to operational reality. Most large DACH companies already have 60–70% of the building blocks from GHG Protocol, SBTi, and CDP work; CSRD is the integrating framework that raises the bar on documentation, granularity, and audit-readiness.