🇪🇺 EU ETS meets CDR: the integration nobody is ready for

The EU ETS is in the middle of its most consequential rewrite since Phase 3. And with the Commission’s Article 30 deadline locked for July 2026, the question is no longer whether CDR will be included — but how and when.

This newsletter covers where the EU ETS stands now, explains the four integration models the Commission is weighing, breaks down what this means for voluntary buyers and ETS-covered corporates, and shows why biochar and EUA prices are about to converge.

30-second snapshot: where the EU ETS stands right now

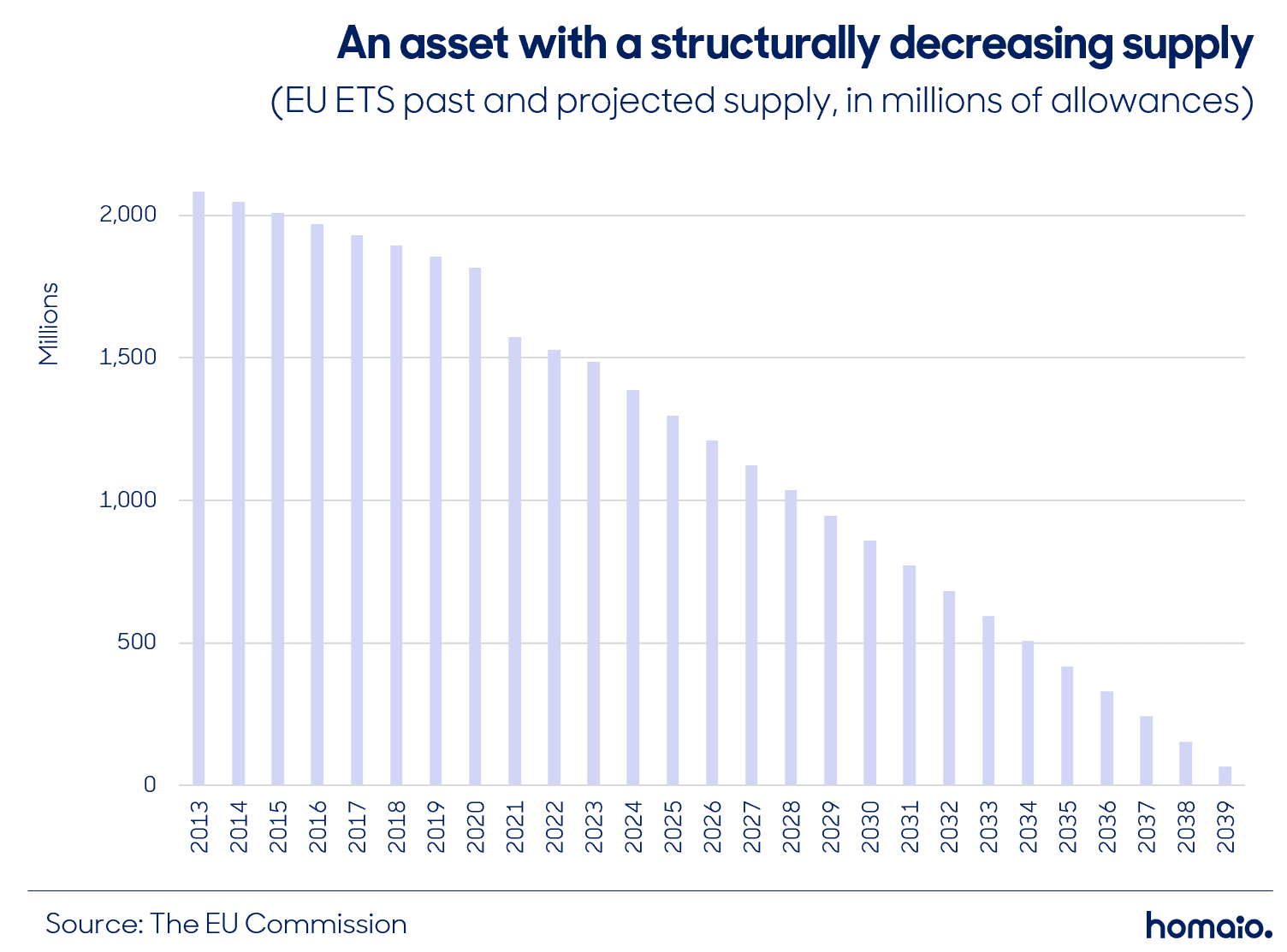

The EU ETS is in the middle of its most consequential rewrite since Phase 3. The linear reduction factor is now 4.3%, stepping up to 4.4% from 2028, and two one-off cap cuts in 2024 and 2026 have pulled roughly 117 Mt of allowances out of the system. Free allocation for CBAM-exposed sectors is phasing out on a fixed glide path, and the definitive CBAM regime went live in January 2026, which means importers of steel, cement, aluminium, fertilisers, hydrogen and electricity are now paying the full carbon cost at the border.

