💡 The carbon credit paradox: smart buyers matter most in messy markets

A sustainability lead at a DAX company said this to me last week: "Adrian, with all the scandals, the press coverage, the rating agencies tearing projects apart, the smart move is just to stop. We will reduce internally and forget the offset market. Way less reputational risk."

I understood her instinct. I disagreed with her conclusion.

Stopping is the most dangerous mistake a corporate can make right now. There are three reasons for that, one emotional, one scientific, one regulatory and economical. And there is one thing that connects all three. I want to walk you through both in this issue.

First, let me concede the obvious

I sell carbon credits for a living. And I will be the first to tell you: the majority of what is on the voluntary carbon market today does not deliver what it promises.

The press is not wrong. The Guardian's investigation found 90% of certain rainforest credits to be effectively worthless. Die Zeit called offsetting "a free pass to pollute". Der Spiegel called it "the great carbon credit fraud". Handelsblatt: "companies are buying hot air".

The data is even sharper. We at Senken pulled every 2025 CSRD report from the DAX40 for our 'Buying Blind?' Report. 21 of 39 companies actively buy carbon credits. 4.84 million tCO2e in retired volume. 60% of the projects we could assess sit below BBB, the minimum credible threshold. 46% of the total volume was not publicly disclosed at all. That is procurement in the dark.

So yes, the criticism is justified. The market has a quality problem. That is not the question.

The question is what you do with that information. And the wrong answer is "nothing".

Reason one: emotional

I am about to become a father. In a few weeks.

I want my son to grow up walking through forests that still exist. To see species that are still alive. To inherit a climate that is still survivable. That is not a strategy slide. That is non-negotiable for me, and I suspect for most people reading this.

Walking away from carbon credits because the market is messy is the climate equivalent of refusing to invest in any company because Wirecard happened. The scandal is real. The asset class is still necessary.

Pulling capital out of credible removal and avoidance projects does not punish the bad actors. It starves the good ones. The 5% of projects that actually work need buyers. If the entire corporate sector pivots away in disgust, the projects we need most, the rare ones with real additionality, real permanence, real measurable impact, lose their funding base. The cynics win.

Reason two: scientific

Even the loudest skeptics in the climate science community agree on one thing: carbon removal is not optional.

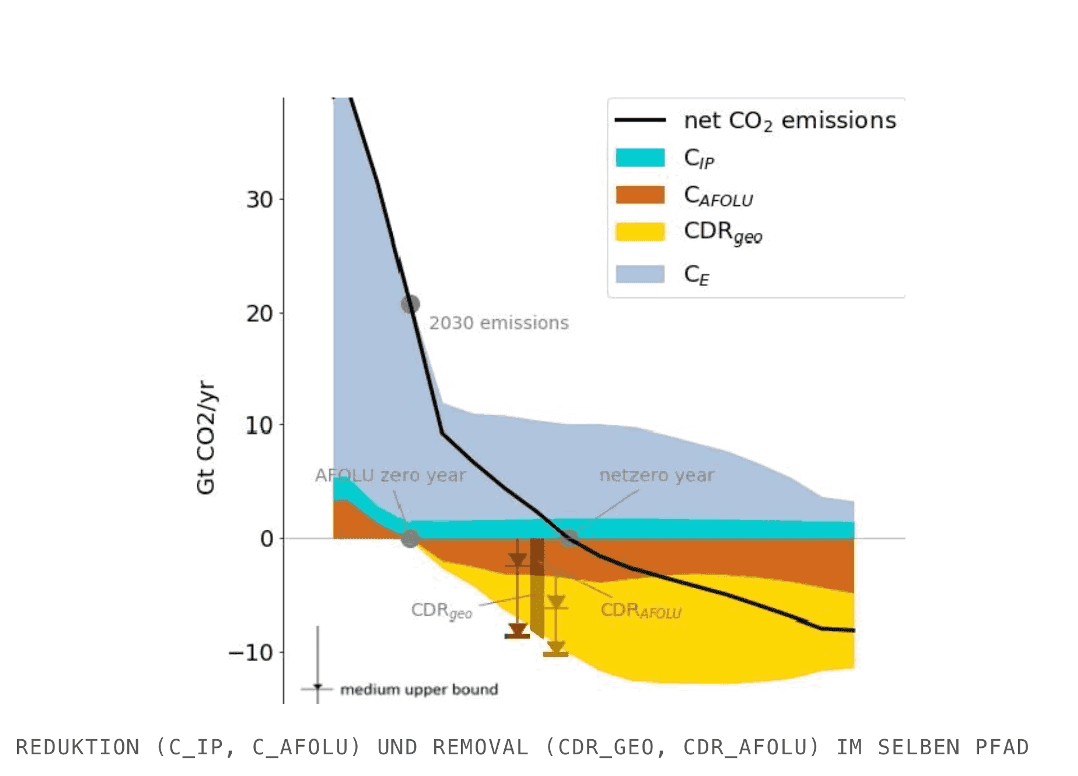

Look at any credible Net Zero pathway. PIK, Rogelj et al., the IPCC AR6 scenarios. They all show the same picture. Reducing emissions takes us most of the way. It does not take us all the way. The remaining residual emissions, the hard-to-abate processes, the agriculture footprint, the cement and steel and aviation tonnes that cannot be eliminated this decade, have to be removed from the atmosphere. Not "compensated for". Removed.

