SBTi changed again?!

SBTi has released its updated draft for the Corporate Net-Zero Standard v2.

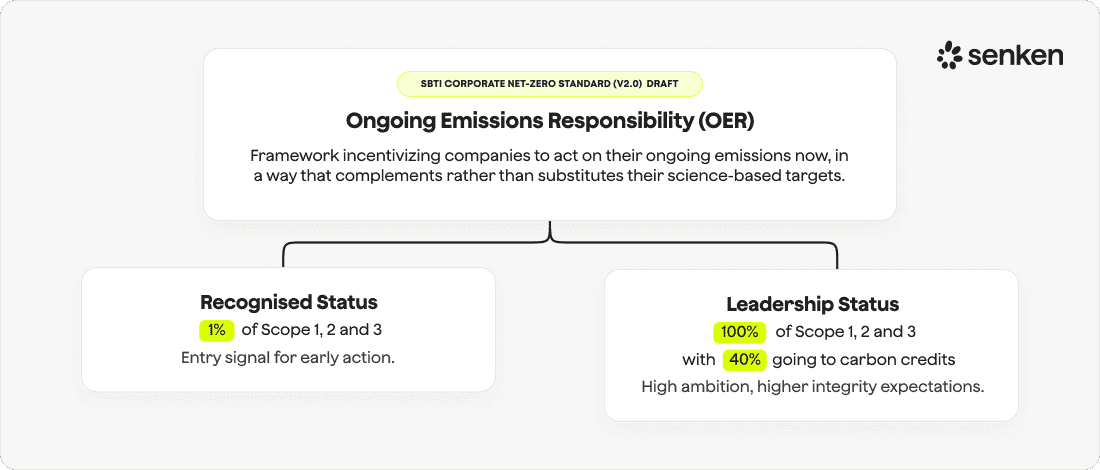

The most significant change being the introduction of Ongoing Emissions Responsibility (OER) — a framework to account for the emissions you still release on the path to net zero.

It gives early movers recognition now and will become a requirement later.

Let’s unpack what this means in plain English.

The two statuses (in plain English):

1. “Recognized”

- Address at least 1% of your ongoing Scope 1, 2, and 3 emissions each year.

- Two routes:

1. Deliver verified mitigation outcomes equal to 1% (ex-post “ton-for-ton”) 2. Apply an internal carbon price to at least 1% and spend that budget on eligible climate actions.

2. “Leadership”

These are SBTi’s words — but the direction is clear: cut first, then take transparent responsibility for what remains.

Is this mandatory?

Not yet. Recognition is voluntary today, but disclosure is not.

You must state whether you participate — and if not, why.

From 2035, Category A companies must begin taking responsibility, starting with 1% through removals and ramping up to full neutralisation by their net-zero year.

What it costs: a quick example

Let's say your annual footprint is:

- Scope 1: 1,000 t

- Scope 2: 5,000 t

- Scope 3: 500,000 t

= 506,000 t (Total ongoing emissions)

- “Recognized” asks for 1%, which is 5,060 t.

- If you buy verified mitigation outcomes at an illustrative €33/t, that is about €166,980 a year.

- If your profit is €100 million, this is 0.17% of profit. Most firms can do this.

- Use your own internal prices if they are higher.

- For the carbon-price route, SBTi’s minimum is USD 20/t applied to at least 1% of ongoing emissions.

💡 Try it for your own numbers

Use Senken's free OER Calculator to compare Recognized and Leadership status. By entering your Scope 1, 2 and 3 emissions, you’ll see how each approach affects your annual profit and budget allocations.

👉 Try Senken's free OER Calculator

How to get it right

Start small, make it real, and show your maths.

Key questions for your internal planning:

- Which route fits us now: 1% “tonne-for-tonne” or 1% internal carbon price?

Let me know if you have any further questions or need support planning for this new approach.

Kind regards,

Adrian

Sources

- SBTi news: second draft of Corporate Net-Zero Standard v2, introducing OER and timelines.

https://sciencebasedtargets.org/news/sbti-releases-second-draft-corporate-net-zero-standard-v2-for-consultation - SBTi blog: what’s new in the updated draft, 1% “Recognized”, 2035 start for responsibility, neutralisation path https://sciencebasedtargets.org/blog/whats-next-for-net-zero-an-updated-draft-of-the-corporate-net-zero-standard-v2

- Consultation guide: disclosure if you do not participate in recognition and how to explain it.

https://sciencebasedtargets.org/consultations/cnzs-v2-second-consultation/draft-standard-chapter-4-taking-responsibility-for-ongoing-emissions - OER explanatory paper: requirements for “Recognized” (≥1% via ex-post outcomes or ≥1% priced at ≥USD 20/t), “Leadership” (USD 80/t on 100% and outcomes equal to 40%.

https://files.sciencebasedtargets.org/production/files/Ongoing-emissions-responsibility-A-framework-for-credible-and-competitive-climate-action.pdf

P.S... Interested in working with Senken? Book a discovery call and let’s see if we’re a good fit.