ETS2, the parallel system for buildings and road transport fuels, launches in 2027. Most analysts expect it to front-load price pressure well before that, as fuel suppliers start hedging their 2027 exposure this year. EUA prices have settled in the €75 to €90 range after a volatile 2024 and 2025, and the Market Stability Reserve keeps absorbing surplus. The political conversation has moved from “is the cap tight enough” to “what happens when we run out of conventional abatement”.

That last question is why CDR is suddenly on every Brussels agenda.

CDR inclusion: what the Commission actually has to do

Article 30 of the revised ETS Directive gives the Commission a hard deadline. By 31 July 2026 it must publish a report on how negative emissions could be accounted for and, if appropriate, covered by emissions trading. That report will sit alongside the 2040 climate target legislation and the Industrial Carbon Management Strategy, which together sketch a pathway of roughly 75 Mt of industrial CDR by 2040 and around 400 Mt across all removal categories.

Translation: the Commission is not debating whether to include CDR. It is debating how and when.

The quality backbone is already in place. The Carbon Removal Certification Framework was adopted in late 2024 and is now being populated with methodologies for permanent storage (DACCS, BECCS, enhanced weathering, mineralisation), carbon farming, and long-lived products. CRCF is explicitly designed to be the gatekeeper for any future compliance use. No CRCF label, no access to the ETS. That is the emerging consensus in DG CLIMA and the Scientific Advisory Board on Climate Change has backed it in its 2024 and 2025 reports.

Where the debate gets heated is on three questions: which CDR categories qualify (permanent only, or also carbon farming and hybrid solutions), whether removals are fungible with allowances or sit in a parallel pool, and whether there is a quota that ETS installations must buy.

Potential volume: the numbers that should wake you up

The EU ETS covers around 1.35 Gt CO2e in stationary and aviation emissions today. ETS2 adds roughly another 1 Gt when it goes live. That is the pool any CDR integration mechanism would plug into.

For context, the entire voluntary CDR market in 2025 delivered fewer than 500,000 tonnes of durable removals, with a total contracted pipeline across all suppliers of perhaps 10 to 15 Mt stretching to 2030. The gap between voluntary demand and what a compliance market could pull in is roughly two orders of magnitude.