That is not opinion. That is arithmetic. If your scope 1, 2 and 3 trajectory leaves 20% on the table in 2040, and you have not built a removal portfolio to address it, you do not reach Net Zero. You reach 80%. There is no version of climate science in which that gap closes by itself.

And here is the part that nobody on a corporate sustainability team wants to hear. Look at the PIK pathway chart side by side. The wedge for carbon removal, geological and AFOLU combined, is roughly the same size as the wedge for carbon reduction by 2050. Removal is not a rounding error at the bottom of the curve. It is a parallel undertaking of equivalent scale. We are talking about pulling gigatonnes per year out of the atmosphere, every year, for the rest of the century.

So why is reduction treated as the serious work and removal as the optional sideshow? Why does the average corporate climate strategy have ten people working on emissions reduction and zero on building a removal portfolio? The science says the two efforts are equally large. The corporate org chart pretends only one of them exists. That is the gap. And it is going to close, fast, the moment auditors and regulators start asking the same question.

So the question is not whether you need carbon removal. You do. The question is whether you start building the relationships, the supply contracts, and the institutional knowledge now, when prices are still in the low hundreds, or whether you wait until 2032 and pay 10x for what is left.

Reason three: regulatory and economical

The rules now require it. SBTi v2, ISO 14068, CSRD, the Oxford Principles. All four explicitly demand that residual emissions be addressed through high-integrity removals. Net Zero without removal is no longer Net Zero. It is marketing.

If you are reporting under CSRD this year, your auditor will ask how you intend to neutralise residuals. "We don't" is not an answer that survives a limited assurance review, let alone reasonable assurance.

The economics make the same point in a different language. The last 20 to 30% of any corporate decarbonisation curve is brutal. Eliminating that final tonne inside your own operations, retrofitting, replacing fleets, redesigning processes, can cost upwards of €5,000 per tonne. The same physical effect, removed from the atmosphere via a high-quality removal credit, costs €100 to €200 today.

That is a 25 to 50x cost gap. For the same physical outcome, measured in tonnes. No CFO who has done this math walks away from the option.

The companies waiting for the market to "stabilise" before they enter are making the most expensive bet in their decarbonisation strategy. Removal supply is finite, growing slowly, and will be heavily oversubscribed by 2030. The price curve only goes one direction.

What connects all three

For my future child, for the PIK pathway, for the auditor, the answer is the same word.

Data.

Data that proves the forest actually came back. Not "we planted, fingers crossed".

Data that proves the tonne actually left the atmosphere. Not modelled, not estimated, measured.

Data that holds up in front of SBTi, in front of CSRD reasonable assurance, in front of the Wirtschaftsprüfer who is going to ask "can you evidence this?" and expects a binder, not a brochure.

Every scandal you have read about in the last three years has the same root cause. Buyers retired credits without independently verifying additionality, permanence, quantification, leakage, or governance. They trusted the project developer's PDD and the registry stamp. That is not due diligence. That is faith.

The right question to ask in your next supplier meeting

Stop asking "is this Verra or Gold Standard?". The registry is the floor, not the ceiling.

Start asking:

- How many independent data points support this project, and can I see the underlying evidence?

- What is your rejection rate, and on what criteria?

- If I retire 50,000 tonnes from this portfolio, can I export an audit-ready evidence file my Wirtschaftsprüfer can open and follow?

- What did the project look like before, and what does the satellite imagery show today?

If the supplier cannot answer those questions in detail, walk away from that supplier. Not from the asset class.

Bottom line

The scandals are real. The 95% is real. The press is justified.

And none of that changes the fact that:

- Your child needs functioning ecosystems funded by buyers who did not flinch.

- Climate science gives you no Net Zero pathway without removal.

- Regulation now mandates it, and the economics reward early entry by an order of magnitude.

The path through the paradox is not less carbon credit purchasing. It is more disciplined carbon credit purchasing. Demand data, demand evidence, demand a rejection rate, demand audit-readiness. If you cannot get those, the project is not for you. If you can, the project is one of the few that is genuinely moving the needle.

Walking away is the easy solution. It is also the wrong one.

Coming soon: Buying Blind? Report

Everything I referenced above, the 21 of 39 DAX40 companies, the 4.84 million tonnes, the 60% below BBB, comes from our upcoming 'Buying Blind?' Report, incollaboration with Sylvera. We independently assessed 98 of 112 projects retired across FY2025 CSRD disclosures.

If you want to see how your peers actually scored, and whether your own portfolio would survive the same audit, Keep an eye out for the full report in coming weeks!

Sources

- Senken 'Buying Blind?' Report 2025, DAX40 CSRD analysis (98 of 112 projects independently assessed)

- The Guardian, "Revealed: more than 90% of rainforest carbon offsets by biggest certifier are worthless"

- Die Zeit · Handelsblatt · Süddeutsche Zeitung · Der Spiegel, offset-market coverage, 2023–2025

- Rogelj et al. / PIK Net-Zero pathway analysis

- IPCC AR6 WG3, Chapter 12 (Cross-sectoral perspectives)

- SBTi Corporate Net-Zero Standard v2

- ISO 14068-1:2023, Climate change management

- CSRD / ESRS E1

- University of Oxford, Principles for Net Zero Aligned Carbon Offsetting (revised 2024)