CBAM and carbon credits? Here's how you can save €€€ at the border

You’ve probably heard of the EU’s Carbon Border Adjustment Mechanism (CBAM).

What most people haven’t heard: CBAM could become one of the strongest forces behind carbon credit growth over the next decade.

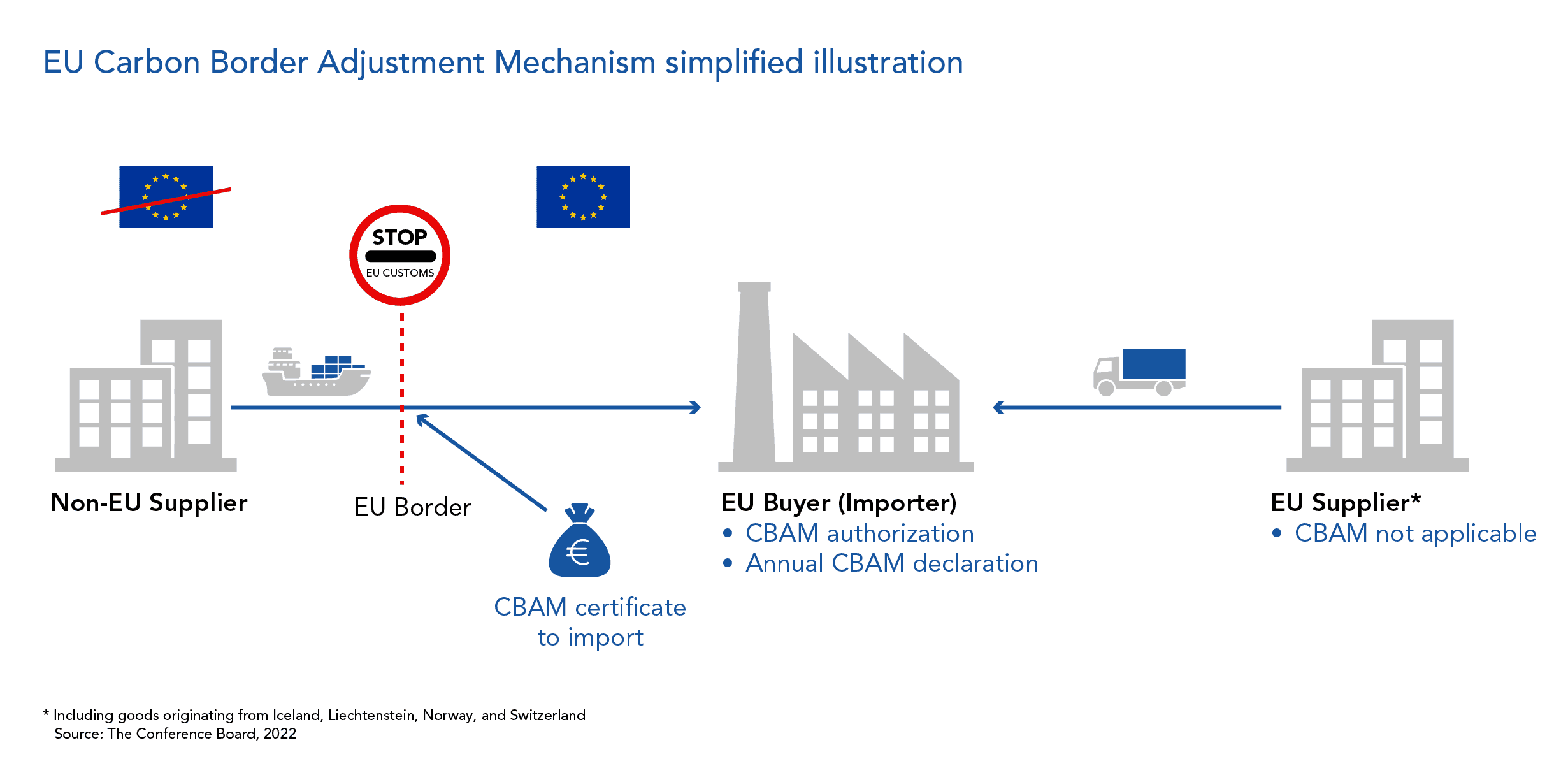

CBAM puts a price on the embedded emissions in imports to the EU.