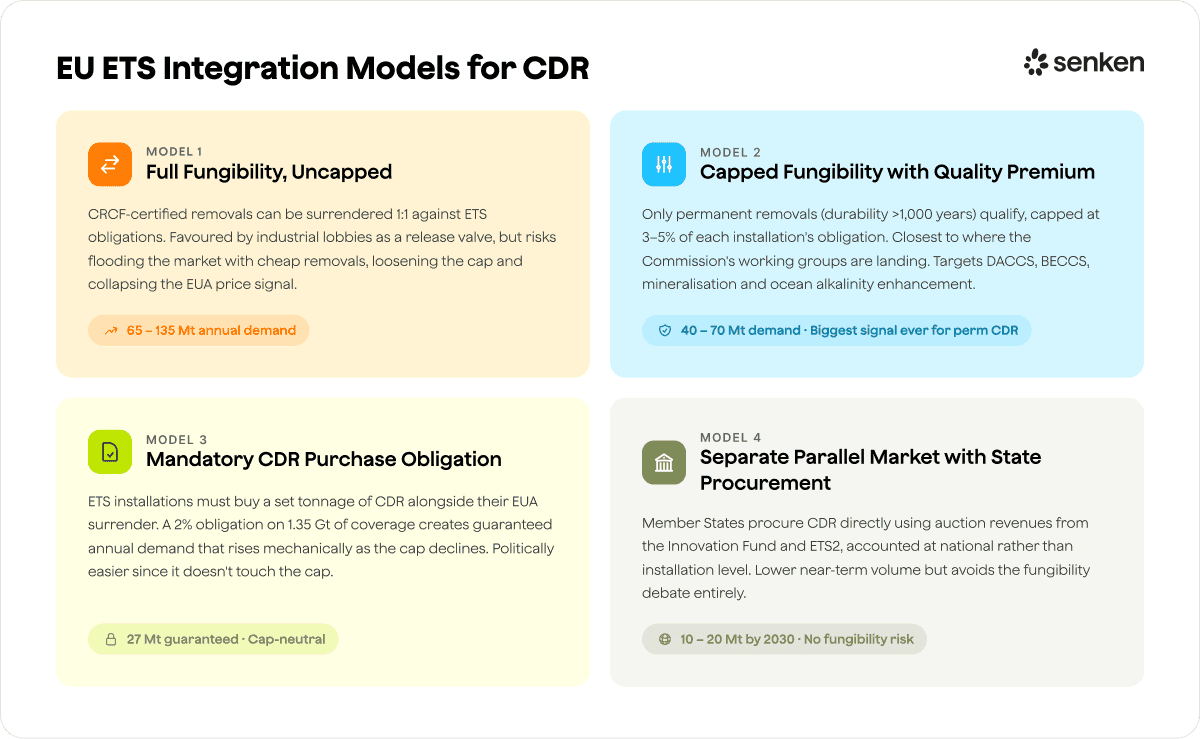

Let me run four integration models and what each would mean for volume.

Model 1: full fungibility, uncapped. CRCF-certified removals can be surrendered 1:1 against ETS obligations. This is the model most industrial associations are lobbying for because it gives them a release valve. The risk for the Commission is obvious: cheap removals flood in, the cap effectively loosens, and the price signal collapses. If even 5% of ETS obligations were met with CDR, that is 65 to 70 Mt of annual demand. At 10%, it is 135 Mt. Either number dwarfs the entire current CDR industry by a factor of 100 or more.

Model 2: capped fungibility with a quality premium. Only permanent removals (durability above 1,000 years) qualify, capped at 3 to 5% of each installation’s obligation. This is closer to where the Commission’s internal working groups seem to be landing. It would generate 40 to 70 Mt of annual compliance demand for DACCS, BECCS, mineralisation and ocean alkalinity enhancement. That is the single biggest demand signal these technologies have ever had.

Model 3: mandatory CDR purchase obligation. Instead of fungibility, ETS installations are required to buy a set tonnage of CDR alongside their EUA surrender. A 2% obligation on 1.35 Gt of coverage is 27 Mt of guaranteed annual demand, rising mechanically as the cap declines. Germany’s Langfristige Negativemissionen-Strategie already floats a version of this for hard-to-abate sectors. It is politically easier than fungibility because it does not touch the cap.

Model 4: separate parallel market with state procurement. Member States procure CDR directly using auction revenues from the Innovation Fund and ETS2, and account for them at national level rather than at installation level. Lower volume in the near term, perhaps 10 to 20 Mt per year by 2030, but it avoids the fungibility debate entirely.

My base case for 2026 to 2027: the Commission proposes Model 2 or Model 3, with a hard quality gate via CRCF, starting small (1 to 2% of obligation) and escalating through the 2030s. Both produce 20 to 30 Mt of compliance demand by 2030 and 100 Mt plus by 2035.

What this means if you buy carbon credits voluntarily

If you are a sustainability manager running a voluntary portfolio today, this is the most important market shift you need to price in. Three things happen in parallel.

First, durable CDR supply is going to get pulled out of the voluntary market and into compliance the moment integration is confirmed. The suppliers you are talking to now (Climeworks, Stockholm Exergi, 1PointFive, Heirloom, CarbonCure, Eion, and so on) will have a compliance buyer queuing up with deeper pockets and regulatory urgency. If you want offtake, you lock it in before the Article 30 report lands in July 2026, not after.

Second, pricing. The voluntary price for durable CDR sits between €250 and €700 per tonne depending on technology. Once compliance demand arrives, the floor moves up, not down. Anyone expecting CDR to get cheaper as it scales is half right and half wrong: unit costs will decline with deployment, but the marginal compliance buyer will set the clearing price and that buyer can afford to pay more than you can.

Third, SBTi alignment gets easier. SBTi v2 explicitly wants corporates to build neutralisation portfolios now, with durable removals scaling toward 2050. A functioning CDR compliance market makes the supply side credible in a way the voluntary market alone cannot.

Practical takeaway: if CDR sits anywhere in your target architecture, you should be contracting multi-year offtake in 2026, not running another RFP in 2027.

What this means if you are already in the EU ETS

For installations under the cap, CDR integration is both an opportunity and a new cost line. The opportunity is flexibility. Marginal abatement in cement, steel, chemicals and refining is expensive, often north of €200 per tonne for the last 20% of emissions. If CRCF-certified removals are available at comparable or lower cost, they become a legitimate compliance tool. That is a real saving for sectors where electrification or hydrogen are still a decade out.

The cost line comes in two forms. Under a fungibility model, you need procurement infrastructure you probably do not have today: supplier diligence, long-term offtake contracting, counterparty risk management for removal vintages that deliver 5 to 15 years out. Under a mandatory quota model, you have no choice at all. The tonnage is set by regulation and you pay the clearing price.

Either way, the teams that start building CDR procurement capability in 2026 will outperform the teams that wait for the regulation to land. This is the same pattern we saw with CBAM, where the companies that ran pilot reporting in 2023 and 2024 are now operating smoothly, and the companies that waited are scrambling.

One underappreciated point: free allocation phase-out and CDR integration interact. As free EUAs disappear for CBAM sectors between now and 2034, the effective carbon cost per tonne of product rises sharply. CDR becomes relatively cheaper as EUA prices climb, which is exactly when compliance demand for removals will accelerate. Plan your 2030 to 2035 procurement curve with that in mind.