If a non-EU supplier has already paid a clear, explicit carbon price at home, that amount can be deducted from the CBAM bill at the EU border.

That’s the core equivalence rule: imports should face the same total carbon cost as EU production under the EU ETS.

Voluntary credits don’t count today. Only explicit carbon prices such as a carbon tax, ETS allowance purchase, or levy qualify.

Source: EU Carbon Border Adjustment Mechanism: A Primer for Stakeholders

Why this matters for carbon credits

Some countries already allow part of their domestic carbon price to be paid with Article 6 units, internationally traded credits under the Paris Agreement.

If the EU recognises that country’s domestic price for CBAM deductions, the embedded Article 6 content could flow through indirectly.

You can already see this in Singapore, where companies can use up to 5 % of their carbon tax liability with ITMOs. If the EU recognises Singapore’s tax, importers could effectively see a small share of Article 6 credits reduce their CBAM bill without any new EU law on credits.

Colombia and Japan are piloting similar hybrids.

Quick note: what are ITMOs?

They’re Internationally Transferred Mitigation Outcomes, government-authorised emission reductions that one country can transfer to another under Article 6.

Think of them as credits traded between countries, with safeguards to prevent double counting.

What this means for your supply chain

If you import from outside the EU, this is the key takeaway:

you’ll often pay less by engaging with the carbon price where your goods are produced rather than only paying CBAM at the border.

When your supplier pays a recognised carbon price at home, that amount can be deducted in Europe.

Where no local price exists, you pay CBAM in full.

And those differences are big:

That gap becomes your residual CBAM cost.