Source: Enerdata

Pricing: where biochar meets the EUA curve

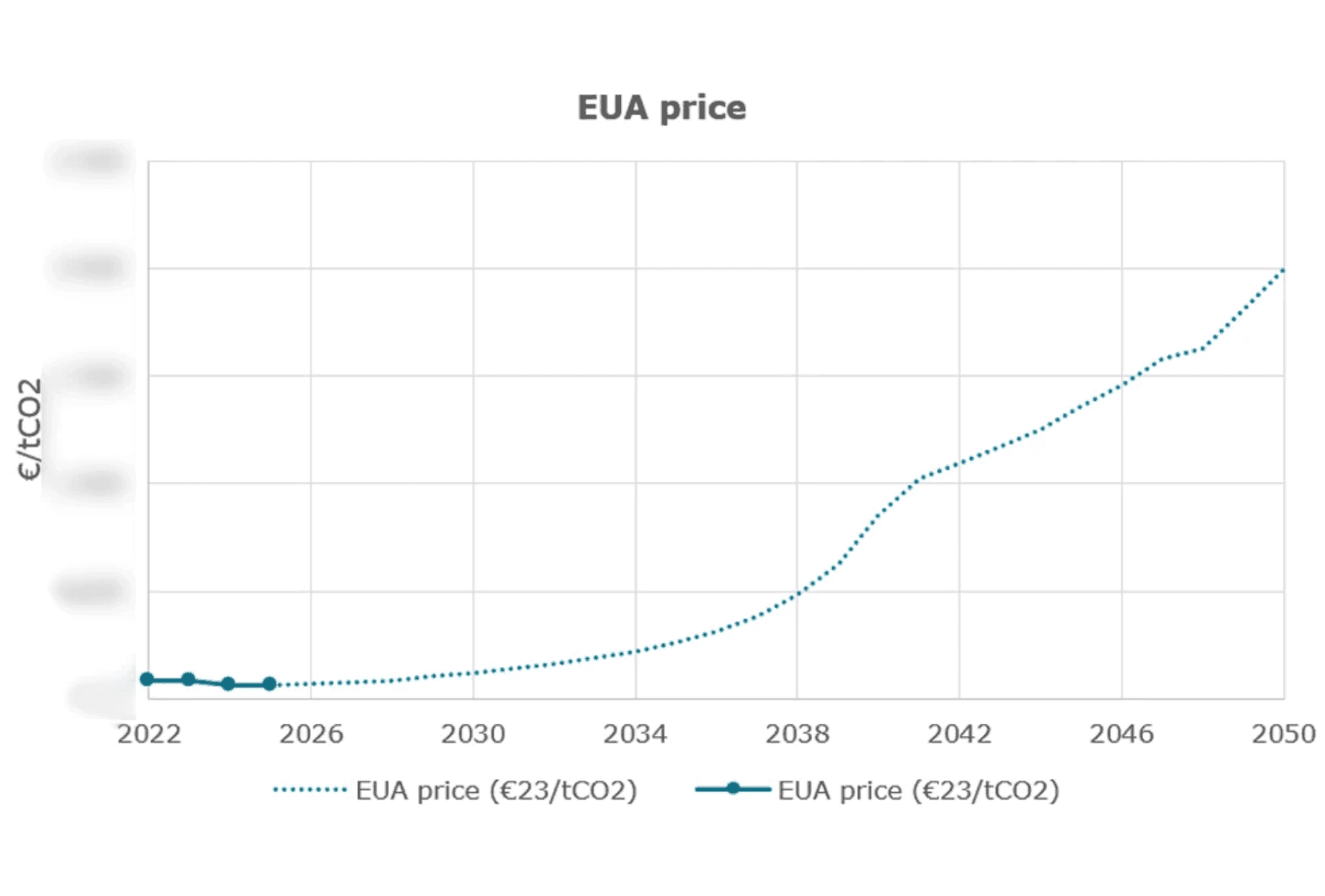

This is the part of the conversation that most sustainability managers still get wrong. They look at today’s EUA price around €80 and today’s European biochar price between €170 and €210 per tonne and conclude that removals will never be competitive with compliance. That view does not survive contact with the 2031 forward curve.

The consensus forecasts for EUA prices in 2031 cluster around €140 to €170 per tonne in the base case. BNEF’s 2025 long-term outlook sits near €149, ICIS has modelled €155 to €165 depending on ETS2 linkage, and Veyt’s central scenario lands around €145. Upside cases from Morgan Stanley and Bernstein push €200 plus if the 2040 target is formally set at 90% net reduction and the linear reduction factor accelerates. The political signal from Brussels in the last six months, including the Commission’s 2040 communication and the Scientific Advisory Board’s guidance, points toward the upper half of that range rather than the lower.

Now overlay European biochar. Current CRCF-track biochar pricing sits at €170 to €210 per tonne for verified, EBC certified product with durability above 100 years. Unit economics are improving as operators scale, but the floor is set by feedstock logistics and pyrolysis capex, so I do not expect average prices below €150 before 2030. Call the 2031 range €160 to €200, roughly flat to modestly down from today.

The lines cross around 2029 to 2031. In the base case, EUA and durable biochar trade inside the same €150 to €200 band by the time the Commission’s Article 30 framework would be operationally live. In the upside EUA case, biochar trades at a discount to allowances for the first time in the ETS’s history. Either way, the price gap that makes CDR feel expensive today disappears within the procurement planning horizon of anyone reading this.

Two implications matter.

For voluntary buyers, contracting biochar offtake at €170 to €210 in 2026 looks like a premium. By 2031 it looks like a hedge against a compliance market trading at the same level or higher, with the added benefit that you locked in supply before compliance buyers arrived. This is the cleanest arbitrage in the removal market today, and it is hiding in plain sight because the price tag shocks people out of doing the forward maths.

For ETS-covered installations, the 2031 convergence is the strategic case for starting biochar procurement now. If you expect to surrender EUAs at €150 to €170 in 2031, and CRCF opens the door to using certified biochar against part of that obligation, the rational move is to lock offtake at today’s prices through long-term agreements, with delivery scheduled to align with your surrender calendar. Your 2031 compliance cost drops and you get the stacked benefit of supporting the methodology build-out that will shape which removal types qualify in the first place.

Higher durability categories (DACCS, BECCS, mineralisation) sit above this range at €250 to €700 per tonne today and will not converge with EUAs until the mid 2030s at the earliest. That is a separate portfolio decision, driven by SBTi v2 alignment and corporate durability preferences, not by near-term price parity. But biochar is different. Biochar is the category where the compliance and voluntary prices are about to meet, and the buyers who see that first will have a material advantage.

The honest bottom line

CDR inclusion in the EU ETS is not a question of if. The Article 30 deadline is locked, the CRCF is built, the 2040 target assumes hundreds of megatonnes of removals, and the Industrial Carbon Management Strategy has already set the direction. The real unknowns are the integration model, the starting quota, and whether carbon farming gets in alongside permanent removals.

For voluntary buyers, the window to contract durable CDR at voluntary-market prices is closing. For ETS-covered corporates, the procurement muscle you build in 2026 will decide how well you navigate the 2030s.

I will keep tracking the Commission’s Article 30 work and the CRCF methodology pipeline. If you want a deeper dive on any of the four integration models, or a view on which suppliers are already positioning for compliance offtake, reply to this email and I will share our internal assessment.