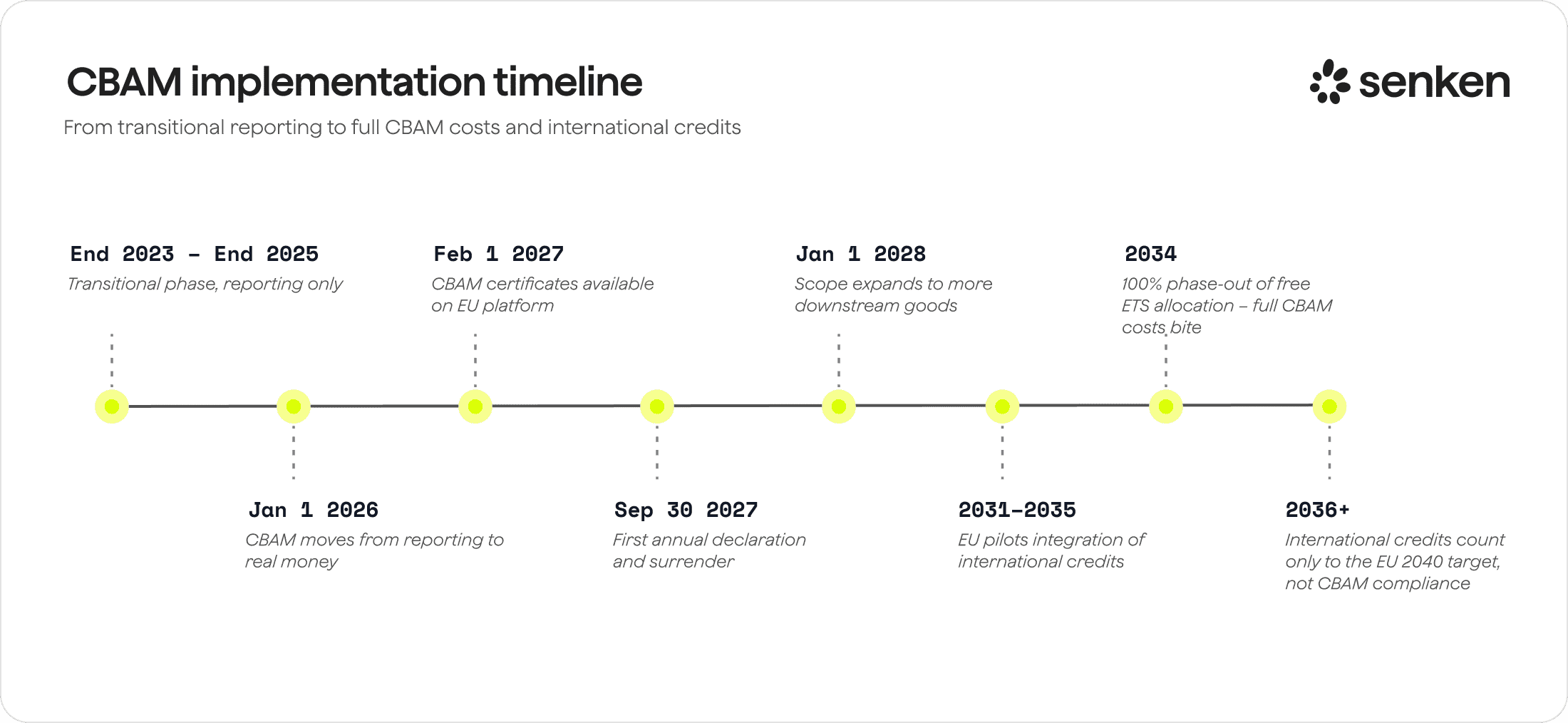

The state of play

The crucial step to watch:

A Commission Implementing Act under Article 9(4), expected Q1 2026, will define which foreign carbon prices qualify and whether systems that include Article 6 units count as “equivalent”.

Until then, the rule is simple: explicit domestic carbon prices reduce CBAM; voluntary credits do not.

A global shift

Carbon pricing is spreading fast.

Roughly 80 systems now cover 28% of global emissions (up from 24% in 2024).

As more countries price carbon and some allow a limited share of Article 6 units, a growing portion of EU imports will arrive with a recognised price attached.

That means lower CBAM bills and, indirectly, more cross-border demand for high-quality credits upstream.

For companies, the question is where to engage.

A supplier paying €10 /t locally won’t offset an €80 EU price, but it reduces what you owe at the border.

That deduction will matter more as CBAM expands.

Three futures to watch

1) Conservative

Only explicit domestic prices count. No credit transitivity.

Credits grow indirectly as producers decarbonise to avoid CBAM costs, but voluntary credits stay outside the equation.

2) Moderate

The EU recognises foreign systems that include Article 6 units.

Transitivity applies in a limited way. Importers sourcing from these markets see smaller CBAM bills, quietly pulling demand for high-quality Article 6 credits upstream.

3) Optimistic

Future updates go further, clarifying broader recognition of Article 6 content.

This would align with the EU’s plan to let up to 5% of the 2036–2040 target be met with high-quality international credits, not for CBAM now, but a signal of where things are headed.

The near-term key remains: the 2026 Implementing Act.

What you can (and cannot) do now

Right now, you can only deduct explicit carbon prices paid abroad.

That’s your starting point.

The potential “credit flow-through” depends on the 2026 rules and whether your suppliers operate under systems that use Article 6 units.

These are not yet implemented, so treat them as future potential, not guaranteed.

If you import, start building records today:

When the recognition rules arrive, that evidence will matter.

And even then, remember, most non-EU prices remain far below EU ETS levels, so a residual CBAM bill will still apply.

What this means for your supply chain

If you import from outside the EU, this is the key takeaway:

you’ll often pay less by engaging with the carbon price where your goods are produced rather than only paying CBAM at the border.

When your supplier pays a recognised carbon price at home, that amount can be deducted in Europe.

Where no local price exists, you pay CBAM in full.

And those differences are big:

That gap becomes your residual CBAM cost.

If you want a short one-pager to share with your procurement team,

reply “CBAM explainer” and I’ll send it to you.

Have a great week,

Adrian

Source

- Carbon Border Adjustment Mechanism - The EU’s environmental policy tool for fair carbon emissions pricing

Information only. This is not legal or investment advice.

P.S... Interested in working with Senken? Book a discovery call and let’s see if we’re a good fit.